Personal Wealth Management / Economics

Minding the Fed’s (Possible) Unwinding

Fed balance sheet reduction doesn't seem likely to materially impact stocks.

Many suspect the Fed will try make the numbers on its balance sheet smaller starting next week. Photo by Absolut_100/iStock.

Next Tuesday and Wednesday, the fun bunch at the US Federal Open Market Committee (FOMC, the Fed's monetary policy-making folks) will get together and discuss monetary policy.[i] There is talk of rate hikes, but after Fed head Janet Yellen alluded to it in recent meetings, most speculation centers on whether or not the Fed will begin unwinding the bond purchases made under its earlier quantitative easing program (QE). "Balance sheet reduction," in central bank-speak. Many presume this spells big trouble-higher interest rates! Less Fed "support" for stocks! However, in my view, a look at recent history and the Fed's plan shows these fears are likely quite overdone. Beyond a possible short-term wiggle, the Fed's reducing the size of its balance sheet doesn't seem likely to materially impact stocks.

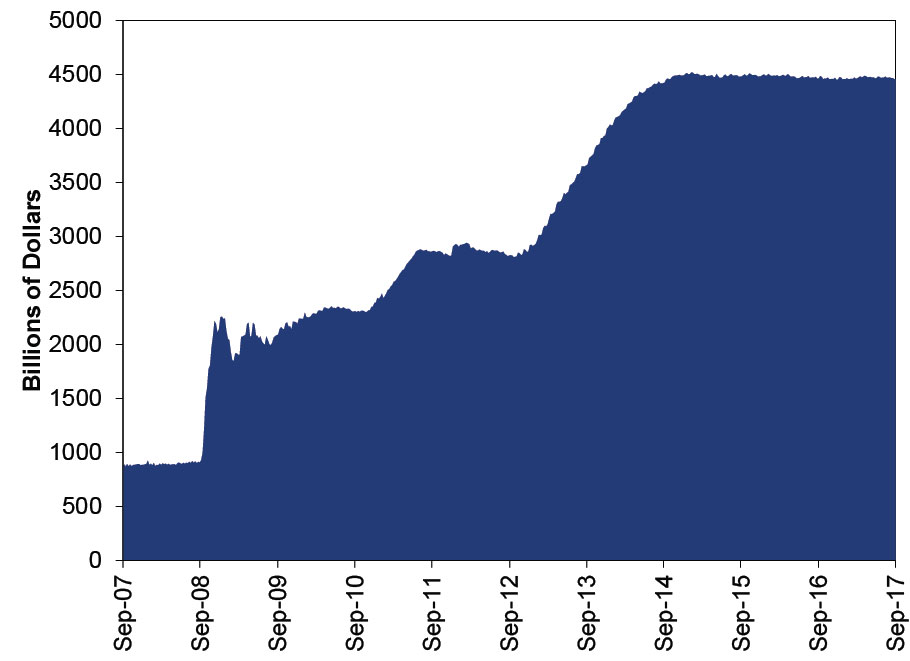

Under QE, the Fed created new bank reserves and used them to purchase longer-term Treasurys and mortgage-backed securities from banks. Trillions' worth, at that. In the 12 months before September 2008, the Fed's assets (which hardly anyone mentioned prior to 2008) averaged $880 billion.[ii] Last week, the Fed's total assets stood just under $4.5 trillion.[iii] While the Fed is no longer increasing its holdings, it is maintaining them by reinvesting the proceeds of maturing bonds. Hence the flattening in the top right of Exhibit 1.

Exhibit 1: Total Fed Assets

Source: Federal Reserve Bank of St. Louis, as of 9/12/2017. 9/5/2007 - 9/6/2017.

Ostensibly, they did so to "stimulate" the US economy by lowering interest rates. The Fed argued this would goose loan-and economic-growth. Many take them at their word, believing the huge increase in Fed assets is responsible (in large measure) for this bull market and economic expansion. Others argue all the Fed "money printing" inflated stocks. Believers in these theories largely fear any tweak to Fed policy. That included the 2013 - 2014 "tapering" (slowing) of bond purchases, which came and went with nary a ripple in markets.[iv] But instead of that experience assuaging Fed fears and making folks realize the central theory of a Fed-fueled bull is off target, many simply shifted focus to the time when the Fed ceases reinvesting and maintaining the mountain of assets.

But despite the big balance sheet increase and promises of "stimulus," QE's bond buying never injected huge quantities of money into the American economy. The Fed actually doesn't do so directly, instead relying on banks to extend loans to increase the quantity of money. The Fed increased the reserves that can underpin bank loans. It didn't-and doesn't-print money.

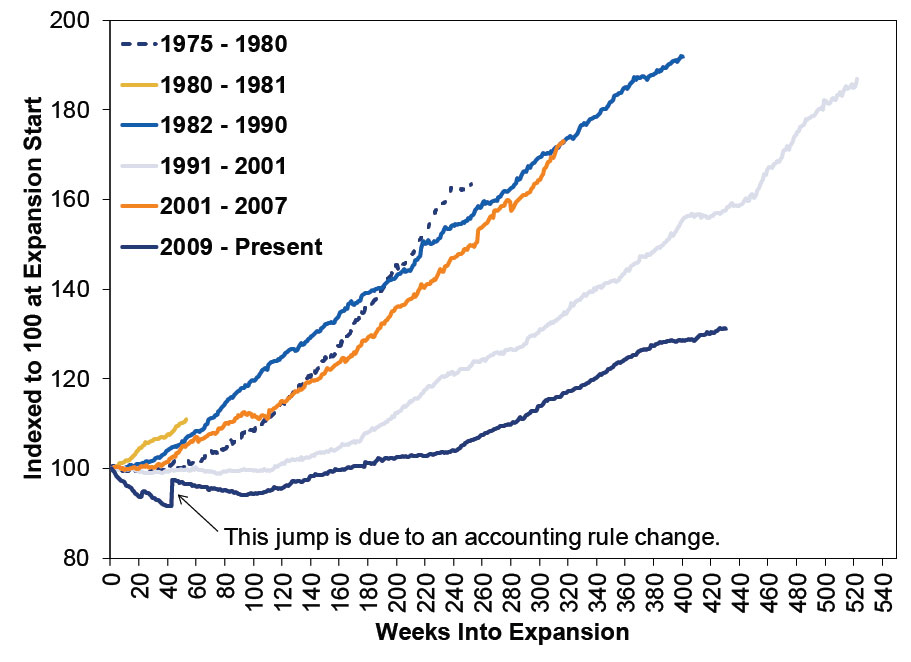

I italicized the word "can" two sentences ago because nothing says reserves "must" underpin new loans. Many of those newly created bank reserves have not underpinned lending in this cycle. Consider Exhibit 2, which shows loan growth has been very slow in this expansion compared to recent US economic history.

Exhibit 2: Slow Bank Loan Growth During This Expansion

Source: Federal Reserve Bank of St. Louis, as of 9/12/2017. Total loan growth indexed to 100 at each expansion's start.

The trouble? The Fed's very actions actually discouraged lending! Banks traditionally profit by borrowing short term (think: checking and savings accounts or interbank loans) and lending long term (mortgages, car loans, business loans). The spread between the rate they receive and their funding cost is profit. Bond prices and yields sit on opposite sides of a seesaw-so roughly $3.8 trillion of Fed buying likely pushed long-term bond prices up and yields down. That dragged down loan profits, discouraging lending. Moreover, with the unpredictable Fed constantly tinkering with long rates, banks had little clarity about where rates-and their profits-would head. Add this to the uncertain post-2008 regulatory environment, and it shouldn't be surprising reserves sat idly on bank balance sheets collecting dust.

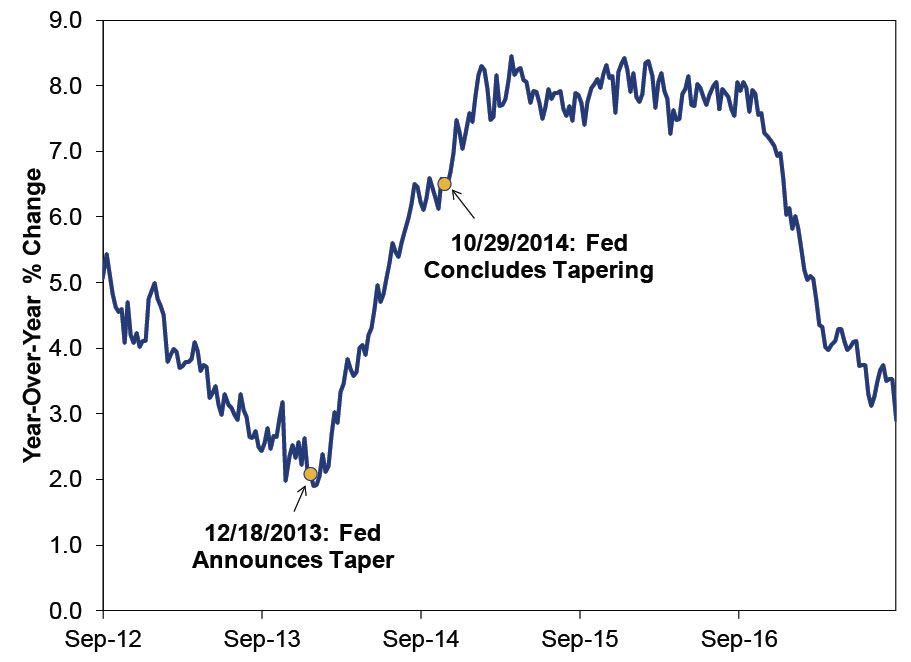

Hence, the Fed's tapering QE didn't hurt the economy; it actually helped. It gave banks some more clarity about the lending environment and likely made them more willing to take risks. Loan growth unsurprisingly accelerated after the taper-just the opposite of what most observers expected.

Exhibit 3: US Loan Growth Accelerated During and After QE Taper

Source: Federal Reserve Bank of St. Louis, as of 9/12/2017. 9/5/2012 - 8/30/2017.

For the same reason, it would likely be positive-not negative-if yields were to tick up after the Fed reduces its balance sheet.[v] A steeper yield curve could encourage more lending and possibly reverse the recent slowdown seen in Exhibit 3. Decades of data show steep yield curves typically foretell faster economic growth ahead. Although I doubt we'll actually see much higher rates post-balance sheet reduction, given the scope of the Fed's plan.

If the Fed were to go hog wild and sell a slew of bonds all at once, that might boost rates (and potentially cause disruptions). But that isn't what they said their plan is. In June, the Fed published how it intended to reduce its balance sheet. The plan is to move at a pace reminiscent of continental drift.

The Fed isn't going to sell assets at all. It isn't even going to stop reinvesting all maturing bonds. Initially, the Fed will stop reinvesting $10 billion in maturing bonds monthly. That is 0.2% of Fed assets. It will increase this amount by $10 billion quarterly until reaching a maximum $50 billion monthly rate. If the Fed initiated this plan next week, it would reach pre-crisis asset levels sometime around St. Patrick's Day 2024. The Fed hasn't said how big or small they intend the balance sheet to be when unwinding is complete, but it sure doesn't seem like they are in a rush to get to whatever level they target. From my perspective, that pace is far too gradual to affect markets materially.

Of course, the Fed could change plans. Data could shift. Their interpretations of said data could change-they are unpredictable humans who can't be forecast, after all. And, as has been well documented, the Fed has lots of openings on its board-over time, new FOMC officials may not be wedded to whatever the Fed's course is. Heck, maybe somebody accidentally bumps a giant red button labelled "Liquidate Assets Non-Incrementally."[vi] But based on what we know now, the Fed's balance sheet reduction plan seems likely to prove a very gradual reversal of what was an economic and market negative to begin with. Beyond possible very short-term swings, this seems very unlikely to move markets much.

[i] They usually do crack some jokes too. It may actually be fun. Though Janet Yellen's jokes from the day after Lehman failed in 2008 now seem a little...insensitive?

[ii] Source: Federal Reserve Bank of St. Louis, as of 9/12/2017. Average Federal Reserve system total assets, 9/5/2007 - 9/3/2008.

[iii] Ibid. Total Federal Reserve system assets, 9/6/2017.

[iv] It also included folks (wrongly) fearing fed-funds target rate hikes, although that isn't a feature unique to this bull market. At any rate, the Fed has hiked four times now in this cycle with no bear ensuing.

[v] Yields actually fell after the Fed tapered, probably partly because they rose in anticipation of the move and because there is a whole lot of demand for high-quality, liquid sovereign debt.

[vi] That is a joke about central banker-speak. Sorry.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary 3 Things You Need to Know This Week | Q2 Earnings, ECB Meeting, Trump Accounts

2026-07-20

2026-07-20 -

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—July 13 - July 172026-07-20

-

Market Analysis Pumping Up the Yen?2026-07-17

-

Expert Commentary This Week in Review | US-Iran Conflict, US Inflation, New UK Prime Minister

2026-07-17

2026-07-17

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today