Personal Wealth Management / Market Analysis

No Mystery in Falling Bond Yields

Like so much else, they imply a return to (mostly) normal.

Since mid-May, eurozone long-term interest rates have plummeted. In Germany, the entire yield curve—interest rates across the range of German government bond maturities—is below zero out to 30 years. This is occurring as eurozone (and German) economic growth has accelerated. Is there a disconnect—a cause for concern—as some coverage suggests? We don’t think so. Let us explain.

The recent move is largely a reversal of volatility earlier this year, when so many thought reopening would juice economic growth and inflation for a long time to come. Bond yields’ rise was global, dubbed the “reflation trade.” Long-term eurozone yields climbed into positive territory in February as vaccinations ramped up and countries began reopening.[i] Deflation late last year turned into inflation this year with the headline rate speeding to 2.0% y/y in May (finally hitting the ECB’s target after years below it).[ii] Pundits saw this as just the tip of the iceberg, warning supply constraints and rising raw materials prices would make prices soar and stay there. Eurozone GDP has since accelerated to 2.0% q/q growth (8.3% annualized) in Q2 from Q1’s -0.3%, with economists presently projecting 2.4% growth in Q3.[iii] Q2 GDP stands -3.0% below its late-2019 peak, so a couple more quarters of rapid catch-up growth could lie ahead.[iv]

But after the rebound back to pre-pandemic GDP levels, more pedestrian pre-pandemic growth rates should follow. Countries that reopened earlier—and regained their pre-pandemic peaks—like China and America, are already experiencing this. Meanwhile, economists are penciling in similar, with quarterly eurozone GDP growth estimates falling back to sub-1% q/q next year—its typical rate range.[v] Inflation also seems to be leveling off, with June’s reading decelerating to 1.9% y/y.[vi] Inflation fears have tapered off as well, and most pundits now presume this year’s inflationary pressures are temporary anomalies. Falling eurozone bond yields are perfectly consistent with the economic outlook many see: slower economic growth and milder inflation than they initially expected.

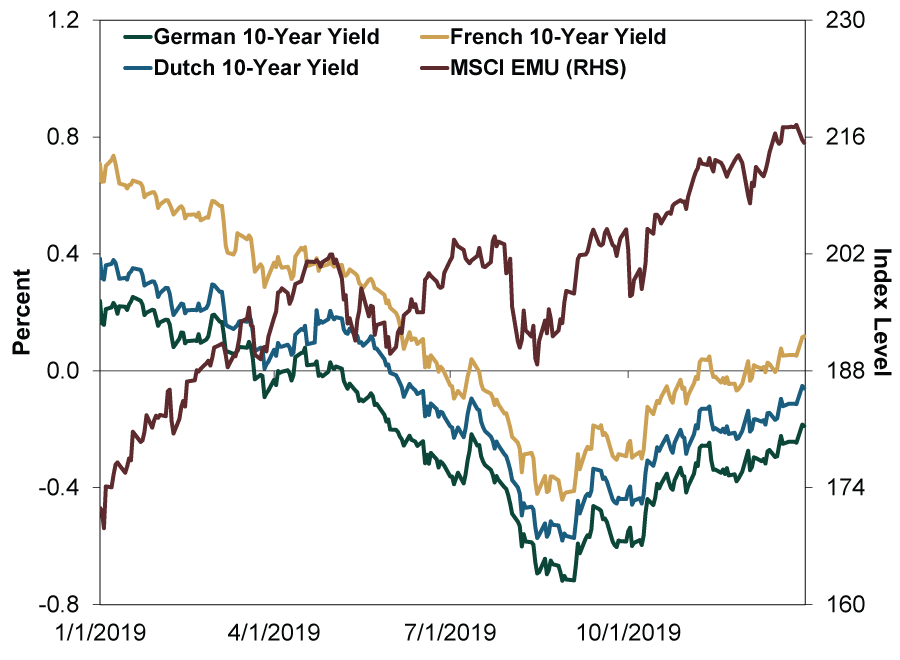

Yields’ directionality isn’t the only thing boggling pundits. The level—sub-zero long-term yields—is also a bogeyman. Yet negative eurozone government bond yields are nothing new—they existed most of (pre-pandemic) 2019. Back then, pundits argued growing piles of negative-yielding bonds signaled the world was “turning Japanese,” buried under mountains of debt and facing lost decades of economic sclerosis. Expectations now aren’t that dire, but many still fear negative yields portend a swift return to recession in Europe. Yet 2019 is a strong counterpoint against that fear. As it turned out, the eurozone economy—and stocks—were fine with negative rates. There was no stagflation or deflation. Despite sub-zero bond yields in 2019, GDP grew. Stocks climbed, too. (Exhibit 1) 10-year German bund yields also dipped negative from June to October 2016 without any ill consequences. Germany’s GDP rose 2.1% that year and its prices didn’t deflate.[vii] German stocks rose 5.8%.[viii]

Exhibit 1: Stocks Aren’t Bothered by Negative Rates

Source: FactSet, as of 8/6/2021. 10-year German, French and Dutch government benchmark bond yields and MSCI EMU return with net dividends, 1/1/2019 – 12/31/2019.

It is also important to recognize the outside influences on eurozone nations’ yield curves. The ECB is still buying €87 billion per month in long-term bonds through its quantitative easing (QE) program. By taking bond supply off the market, the ECB adds to downward pressure on yields. With the ECB (and other central banks) meddling so much in long-term bond markets, rates there reflect QE as well as private investors’ independent assessment of economic conditions. Said differently, it is important to discern between artificial forces influencing rates’ level and the strong market forces influencing their directionality.

Compounding matters, the ECB has gone farther than other central banks in taking its short-term policy rates negative. Its benchmark rate is presently at -0.5%, versus 0.0% – 0.25% in the US and 0.1% in the UK. Meanwhile, in Japan, where yields are negative out to nine years, the BoJ’s policy rate is -0.1%.[ix] We think that goes a long way toward explaining why the eurozone’s yield curve is mostly negative and the US’s and UK’s aren’t. As those who make their living in bond arbitrage might point out: The long term is made of a series of short terms. Negative short-term rates, over a long enough while, add up to negative long-term rates.

Lastly, the latest downdraft in eurozone yields is part of a global move. Developed-market bond yields may be higher or lower in different areas of the world—in part due to structural issues like we just discussed—but directionally they tend to move together, as global markets usually do.

Overall, we don’t see cause for alarm in bond yields’ move. Perma-fast growth was never likely, which we think most now recognize. Roaring Twenties chatter, ubiquitous earlier in the year, has died down. It shouldn’t be surprising to see slower growth rates after economic activity returns to normal—and markets reflect that outlook. Low and negative developed market bond yields featured prominently in the pre-pandemic financial landscape. They seem to be picking up where they left off before lockdowns interrupted: pricing in a late-cycle, slow-growth economic expansion and little inflation in the long run, once the current distortions even out.

Stocks appear to be doing the same. While bull markets do fine in a slow-growth environment, not all categories benefit equally—growth stocks usually do best at such times, and we think the resumption of growth’s leadership this spring is no coincidence. In our view, this is all of a piece. There is no disconnect, mixed messages or conundrum. In our view, markets are behaving rationally given the likely conditions ahead.

[i] Source: ECB, as of 8/9/2021. Statement based on Euro area yield curves, 2/16/2021.

[ii] Source: FactSet, as of 8/9/2021. Eurozone Harmonised Index of Consumer Prices, August 2020 – May 2021.

[iii] Ibid. Real GDP, Q1 and Q2 2021, and FactSet Economic Estimates for real GDP growth, Q3 2021.

[iv] Ibid.

[v] Ibid. Statement based on FactSet Economic Estimates for real GDP growth, Q1 2022 – Q4 2022.

[vi] Ibid. Eurozone Harmonised Index of Consumer Prices, June 2021.

[vii] Ibid. German GDP, 2016.

[viii] Ibid. MSCI Germany return with net dividends, 12/31/2015 – 12/31/2016.

[ix] Ibid. ECB, Fed, BoE and BoJ overnight policy rates, 8/9/2021.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis Pumping Up the Yen?2026-07-17

-

Expert Commentary This Week in Review | US-Iran Conflict, US Inflation, New UK Prime Minister

2026-07-17

2026-07-17 -

Market Analysis Business Friendly Bureaucracy or No, Britain is Growing2026-07-16

-

Economics Don’t Doubt the Old World2026-07-16

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today