Personal Wealth Management / Market Analysis

Notes on the November Pundits Say You Should Remember

The bull market’s breadth is a lot longer-lived than headlines suggest.

Have you heard the good news? Evidently, November is when the S&P 500’s rally finally became real. In addition to being an overall banger of a month with a 10.8% price return, more constituents rose than in any prior month since April.[i] Headlines hyped this piece of trivia Monday, exclaiming their relief that this bull market has finally spread beyond huge Tech and Tech-like companies. The implication: The recovery is now real and value stocks’ time to shine has arrived. Thing is, the rally has long been a lot broader than pundits seem to think, and it has featured several value countertrends. Reading into any of November’s trivia as if they were significant or predictive is a recipe for error, in our view.

Through last Friday’s close, of the companies that have been in the S&P 500 all year, 464 had positive returns for November.[ii] That is indeed the most since April, when 477 were positive.[iii] But it isn’t like the vast majority of S&P 500 constituents just stood still all spring and summer. Even before November’s barnburner, 487 S&P 500 companies had positive returns since the bear market’s March 23 low.[iv] So if you are inclined to be cheeky, you are welcome to point out that the rally actually narrowed in November. More importantly: The notion that Tech and Tech-like companies alone were driving this rally has been wrong from the start. This new bull market has always had broad participation. It just took a long while for people to notice, which speaks to sentiment, but that is about it.

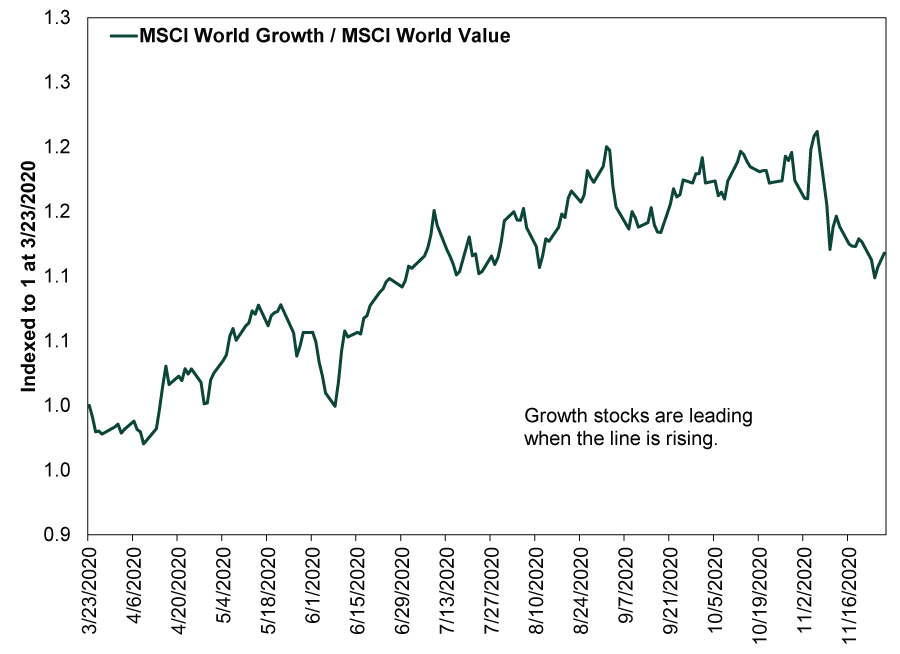

The heavy focus on value’s November leadership also speaks to sentiment. People keep looking for value to take the reins permanently. As Exhibit 1 shows, this isn’t value’s first turn with the baton since the bull market began in March. It has had several prior short bursts of leadership, and pundits seized on all of them as a sign of a permanent shift. Yet growth has led overall, and it takes a fundamental change in market conditions for longer-term leadership to shift. That is why value’s prior stretches of outperformance didn’t last—they stemmed from sentiment, not fundamental change.

Exhibit 1: Growth and Value in This Bull Market

Source: FactSet, as of 11/30/2020. MSCI World Growth and Value Index returns with net dividends, 3/23/2020 – 11/27/2020. Indexed to 1 at 3/23/2020.

We think that is likely the case this time, as well. For months, we have heard speculation that a vaccine would be a catalyst for small value-oriented stocks to outperform, as it would allow the businesses most hit by the pandemic to get back to normal. While that is possible, the theory is widespread—suggesting efficient markets have already incorporated the developments into pricing. Investors have been well aware of the various candidates and their progress in clinical trials for months now. If a vaccine were a fundamental driver for value leadership, then based on how markets generally work, it would have shown up in returns before November. So while we are monitoring growth and value trends, we think this suggests November’s pop was another sentiment-based reaction.

Also favoring growth stocks: Financial conditions. Long-term bond yields might be up a smidge since summer, but they are still near generational lows, leaving yield curves globally quite flat. This is a headwind for value stocks, which tend to get the majority of their funding from bank loans rather than issuing corporate bonds. They also carry relatively higher debt, making them more of a credit risk than big growth stocks (which boast cash-rich balance sheets). When the yield curve flattens, it discourages lending to all but the most creditworthy companies—banks borrow at short rates and lend at long rates, so the yield curve spread is a proxy for their profit margins on new loans. A flat spread means flat profits and minimal reward for taking risk. Since value stocks are generally higher-risk for banks, a flat yield curve tightens credit availability. As a result, we have a strong hunch that even if a vaccine does turn on the revenue spigots for many of these companies, they will probably use that windfall to pay down debt and shore up the underlying business, rather than return mountains of cash to shareholders, which erases one of value stocks’ main attractions. Elsewhere, value-oriented Energy firms still face an oil glut that weighed on prices and profts even before the pandemic. Reigniting demand would help, but it will likely take a considerable resurgence.

Value isn’t dead, and we think owning some for diversification’s sake is important. But we think it would take a fundamental shift and/or a notable deterioration in sentiment toward it—folks ceasing the continual hunt for a value catalyst—for its leadership to prove lasting. Thus far, we haven’t seen either one.

Leadership or no, value stocks have participated in this bull market dating back to March. In our view, pundits’ inability to see this speaks to bleak pessimism that has led to so many dismissing the upturn for the entirety of its climb thus far. Perhaps that narrative changed in November. If so, fine, but investors shouldn’t see it as a material turning point for stocks.

[i] Source: FactSet, as of 11/30/2020. S&P 500 price return, 10/31/2020 – 11/30/2020.

[ii] Source: FactSet, as of 11/30/2020. S&P 500 constituent total returns, 10/31/2020 – 11/27/2020.

[iii] Source: FactSet, as of 11/30/2020. S&P 500 constituent total returns, 3/31/2020 – 4/20/2020.

[iv] Source: FactSet, as of 11/30/2020. S&P 500 constituent total returns, 3/23/2020 – 10/31/2020.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis The New Tariffs in Town Are Still Old News2026-07-24

-

Expert Commentary This Week in Review | Market Volatility, Tariffs, SpaceX

2026-07-24

2026-07-24 -

Expert Commentary Why Ken Fisher Is Optimistic About European Stocks

2026-07-23

2026-07-23 -

Economics A Summertime Check-in on US Consumers2026-07-23

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today