Personal Wealth Management / Economics

Now Hiring: Shades of Optimism

The reaction to the latest US jobs data points to warming sentiment.

Last week’s November US jobs report gave pundits plenty of reasons to cheer. Employers hired at the fastest clip since January, and the unemployment rate fell to a 50-year low. While employment numbers are late-lagging indicators, they confirm what forward-looking markets have long since priced in: The US expansion is chugging along. Yet the reaction wasn’t universally positive, as some nitpicked at measures like the labor force participation rate and its implications for future growth. That pundits are still poring over a long-running false fear suggests sentiment is rationally warming up to the US’s solid economic picture—but isn’t overdoing it. All perfectly normal, in our view, in a later-stage bull market.

Here is the November hiring highlight reel: Employers added 266,000 jobs, the headline unemployment rate fell to 3.5%—the lowest since May 1969—and wages rose 3.1% y/y. The U6 unemployment rate, which includes discouraged workers who haven’t sought jobs recently and those working part-time because they couldn’t find full time work, hit 6.9%, the second-lowest reading in its 25-year history. However you slice it, good news!

Most acknowledged those solid numbers, but a few still questioned some measures’ ongoing weakness—like the labor force participation rate (LFPR). The LFPR is the percentage of the civilian population (16 years and older) that is working or actively seeking a job. At the expansion’s start, the LFPR was 65.7%.[i] Since then, it has lurched lower, bottoming at 62.4% in September 2015. It is currently at 63.2%, recovering less than a percentage point since that 2015 low, and still far off the 66% – 67% range during the 1990s expansion.

LFPR worries have been around for the past decade and involve handwringing about the long-term economic consequences. In 2011, a declining LFPR allegedly signaled the labor market was changing for the worse—a headwind for future growth.[ii] A couple years later, a LFPR just north of 63% supposedly implied fewer workers were supporting entitlement programs like Social Security and Medicare.[iii] In 2015, headlines speculated a falling LFPR could prompt Fed stimulus.[iv] In 2017, some argued the long-term decline of the “prime-age” LFPR—which tracks workers aged 25 – 54—meant certain segments of the population were getting shut out of the economy.[v]

These developments are noteworthy and impactful, but they are mostly sociological—not economic—issues. From a market perspective, these trends don’t materially affect stock supply and demand in the next 3 – 30 months, the timeframe stocks care about most. Certainly some of the declining labor force participation is associated with retiring baby boomers who don’t financially need to work until age 65. Some likely is tied to higher education. But for our purposes, the “why” behind the lower LFPR isn’t hugely important.

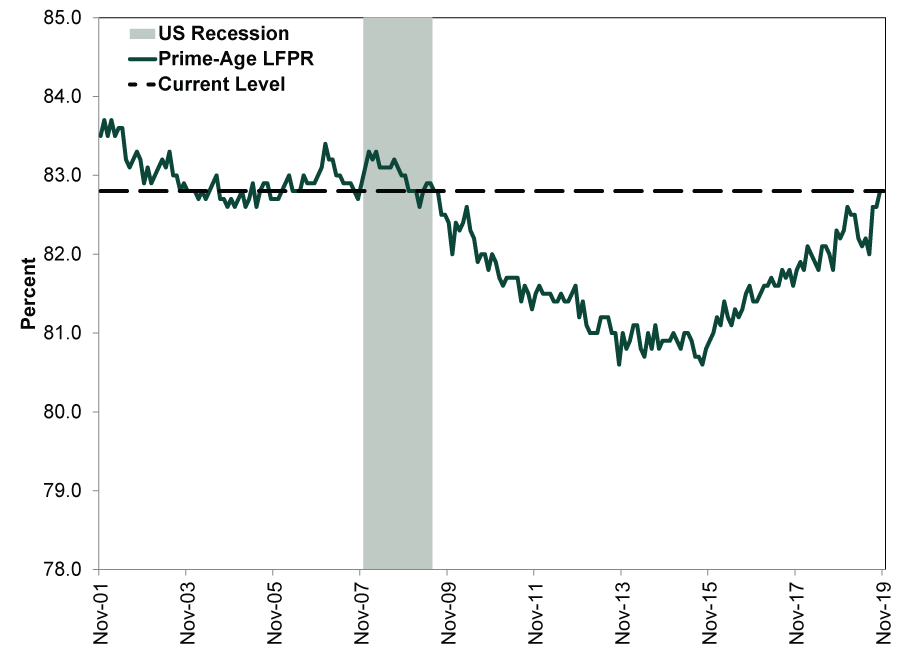

Rather, we find it interesting pundits are still fretting a lower LFPR’s alleged negative economic implications despite a decade-long expansion. The ongoing negative focus also overshadows some positive trends. Consider the closely followed prime-age LFPR. This rate has been improving since its September 2015 low. November 2019’s 82.8% rate is a shade shy of the expansion’s June 2009 82.9% high—and in line with rates seen throughout the pre-financial crisis expansion. Not all is as bad as portrayed.

Exhibit 1: US Prime-Age Labor Force Participation Rate Since November 2001

Source: Federal Reserve Bank of St. Louis. Civilian labor force participation rate: 25 to 54 years, percent, monthly, seasonally adjusted, as of 12/10/2019. November 2001 – November 2019.

Interestingly, a time economists cheered a rising labor participation rate coincided near a bull market peak. In April 2000, The New York Times noted this about the March jobs report:

To some economists, the most striking element of the report was its suggestion that the intense demand for workers is drawing more people into the labor force, allowing the labor force to expand at a pace above the growth in the working age population.[vi]

This was less than two weeks after the Tech Bubble burst, starting a bear market—and recession would follow in March 2001. While just one example, this tidbit reinforces both employment data’s lagging nature as well as the euphoric sentiment that colored experts’ views of the US economy at that time. Some believed labor force growth was about to speed up—yet the economy would contract less than a year later.

We aren’t saying these metrics are market-timing tools. Again, shifts in employment trends follow economic growth, which in turn lags the stock market. But how pundits view the numbers provides a snapshot of sentiment. While many seem to acknowledge the US economy is doing well—a rational perspective, in our view—some hesitation still lingers. When the fretting stops and folks are broadly optimistic, investors should start monitoring how reality squares with expectations—and whether the latter starts exceeding the former.

[i] Source: FactSet, as of 12/12/2019. Labor Force Participation Rate, June 2009.

[ii] Source: “Why the Unemployment Rate Has Become a Bad Joke,” Jeff Cox, CNBC, published 2/14/2011. https://www.cnbc.com/id/41583533

[iii] Source: “Labor Participation Lowest Since 1978,” Steve Hargreaves, CNN, published on 9/6/2013. https://money.cnn.com/2013/09/06/news/economy/labor-force-participation/

[iv] Source: “Falling Labour Participation Raises US Jobs Dilemma for Fed,” Sam Fleming, Financial Times, published 11/3/2015. https://www.ft.com/content/ae71a322-81de-11e5-8095-ed1a37d1e096

[v] Source: “Unemployment Is So 2009: Labor Shortage Gives Workers an Edge,” Eduardo Porter, The New York Times, published 9/19/2017. https://www.nytimes.com/2017/09/19/business/economy/labor-shortage.html

[vi] Source: “Job Growth Sets 4-Year Peak Despite Higher Interest Rates,” Richard W. Stevenson, The New York Times, published 4/8/2000. https://www.nytimes.com/2000/04/08/business/job-growth-sets-4-year-peak-despite-higher-interest-rates.html?searchResultPosition=44

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis The New Tariffs in Town Are Still Old News2026-07-24

-

Expert Commentary This Week in Review | Market Volatility, Tariffs, SpaceX

2026-07-24

2026-07-24 -

Economics A Summertime Check-in on US Consumers2026-07-23

-

Expert Commentary Why Ken Fisher Is Optimistic About European Stocks

2026-07-23

2026-07-23

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today