Personal Wealth Management / Market Analysis

On Britain’s Rising Rates and Debt Service

While a chunk of Britain’s debt costs is linked to inflation, interest payments aren’t soaring.

Editors’ Note: MarketMinder doesn’t make individual security recommendations. The below merely represent a broader theme we wish to highlight.

Whenever long-term interest rates rise, it isn’t long before the focus turns to debt—national debt. It already seemingly has in Britain, with 10-year Gilt yields set to close August at their highest since early 2014—2.8%.[i] That level isn’t high by global or historical standards. Nor does it tie to concerns about the UK’s creditworthiness—rather, we think it is part of a global, sentiment-fueled wiggle as investors continue overthinking central bank rate hikes. We doubt it sticks for long. Yet it is raising some eyebrows across the pond because a big chunk of the UK’s outstanding debt has inflation-linked interest rates, making Britain’s debt service costs more sensitive to consumer price levels than America’s. Even with this factored in, however, we don’t think UK debt is a ticking time bomb likely to hit the economy or markets in the foreseeable future.

The raw numbers here might seem alarming. UK net debt (which excludes intra-government holdings) outstanding tops £2 trillion and finished fiscal 2021/2022 at 98.2% of GDP.[ii] According to the official figures, 30% of the total Gilt pile is inflation-linked, and due to some quirks in British national statistics and official policy, that linkage is to the antiquated Retail Price Index (RPI), which runs higher than the Consumer Price Index.[iii] That rate hit 12.3% y/y in July, creating the specter of a rapidly rising interest rate bill.[iv]

We appreciate that those who highlight this risk are focused on debt service costs, which we think is the right way to look at it. After all, national debt isn’t due all at once. What matters is interest and principal due. Governments usually cover principal repayments by refinancing maturing bonds with newly issued bonds. The UK, like the US, doesn’t have problems on this front given Her Majesty’s Treasury’s sterling reputation.[v] That renders interest payments the swing factor.

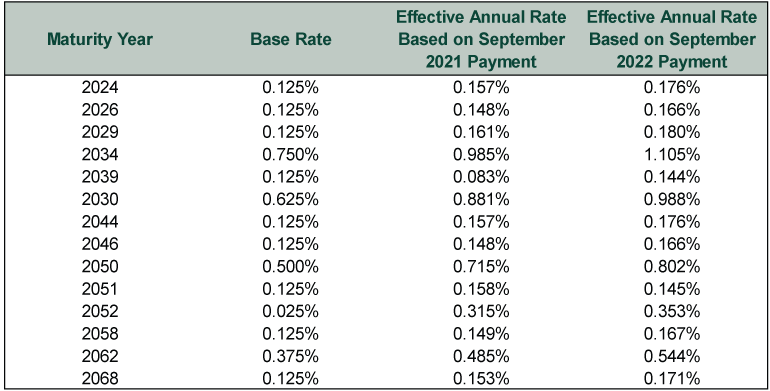

Yet the inflation-adjustment isn’t as simple as applying the RPI inflation rate to the principal value. The UK’s Debt Management Office (DMO) helpfully provides a simple tutorial on how the math works. All inflation-linked bonds have a fixed base rate at issue, which is below the coupon rate for conventional Gilts of comparable maturities. For example, the 50-year index-linked Gilt issued in November 2021 has a base rate of 0.125%, while the conventional 50-year Gilt issued in February 2022, when market-based rates were little changed from November 2021, pays 1.125%.[vi] That base rate then gets multiplied by the cumulative change in the RPI since the bond’s issuance (current RPI divided by RPI at issuance) at a three-month lag. So let’s consider the annual rate the coupon payments on that November 2021 bond due next month imply. First, divide June’s RPI level by September 2021’s. That gives you a ratio of 1.10275. You then multiply that by the base rate, which gives us 0.14%—far below the market rate.[vii] Now, indexed-linked Gilts’ redemption amount also adjusts the principal for inflation. And bonds that have been in issuance longer will have a larger built-in inflation premium, but even there, the immediate payment is much less than headlines imply. Exhibit 1 demonstrates this with all the outstanding index-linked Gilts with interest payments scheduled in September that have been in circulation for longer than a year. (We are using these bonds because the DMO has already officially calculated the September payments, making a year-ago comparison possible.)

Exhibit 1: Effective Annual Interest Rates for UK Index-Linked Gilts With Payments Due in September

Source: UK Debt Management Office, as of 8/31/2022. Lists only bonds issued more than one year ago, hence our earlier example isn’t included.

Moreover, the UK’s overall debt service bill remains quite low. Total interest costs for fiscal 2021/2022 were just 12.1% of total tax revenue.[viii] Interest payments’ share of tax revenues were more than double that throughout the 1960s, 1970s and 1980s, yet that didn’t bring a Greece-style debt crisis or default. The economic upheaval that occasionally arose in the 20th century’s second half, including Black Wednesday and the Winter of Discontent, stemmed primarily from external factors (defending the European Exchange Rate Mechanism for the former, and political issues and the energy crisis for the latter). If Britain could afford paying over 30% of tax revenues on interest at times in the mid-to-late 20th century, we daresay it can afford paying around 12% now, plus whatever inflation adds to the pile—especially with issuance slowing significantly this year thanks to the end of COVID relief borrowing and economic growth lifting tax revenues. We know the latter is a very sore spot for those whose salaries have jumped into higher tax bands now that the rate thresholds aren’t indexed to inflation, but from a pure public finance standpoint, objectively, it helps.

None of this is to argue that all is well and rosy in the UK economy right now. The higher energy price cap, announced late last week, is a headwind for households. Spiraling energy costs are hitting small businesses hard as well, and shortages of CO2 and other important feedstocks are another negative. Most forecasts project recession, and they could well be right. But all of these factors are quite well-known to stocks, limiting the likelihood of some massively negative surprise from here. Meanwhile, debt fears add to the negative sentiment surrounding UK stocks, creating opportunities for uncertainty to fall as investors gradually realize, however subconsciously, that these fears are false.

[i] Source: FactSet, as of 8/31/2022. UK 10-year Gilt yield on 8/31/2022.

[ii] Source: UK Debt Management Office (DMO), as of 8/31/2022. Net debt includes debt owned by the Bank of England as part of its quantitative easing program (officially named the Asset Purchase Programme), as this debt is “marketable,” meaning, it will eventually be available for sale.

[iii] Ibid. Value of index-linked Gilts as a percentage of total UK Gilts, which are all marketable debt securities excluding ultra-short-dated Treasury Bills. This figure is based on the DMO’s estimate of index-linked Gilts’ inflation-adjusted principal values at maturity.

[iv] Source: UK Office for National Statistics, as of 8/31/2022.

[v] Pun intended.

[vi] Source: UK DMO, as of 8/31/2022.

[vii] We are intentionally simplifying this for clarity and argument’s sake. The actual coupon payments, which are paid semiannually, would divide this figure by two, and the inflation-adjustment would change every six months.

[viii] See Note iii.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Politics Blunting Burnham?2026-07-21

-

Market Analysis Why the SOX “Bear Market” Isn’t Foreboding2026-07-21

-

Expert Commentary 3 Things You Need to Know This Week | Q2 Earnings, ECB Meeting, Trump Accounts

2026-07-20

2026-07-20 -

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—July 13 - July 172026-07-20

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today