Personal Wealth Management / Market Analysis

On “Currency Manipulation,” US Trade and Stocks

Currency moves just don't have much influence on trade.

A pile of global loot. Photo by Xaume Olleros/Bloomberg via Getty Images.

As buzzwords go, "currency manipulation" is clunky-two words, eight syllables and a whiff of jargon. But it is nevertheless quite buzzy, thanks to the Presidential debates and Congressional bickering over the Trans-Pacific Partnership trade deal. The claim: Our trading partners are deliberately driving down their currencies to boost exports and gain an unfair advantage over US manufacturers, and unless we make them all play by some tough new rules, America is doomed to be an economic also-ran. It is an easy narrative to sell, and an easy way to score political points for both parties. But it is also wrong. Currency swings hold far less influence over trade than most believe-a point especially relevant to investors today, as fears of the strong dollar escalate.

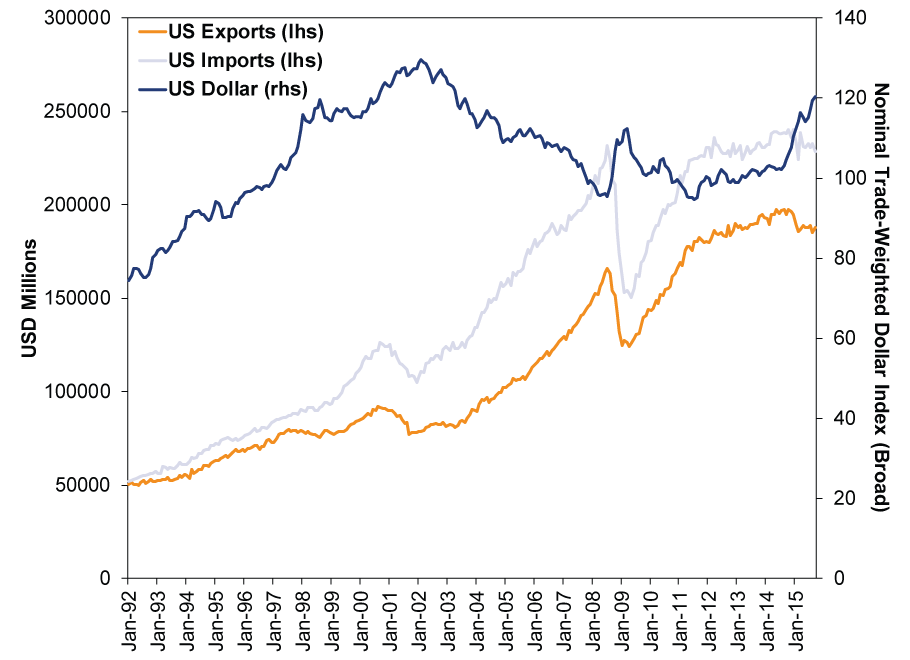

Theory and conventional wisdom say a weak currency boosts exports because it makes goods cheaper overseas, boosting demand. A strong currency, by contrast, makes goods pricier overseas, hitting demand. However, if this were true, one might expect a given country's exports and imports to move in opposite directions from time to time: exports up and imports down when the currency is weak, exports down and imports up when the currency is strong. As Exhibit 1 shows, however, this isn't so. Exports and imports usually move in the same direction, with economic growth the primary driver. Currency trends hold little to no visible influence.

Exhibit 1: US Trade and the Dollar

Source: FactSet, as of 11/11/2015. Seasonally adjusted total exports, seasonally adjusted total imports and Nominal Trade-Weighted Dollar Index (Broad), monthly, January 1992 - September 2015.

The same is true if you look more granularly, at US trade with individual nations. In recent weeks, China, Mexico and Japan have all been cited by various pols as job-stealing currency manipulators. Now, of these three, only China has a closely managed exchange rate, and policymakers there are presently driving the yuan up, not down. The other two trade freely (though Japan's yen is heavily influenced by quantitative easing these days). But politicians rarely let facts ruin a good narrative, so the scapegoating continues.

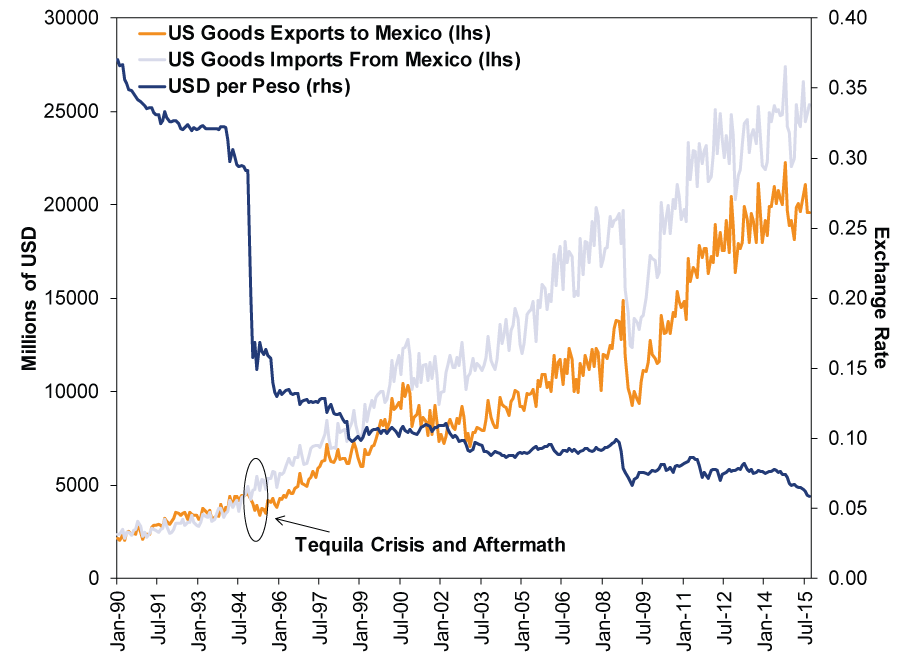

Anyway. If politicians viewed these relationships over the past 25 years, the accusations would fizzle. Let's start with Mexico. NAFTA became the law of the land(s) on January 1, 1994. Months later, Mexico had a financial crisis-known as the Tequila Crisis-culminating in a huge devaluation in December 1994. For the next seven months, US exports to Mexico fell, seemingly supporting the "strong currencies quash exports" crowd. But that assumes the devaluation happened in a vacuum, and all else was hunky dory in Mexico-totally false. The Tequila Crisis had a sweeping economic impact. Mexico took a $50 billion bailout from America in December 1994, and its GDP fell over -6% in 1995. That huge economic contraction sank demand for imported goods. By contrast, America's economy was humming in the mid-1990s, fueling demand for goods from south of the border. As Mexico's crisis faded into history and its economy recovered, demand for US goods returned. Over the last 20 years, barring recessionary blips, US-Mexican exports and imports have soared in tandem, even as the peso gradually weakened. Giant sucking sound, this is not.

Exhibit 2: US Trade With Mexico

Source: FactSet, as of 11/11/2015. US goods exports to Mexico (not seasonally adjusted), US goods imports from Mexico (not seasonally adjusted) and MXN:USD exchange rate, monthly, January 1990 - September 2015.

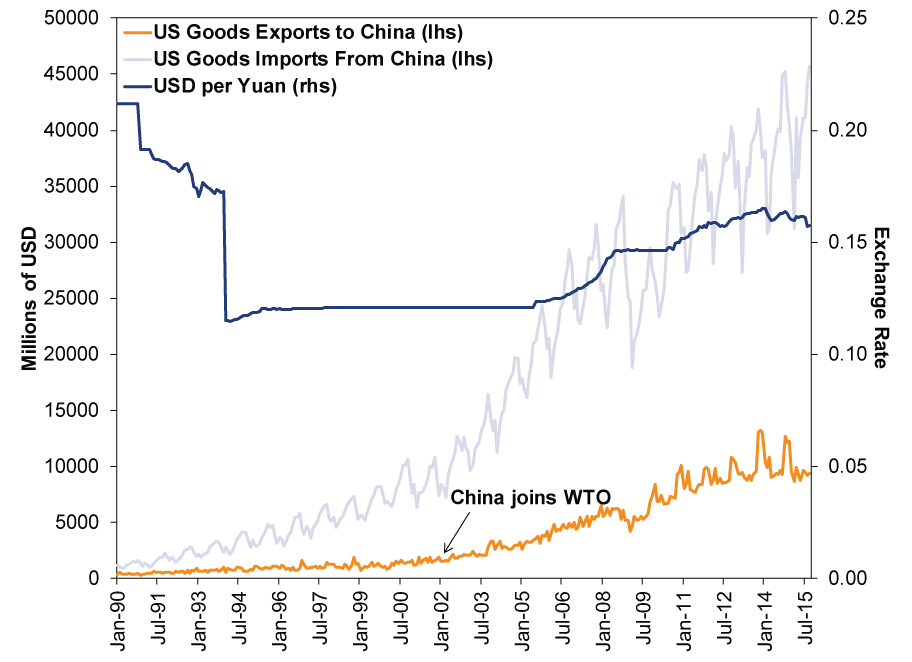

China's story is a bit different. That country also had a currency crisis in the early 1990s, ultimately devaluing in January 1994. Officials pegged the yuan to the dollar for the next decade ostensibly to promote stability-a widespread tactic in developing countries. Since 2005, the central bank has allowed the yuan to appreciate gradually, with some occasional intervention along the way. At the moment, they appear to be propping the yuan up to prevent capital outflows from destabilizing the economy.

US imports from and exports to China grew modestly in the 1990s. Neither changed dramatically after 1994. Imports had grown faster than exports before the devaluation, and that trend persisted afterward-logical, when you consider what each country's manufacturing sector specialized in. China back then was transitioning from its garment phase to its cheap consumer goods phase, and America has long had robust demand for both. America, by contrast, became increasingly focused on high-tech goods, which would naturally find less demand in a less developed nation. China also maintained high trade barriers, further limiting US firms' opportunities there.

But in December 2001, China joined the World Trade Organization (WTO), which required them to slash tariffs and ease administrative import restrictions. We dropped tariffs in return, and bilateral trade took off. Exports and imports grew markedly after that, driven by strong growth in both nations.

Exhibit 3: US Trade With China

Source: FactSet, as of 11/11/2015. US goods exports to China (not seasonally adjusted), US goods imports from China (not seasonally adjusted) and CNY:USD exchange rate, monthly, January 1990 - September 2015.

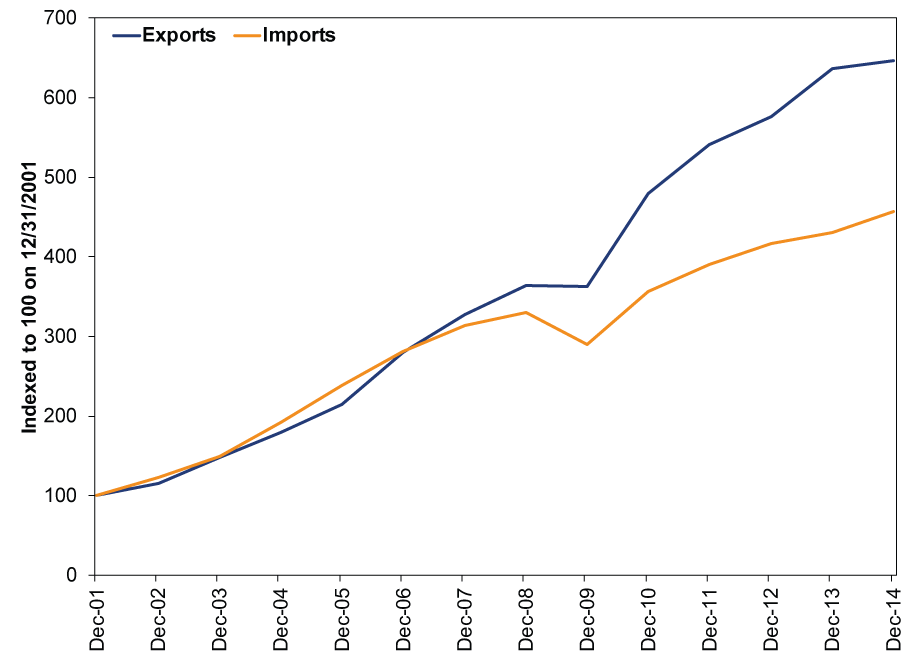

Yes, imports are obviously far, far higher than exports. But they started at a higher base. As Exhibit 4 shows, exports have grown significantly faster than imports since China joined the WTO, even though policymakers from here to Timbuktu claimed the yuan was severely undervalued for much of that span. Growth and trade policy were the swing factors, not currencies, and this is a relationship where both parties "win."[i]

Exhibit 4: Growth in US Trade With China Since China Joined the WTO

Source: FactSet, as of 11/11/2015. Cumulative growth in annual US goods exports to China and US goods imports from China, 2001 - 2014.

And then we have Japan, whose currency has swung wildly for the past 25 years. Japanese GDP has mostly moved sideways since 1997, as the country struggled in vain to shake off its so-called lost decade(s). US-Japan exports and imports have also drifted directionlessly since then-each rose during the good times then fell back in the not-so-good times, sometimes with a rising yen, sometimes with a falling yen.

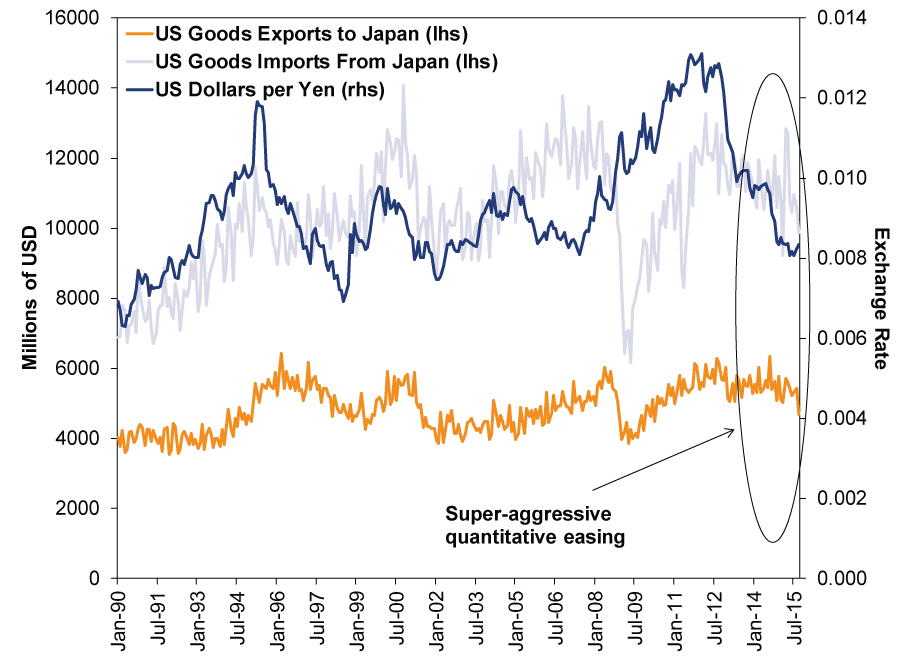

Exhibit 5: US Trade With Japan

Source: FactSet, as of 11/11/2015. US goods exports to Japan (not seasonally adjusted), US goods imports from Japan (not seasonally adjusted) and JPY:USD exchange rate, monthly, January 1990 - September 2015.

Interestingly, exports and imports have fallen a bit since the yen started plunging in late 2012. Conventional wisdom-and Japanese politicians-said Japan's exports would soar as the world snapped up cheaper Japanese cars and gadgets. But Japan's exports didn't soar-not when measured in volume terms. Instead of cutting prices to boost demand, Japanese exporters settled for making a boodle on currency conversion-getting more bang for their buck when turning their dollars back into yen.

This gets to the heart of why currency swings don't influence trade much. Supply and demand in the end market are what ultimately drive pricing. If the US market will bear pricier Japanese goods, then they'll be pricier-simple as that. If firms don't need to slash prices to attract demand, they probably won't. This is why my favorite imported Japanese iced tea has gotten moreexpensive since 2013, not less-anecdotal, granted, but it illustrates the point.

For investors, the upshots are twofold. One, the Trans-Pacific Partnership's (TPP's) lack of strict currency-related provisions doesn't make it a raw deal for America. (And yes, Rand Paul was correct to point out in Tuesday's debate that China isn't part of the TPP.) Should the agreement take effect, it likely would be a very long-term positive for the US economy and markets-markets adore free trade. Two, the currently strong dollar just isn't the severe headwind headlines make it out to be. Firms can and probably will continue exporting more as the rest of the world continues growing. Demand for foreign goods is a byproduct of growth. Those exports might bring in less revenue once the final tally is converted back to dollars, but most exporters have overseas costs, too (imported parts and raw materials, labor, transportation), and the strong dollar reduces these. For many firms, it's a zero-sum game or close to it.

Pop back up to Exhibit 1, and you'll see the dollar soared throughout the mid-to-late 1990s, a great time for US trade, growth and stocks. No reason the same can't be true this time around.

[i] This last bit applies no matter what you think of China's currency policy. You see, the country that exports more doesn't "win" at trade-particularly if their currency policy means they are selling goods cheaper than they could. The "winner" then, logically, is the consumer, who gets the same good he or she wanted at an even better price.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis The New Tariffs in Town Are Still Old News2026-07-24

-

Expert Commentary This Week in Review | Market Volatility, Tariffs, SpaceX

2026-07-24

2026-07-24 -

Economics A Summertime Check-in on US Consumers2026-07-23

-

Expert Commentary Why Ken Fisher Is Optimistic About European Stocks

2026-07-23

2026-07-23

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today