Personal Wealth Management / Market Analysis

On Greek Tweets, Capital Controls, Chaos and Volatility

Has the endgame finally arrived?

Greek Prime Minister Alexis Tsipras takes a break from Tweeting to address Parliament Sunday. Photo by Kostas Tsironis/Bloomberg via Getty Images.

So Greece had a busy weekend, PM Alex Tsipras sent 30 increasingly bizarre Tweets[i], and global markets had a busy Monday pricing in all the chaos. Except in Greece, where markets are closed all week to prevent panic. Virtually everywhere else, though, volatility reigned. With Greece facing political pandemonium, capital controls and imminent default-and creditors clearly out of patience-we can only imagine the bludgeoning Greek stocks would have taken if it weren't for the emergency bank holiday.[ii]Our take hasn't changed: However this ends, the risk of protracted global fallout remains quite small. But brace for more volatility, just in case, and spare a thought for Greek people, because they're in for a tough time.

After Greece's weekend of turmoil, most global benchmarks opened well below Friday's closing levels and stayed there. Eurozone stocks finished Monday down -4.2%, with Italy (-5.2%) and Spain (-4.6%) taking the brunt.[iii] Germany (-3.6%) and France (-3.7%) didn't fare much better.[iv] After European markets closed, Tsipras announced Greece won't make its €1.5 billion IMF payment due Tuesday.[v] (He also sent, at last count, another 29 Tweets.) US stocks kept sliding, finishing down -2.1%.[vi] Given the wealth of question marks over the next week and the mounting mayhem in Greece, we wouldn't be surprised if markets stayed rocky. But this isn't the time to panic-volatility is normal, and the world bounced quickly after Greece-related negativity earlier in this bull market. Even if this is the beginning of Grexit-and it very well may be-the risk of contagion is minimal, and without contagion, Greece is too small to take down the world (see here and here). Heck, at this point, one could argue Grexit could even reduce risk in the rest of the eurozone.

But first, let's catch up on the latest-and we have a lot of ground to cover. When last we discussed Greece in this space, Tsipras and the IMF, ECB and eurozone leaders were closing in on a deal. Tsipras had offered big concessions on tax hikes and pension cuts, and he and creditors didn't seem too far apart. But, as has become the norm, by Wednesday, talks fell apart. Creditors' counterproposal wasn't all that different from Tsipras' salvo, but they wrote it by opening Tsipras' document in (we presume) Microsoft Word and turning on "track changes." What they sent back was a redline version with cross-outs and insertions, with the markup displaying in red-typical of Word's default[vii] settings, but evidently insulting to Greece all the same, given its resemblance to a teacher's markup on a D-student's homework.[viii] Adding insult to injury, creditors chose Wednesday to meet with Stavros Theodorakis, the leader of Greece's To Potami, one of the austerity-friendly pro-euro opposition parties-just to see if he'd support a deal, since many members of Tsipras' Syriza party were already denouncing any compromise.

After that, Tsipras basically walked away, saying creditors either had no interest in a deal or were backing "special interests" in Greece. Emergency meetings of eurozone finance ministers (aka the Eurogroup) broke up after less than an hour on Wednesday and Thursday because the ministers had no new Greek proposals to discuss. EU leaders officially rejected Greece's earlier proposal at their own summit on Friday, saying the red-lined version was the last, take-it-or-leave-it offer. Faced with a legacy-defining choice-violate campaign pledges or drag Greece into bankruptcy-Tsipras punted the decision to his constituents Friday night, calling a referendum.[ix] On July 5, Greeks will vote "yes" or "no" on whether to accept creditors' proposal. Tsipras says a "no" would give him more leverage to get a better deal, or as he Tweeted: "We will be ready to reach a sustainable agreement after the #OXI / NO vote in the #referendum." Germany's Vice Chancellor says a "no" would shove Greece through the eurozone's exit door. Italian PM Matteo Renzi called it a vote on "euro vs drachma."

Complicating matters is the fact that the proposal Greeks will vote on will no longer be on the table on July 5. Creditors' offer expires when the bailout does: June 30. Greek Finance Minister Yanis Varoufakis asked for a one-week extension at Saturday's eurogroup meeting, but they said no. Then they basically chucked him and scheduled a meeting for Eurogroup-Minus-Greece to "discuss the next steps." That probably shouldn't surprise, considering Syriza is campaigning for a "no" vote next Sunday. Why would the eurozone grant an extension to a program Greece's government is urging citizens to reject and clearly doesn't want?[x]

Meanwhile, Greek citizens spent most of last week lining up at banks and ATMs to withdraw whatever they could, in order to protect their savings from getting wiped out by Grexit and a forced conversion to devalued drachma. The ECB boosted emergency funding every day last week to help Greek banks battle the bank run, but after Tsipras' referendum bombshell, they announced they'd hold the line. Rumors of capital controls swirled all day Saturday[xi]. Varoufakis denounced those rumors via Twitter on Sunday: "Capital controls within a monetary union are a contradiction in terms. The Greek government opposes the very concept." But a few hours later, capital controls were in place: Banks and Greek stock markets are closed until July 7 at least, and the daily ATM withdrawal limit is at €60. Even with that, they're running low.

So to sum up, Greece's financial system is in limbo, its government has descended into chaos, and a few hours from now it will miss a debt payment with no bailout lifelines left. As we wrote last week, missing a payment due the IMF probably isn't a huge deal. Markets saw this one coming a mile away. Greece defaulted twice in 2012, with no ill effect globally. Granted, these were technically "voluntary" defaults, but if investors hadn't accepted Greece's offer to replace their bonds at a 70% principal reduction, collective action clauses would have forced the issue. This was the bond equivalent of "If you don't tender your resignation, you're fired." Missing the IMF payment isn't the same as defaulting on marketable debt, as it won't trigger a "default" rating from credit ratings agencies or CDS payouts. But missed principal is missed principal, and IMF head Christine Lagarde has said she'll consider Greece in arrears as soon as the on-time payment window closes.[xii] This is largely just a reputational risk for Greece, though. They were already borrowing from the IMF to pay the IMF. Now they can't borrow from the IMF, so they can't pay the IMF, and they go on the naughty list.[xiii]

Defaulting on the ECB next month would be a bigger deal, as that could impact the ECB's remaining Greek bank lifelines, though the ECB could also pull support before then-maybe as soon as Wednesday, when the bailout expires. Capital controls might delay the fallout for a while, but at some point, Greece will likely need to restructure its banking system. If they do that within the euro, the ECB's Single Resolution Mechanism will likely kick in, triggering Cyprus-style bail-ins and a lot of pain for large depositors. If they restructure after leaving the euro, all bets are off-nationalizations wouldn't surprise though.

As ever, no one can handicap what comes next. Most eurozone leaders are fed up and urging Tsipras to U-turn on the referendum, and resume negotiations just as former PM George Papandreou did in 2011. Judging from Tsipras' Twitter feed Monday afternoon, this is highly unlikely. If Greeks vote "no," Tsipras seems highly unlikely to get a better deal. Since the eurozone is fully backstopped, with very few Greek bonds owned by European banks, the urgency for compromise is fading. Yielding to Tsipras would enrage the euroskeptic parties in Germany, France, Austria, the Netherlands and pretty much everywhere else in the eurozone. It would also send an undesirable message to voters in Spain and Portugal, which hold elections later this year. Letting Greece walk, by contrast, would show voters electing anti-austerity parties isn't all it's cracked up to be and maintain domestic political harmony in Germany and elsewhere. A Grexit would look bad for EU leaders after five years of compromising and kicking the can, but at this point, that might cost German Chancellor Angela Merkel and the rest less political capital than surrendering to Tsipras.

But Greece could also vote "yes," and for what it's worth, polls show them leaning strongly that way. It would probably be the end of Syriza's government and Tsipras' political career-hard evidence voters no longer supported Syriza's platform. If they fall, Greece would probably get a caretaker government pending new elections-just as it did after Papandreou's government fell in 2011. A caretaker administration could reopen talks with creditors and get a new deal, and eurozone leaders say the door remains open as far as they're concerned. Though, we're also skeptical that would usher in a new era of calm and quiet, considering creditors had a heck of a time getting the prior, pro-euro/pro-austerity government to fulfill bailout conditions. A reset would keep Greece in the euro, but larger issues like debt relief would remain unsolved.

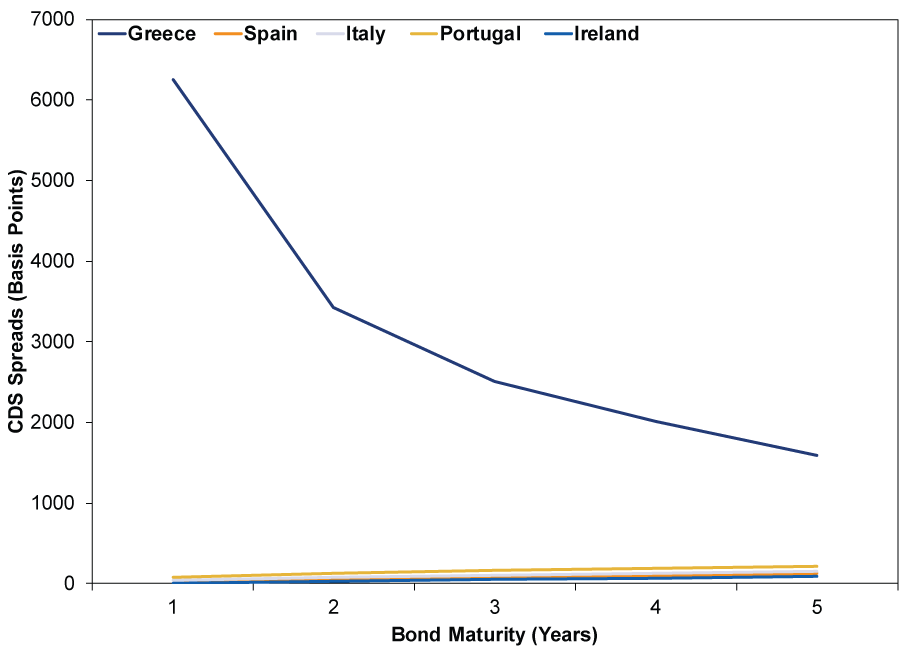

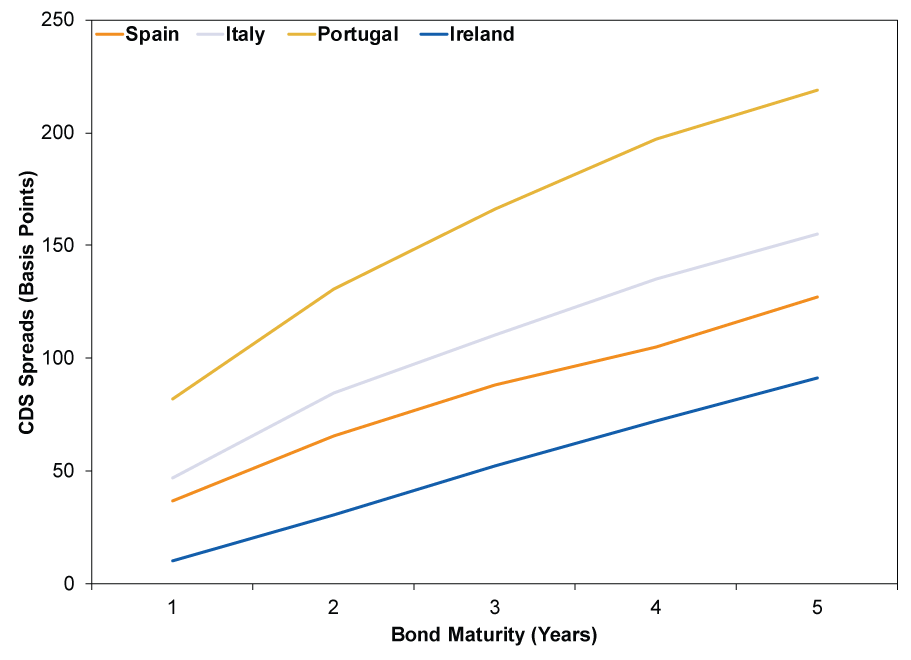

Volatility aside, markets still indicate the outcome isn't a swing factor outside of Greece. Italian, Spanish and Portuguese 10-year yields rose between 0.21 and 0.35 percentage point Monday in sympathy with Greek yields, which surged more than four percentage points, yet they remain near historic lows. CDS markets outside Greece also remain tame. Debt insurance costs in the rest of the periphery remain at rock-bottom levels (Exhibit 1). Greece's CDS curve is inverted-one-year CDS are far pricier than five-year CDS-implying investors (rightly) expect default in the very near term. The others' CDS curves are positively sloped (Exhibit 2), implying markets don't expect a credit event. That also seems about right to us. Default tends not to happen when borrowers can refinance debt at historically low interest rates. Italy, Spain and Portugal have refinanced a big chunk of debt on the cheap. Rates would have to soar to nosebleed levels-higher than 2011/2012-and stay there for these nations to lose market access. Possible, but unlikely, considering all have taken their medicine, unlike Greece.

Exhibit 1: Peripheral Eurozone CDS

Source: FactSet, as of 6/29/2015.

Exhibit 2: Spanish, Italian, Portuguese and Irish CDS

Source: FactSet, as of 6/29/2015.

For Greece, however, this is everything. Some have suggested Grexit means austerity ends swiftly, but that seems far-fetched. Greece would be shut out of capital markets and would thus have to balance the budget in a hurry or risk hyperinflation. Citizens will bear the brunt of it. Greece's national pension would be stuck with a boatload of Greek bonds, which it would probably swap for less valuable drachma-denominated bonds. Any Greek citizen that borrowed in euros from a foreign bank would be left holding the bag, unable to repay with devalued drachma. Steep recession[xiv] would ensue, as it almost always does after a country discards a currency peg. Eventually, devaluation probably would boost tourism and exports, and Greece could recover in a couple years, as some economists envision, but there is a lot of pain between now and then.

At this point, this isn't a global economic story anymore. It is a political story of an irrational government trying to fulfill untenable campaign pledges and negotiate on Twitter. It is a humanitarian story. And on those levels, it is gripping-we say that without a hint of schadenfreude. But as a global market risk story, Greece is as powerless as ever.

[i] We counted.

[ii] Certain Greek ETFs that trade on non-Greek exchanges fell by around -19%, so we would probably start imagining about there.

[iii] FactSet, as of 6/29/2015. Euro Stoxx 50, Italy's FTSE MIB and Spain's IBEX 35 daily price returns in EUR.

[iv] FactSet, as of 6/29/2015. France's CAC 40 and Germany's DAX daily price returns in EUR.

[v]He Tweeted it too: "Having asphyxiated banks & denied extension request, is it reasonable to expect that IMF installment will be paid tomorrow? #ert #Greece"

[vi] FactSet, as of 6/29/2015. S&P 500 Index daily price return.

[vii] Pun intended.

[viii] So you have to wonder: Would we be writing any of this if the markup appeared in one of Word's alternate colors, like fuchsia or aqua?

[ix] You may as well call this a Greferendum on Greform.

[x] The other issue here, which is entirely sociological but fascinating all the same, is that the referendum might well violate Greece's constitution. Bloomberg's Leonid Bershidsky has the full scoop on that.

[xi] Tsipras tried to ease his people's jitters via-what else-Twitter. First he pleaded for "patience and composure," promising "the bank deposits of the Greek people are fully secure. Then, for good measure, he went all FDR, and the Twitterverse peanut gallery did not respond kindly.

[xii] So much for arcane IMF procedures that insert a 30-day lag time between the missed payment and the official "in arrears" designation-it is still a thing, in theory, but no one could pretend Lagarde wouldn't be aware Greece missed a payment until July 30.

[xiii] We'll let others run with the ridiculous comparisons between Greece and the rest of the naughty list.

[xiv] Grecession? Or is that too soon?

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis The New Tariffs in Town Are Still Old News2026-07-24

-

Expert Commentary This Week in Review | Market Volatility, Tariffs, SpaceX

2026-07-24

2026-07-24 -

Expert Commentary Why Ken Fisher Is Optimistic About European Stocks

2026-07-23

2026-07-23 -

Economics A Summertime Check-in on US Consumers2026-07-23

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today