Personal Wealth Management / Politics

On the Senate’s Busy Week

A seeming legislative flurry is capturing investors’ attention.

Where did gridlock go? That is the question many are asking after a flurry of Senate activity this week. On Tuesday, a bipartisan majority passed the Chips and Science Act, a $280 billion package pitched as a solution for the semiconductor shortage and concerns about China’s potential influence over global chip supply—which the House passed and sent on to President Joe Biden’s desk on Thursday. Separately, on Wednesday, the budget reconciliation bill once known as Build Back Better returned from the dead, slimmed down and renamed the Inflation Reduction Act.[i] It hasn’t yet passed and may not, but we see this as a textbook case of how markets and politics typically intersect in the first half or so of a midterm election year—and we think it points further toward a late-year rally as midterm results zap lingering fears of big legislation.

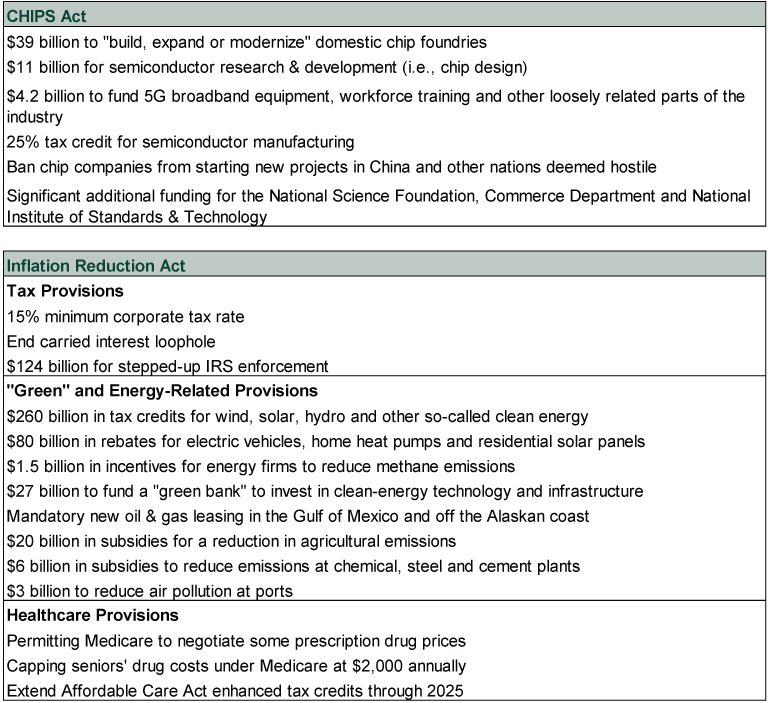

Exhibit 1 shows a high-level look at what is in each bill at the moment, pending committee and both chambers’ votes and possible reconciliation on the Inflation Reduction Act. The provisions could change, but for now, here is how things stand.

Exhibit 1: New Legislation at a Glance

Source: United States Senate, Reuters and The Washington Post, as of 7/28/2022.

We have long observed that people have a natural impulse to parse legislation for provisions that are “good” and “bad” for markets and then see where the balance lies. In our view, this is misguided for a few reasons. One, “good” and “bad” are opinions—too often informed by political biases, which create huge blind spots. Some might consider the Inflation Reduction Act’s efforts to reduce the federal deficit as “good,” seeing deficits as inflationary. Others might consider those same efforts “bad” because they include a corporate tax hike, which could detract from wages and earnings. Some might laud all the spending on wind, solar and other climate-related items as stimulus with long-term societal benefits. Others might see the spending as inefficient and misguided, citing the inefficiency of wind and solar as well as the possible impact of forced change in creating vast winners and losers, like the companies benefiting big from Britain’s subsidized heat pump installation and Dutch nitrogen emissions targets farmers fear will hammer them.[ii]

We would classify the vast majority of these takes as sociology—items that are worth considering from a societal standpoint, but likely outside markets’ sphere. That obviously doesn’t apply to the pure financial provisions, namely the corporate tax changes, but even there, it isn’t as simple as “good” and “bad.” Rather, we see the important questions as, to what extent were changes already priced in? Are they vast enough to discourage investment? If they are a negative, are they big enough to offset the other positive drivers? And, most importantly, what is the likelihood this actually passes?

Even with one-time holdout Senator Joe Manchin (D-WV) signing on to the package, its success isn’t guaranteed. The Senate Parliamentarian has yet to deem it eligible for the budget reconciliation process, which would enable it to pass on party lines. If it clears that hurdle, passage would require unanimity among Democratic senators, and fellow centrist Democrat Kyrsten Sinema (AZ) hasn’t yet tipped which way she is leaning. Additionally, the bill may prove too moderate for the party’s progressive caucus, which—like its ultra free-market counterpart in the Republican Party—has occasionally rejected bills that don’t pass ideological purity tests. Some House Democrats, for example, have long said they won’t agree to measures including tax changes that don’t repeal the State and Local Tax deduction limits enacted in 2017’s reform. Those aren’t in the new bill, raising questions about their support. But overall, we don’t see either of these bills as big, surprising negatives or positives for stocks—both have very limited surprise power for good or ill. Their potential winners and losers are well known.

However, we see positive implications for stocks looking ahead. Neither the CHIPS Act’s passage nor the Inflation Reduction Act’s reappearance means gridlock has suddenly vanished. Gridlock doesn’t mean nothing passes. Rather, it means that whatever does pass tends to be watered down greatly from original proposals. Here, too, consider the Inflation Reduction Act and, specifically, the things it doesn’t include: There are no wealth taxes or taxes on unrealized capital gains. There is no surtax on high incomes. The vast majority of the social programs originally in Build Back Better are absent. The price tag isn’t $3 trillion. Instead, it focuses on so-called green energy, emissions, prescription drug prices and Affordable Care Act subsidies, while limiting tax increases to the 15% minimum corporate tax rate, increasing the IRS’s enforcement budget and ending the long-running carried interest loophole that private equity and hedge funds have enjoyed. All of these items have been batted around for years and their potential plusses and minuses have been discussed ad infinitum. In our view, they are long since out of surprise power. If anything, passing the bill would end the uncertainty and let markets move on.

That last bit—uncertainty—is the key consideration here. In our view, legislative uncertainty has been one of the many items weighing on sentiment this year, as it often does in the first half of a midterm year. Even as people saw intraparty gridlock stalling flagship bills, they worried something could still squeak through. Now they are getting clarity, which can help jitters ease. Midterms should accelerate this process, as Republicans look likely to take the House and could even take the Senate by a hair’s breadth, depending on how the handful of races in swing states progress. We don’t prefer either party over the other, and neither do stocks. But removing Congress and the White House from single-party control, regardless of which party it is, brings the traditional, highly visible form of gridlock that relieves investors’ legislative risk aversion. As the current stealthy intraparty gridlock gives way to its more visible sibling, investor sentiment should get a big lift.

We think that is about the extent of the market impact here. Neither bill looks likely to help with inflation much, considering the looooong lead time for constructing a semiconductor foundry and, despite politicians’ claims, the Inflation Reduction Act’s measures targeting energy prices won’t much affect supply and demand in the near term. Major chip producers were already implementing huge investments without the feds’ help, and additional outlays won’t bear fruit for many years—beyond stocks’ time horizon. Letting Medicare negotiate prescription drug prices could create some winners and losers in the Health Care sector, but with these changes in the pipeline for years, we suspect the impact is largely priced in at this point.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Economics A Summertime Check-in on US Consumers2026-07-23

-

Expert Commentary Why Ken Fisher Is Optimistic About European Stocks

2026-07-23

2026-07-23 -

Politics Blunting Burnham?2026-07-21

-

Market Analysis Why the SOX “Bear Market” Isn’t Foreboding2026-07-21

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today