Personal Wealth Management / Market Analysis

OPEC Stays Put—Will US Shale Take a Hit?

Will OPEC's decision not to reduce its output negatively impact US shale producers?

Thursday, in a widely watched meeting, the Organization of the Petroleum Exporting Countries (OPEC) announced its production ceiling would remain at 30 million barrels per day. Oil prices plunged-a reaction suggesting recent movement owes more to quick supply growth than faltering demand (which we discussed here). Headlines reacted by citing some obvious factoids most folks following this story were probably attuned to already: Lower prices create some losers, mostly oil exploration and production firms and countries that rely on higher prices to keep the lights on (Venezuela, Nigeria, Iran, Russia, Brazil, Ecuador, etc.). As for the winners? Allegedly retailers. Energy importers like Japan and much of Europe. But the major thrust in the press seems to be speculation regarding what sharply falling oil prices mean for US shale oil output. In our view: OPEC's decision likely doesn't have as great an impact on US shale production as many believe, at least not in the short run.

Most seem convinced OPEC keeping production high in spite of recently weak prices is a move seeking to maintain the cartel's market share, threatened by the huge surge in non-OPEC production in recent years. Consider: The added production of the US alone exceeds every OPEC nation's output except Saudi Arabia. But many presume US shale production-the nexus of rising US output-requires higher oil prices to be profitable. Hence, declining prices supposedly threaten US production.

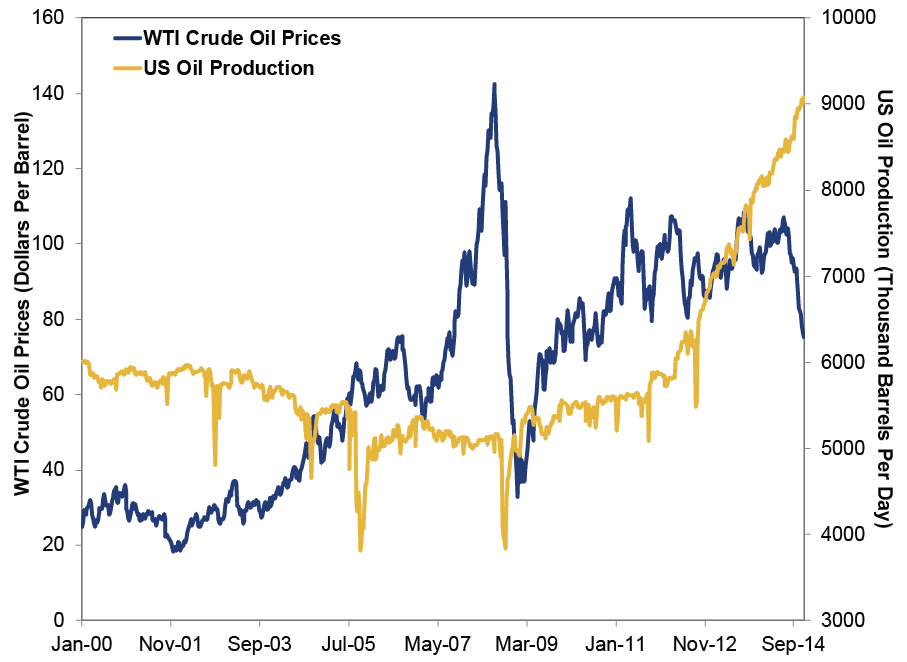

While there could be some impact on marginal producers in higher cost regions-and new well drilling could slow as a result-we're skeptical output would plummet in the near term. Oil prices have fallen over the past several months, but US production has continued climbing. (Exhibit 1)

Exhibit 1: Weekly US Oil Production and West Texas Intermediate (WTI) Crude Oil Prices

Source: St. Louis Federal Reserve, as of 11/28/2014. Weekly WTI Crude Oil Prices, 1/7/2000 - 11/21/2014. US Energy Information Administration (EIA), as of 11/28/2014. Weekly US Crude Oil Production, 1/7/2000 - 11/21/2014.

Now, that doesn't automatically mean sunshine and rainbows ahead for US oil production-but there are several factors that point to continued growth. For starters, since shale companies' costs are largely already in the ground-they've invested a lot of capital-it doesn't make sense to immediately take projects offline. Especially considering how many projects' breakeven point-the oil price point where losses flip to profits-remains below current oil prices (West Texas Intermediate (WTI) crude slumped to $69.00 on Monday).[i]According to the US Energy Information Administration (EIA), only about 4% of US shale output has a breakeven point of $80 per barrel or higher. The breakeven for most of North Dakota's Bakken region-one of only 10 oilfields worldwide with daily output over one million barrels and almost 13% of total US production-is around $42.[ii]According to this chart from Citigroup, most US shale regions have breakeven points below today's oil prices. And this mind-melting chart, which lists every shale project in the world, further highlights the point. While some shale producers could take a hit, it seems most shale regions expect to be in the black despite falling prices.

Why? Hydraulic fracturing technology and techniques are improving, allowing for greater efficiency and cost saving. Techniques such as pad drilling (drilling multiple wells from one rig location) are becoming more widespread. Some estimate pad drilling alone saves producers as much as $500,000 in up-front drilling costs per well, a 10% - 15% savings. In addition, fully assembled rigs can now move from one location to another-a vast difference from years earlier, when moving even just a few yards would require disassembly and reassembly. As a result, oil rigs tend to yield more output than they did in the past. Companies are also continuously testing other new technologies-like coil tubing-to enhance drilling efficiency. And they are putting more emphasis on the post-drilling phase-with techniques like multi-stage fracturing-to minimize the time it takes to transform a drilled well into an oil producer.

There is plenty of potential for shale extraction to become even more streamlined-these firms are highly motivated to stay profitable. Firms are also managing costs where they can. Some are pumping more from their top properties and dropping their less-efficient projects, maintaining output while managing costs. Others are shelving plans to increase rig count.[iii] Companies' efforts to cut costs here and there could slow production growth some-but that differs considerably from yanking projects wholesale, slashing production outright. Overall, it seems shale producers are finding ways to continue pumping oil despite low prices.

Now, if prices continue falling and stay down, we could see a change in US oil output. Prices are a signal to producers, and sustained low prices in the 1980s and 1990s drove years of declining US production. But it took years of prices between $10 and $30 to stymie investment. We're nowhere near those levels today, even when you factor in inflation. Anything is possible, but, in our view, it's premature to think the relatively recent oil price slide will overwhelmingly hurt US shale producers over the foreseeable future.

Stock Market Outlook

Like what you read? Interested in market analysis for your portfolio? Why not download our in-depth analysis of current investing conditions and our forecast for the period ahead. Our latest report looks at key stock market drivers including market, political, and economic factors.

[i] FactSet, as of 12/2/2014. Daily WTI Crude Oil Price (Dollars Per Barrel), 12/1/2014.

[ii] EIA, as of 11/28/2014. Total oil production for US and Bakken Region was 8,864 and 1,134 (thousand barrels per day), respectively, in September 2014.

[iii]But rig count doesn't necessarily equal output direction.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets — August 3 - August 72026-08-11

-

Expert Commentary 3 Things You Need to Know This Week | US Inflation, UK GDP, RBA

2026-08-10

2026-08-10 -

Market Analysis Four Overlooked Costs With Dividends2026-08-10

-

Market Analysis Rechewing Fed Independence Fears2026-08-10

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today