Personal Wealth Management / Market Analysis

Our July Fed Meeting Preview

The yield curve has flattened lately. What next?

The next Fed meeting is less than a week away, and most analysts are penciling in another steep rate hike. Almost no one expects this to do anything about inflation, given the Fed can’t refine petroleum into gasoline, increase the grain harvest, staff airlines or unload container ships, all of which have fueled accelerating inflation even as money supply has started rolling over. But there is mounting fear that even one more big rate hike could be overshooting and kneecapping the economy, especially given how much the yield curve has flattened in recent weeks. In our view, there is some risk of the yield curve inverting, but it isn’t a given—and even a mild inversion isn’t an automatic recession trigger.

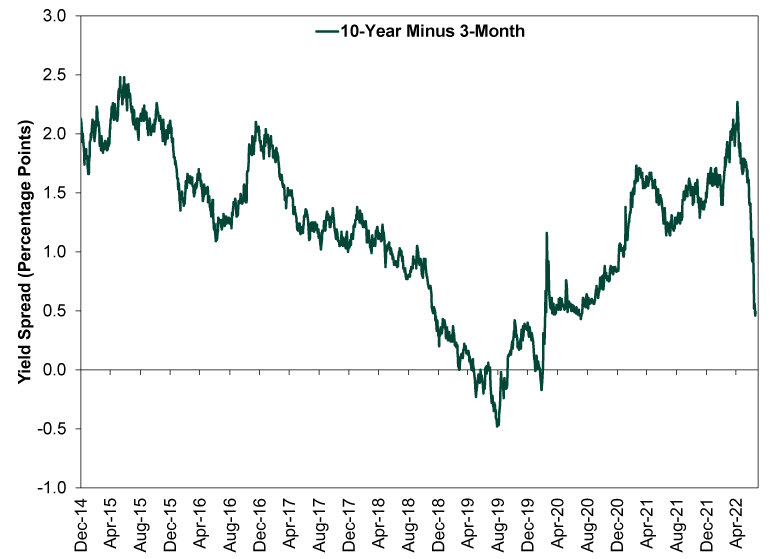

Now, when we look at the yield curve, we don’t use the 2-to-10 year segment that gets most pundits’ attention of late. We think the yield curve’s importance comes from its relationship with banks’ funding costs (short-term rates) and loan revenues (long-term rates), with the spread between them influencing banks’ potential profit margins on new loans—which drives loan growth. Generally, a wide spread means big profits and aggressive lending, while a deeply negative spread can signal a credit crunch. Banks don’t get much funding through 2-year CDs. They fund primarily through retail deposits and interbank markets, which are much shorter-term. We think the 3-month Treasury yield is a better approximation, so we use the 3-month to 10-year yield spread. That spread, as Exhibit 1 shows, has narrowed sharply since early May, from over two full percentage points (a multiyear high) to roughly half a point as of Tuesday’s close.

Exhibit 1: The Rapidly Shrinking Yield Curve Spread

Source: FactSet, as of 7/20/2022. 10-year and 3-month constant maturity US Treasury yields, 12/31/2014 – 7/19/2022.

The flattening has come largely at the short end of the curve. The 10-year yield is down just 0.11 percentage point since the spread peaked, albeit with some big volatility along the way—it closed May 6 at 3.12%, spiked to 3.49% on June 14 and closed Tuesday at 3.01%.[i] Meanwhile, 3-month yields have jumped from 0.85% on May 6 to 2.52% now.[ii]

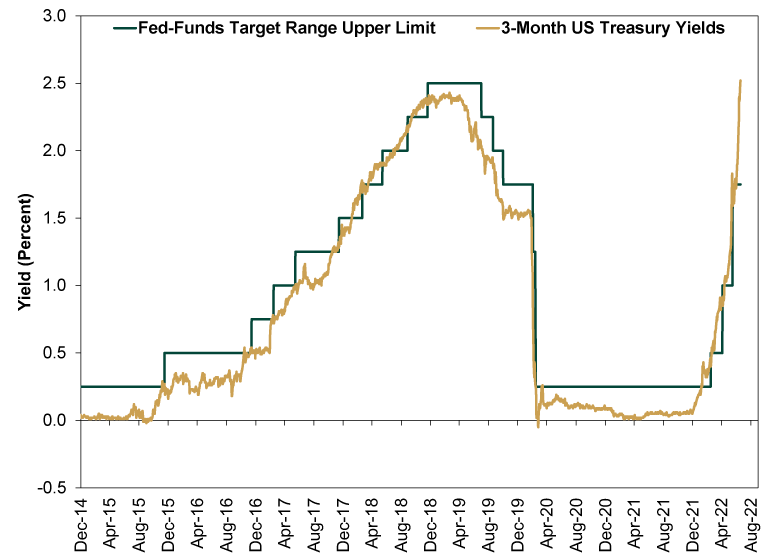

Incidentally, 2.5% is where the upper bound of the fed-funds target range would be if the Fed were to make a 0.75 percentage point rate hike next week—a strong indication that the move is already priced in. It would be very strange if it weren’t, given how much chatter there has been. Markets are efficient, and they are highly likely to reflect commonplace opinions about what may happen in the near future. Plus, as Exhibit 2 shows, 3-month yields have had a strong tendency to move ahead of the Fed.

Exhibit 2: The Prescient 3-Month Treasury Yield

Source: FactSet, as of 7/20/2022. Fed-funds target rate upper bound and 3-month constant maturity US Treasury yield, 12/31/2014 – 7/19/2022.

So it is far from certain that one big rate hike will be enough to invert the curve next week. It is possible, if expectations for more hikes mount—or if inflation expectations drop. But not automatic.

Still, it is worth considering what a shallow inversion would mean—and we see two big reasons it wouldn’t be a recession trigger. For one, note that we said earlier the yield curve influences banks’ costs and revenues—we didn’t say they were identical. The yield curve merely points to potential changes in the banking world. These days, the signal isn’t that strong. Frustratingly, the average national deposit rate, according to the FDIC, is 0.10% thanks to an astronomical deposit glut.[iii] Meanwhile, the prime loan rate is 4.75% and the average 30-year fixed mortgage rate is 5.5%.[iv] These numbers aren’t consistent with a credit crunch that would force businesses to get lean and mean to survive a funding freeze.

Two, money doesn’t care about borders. Banks can borrow in one country, lend in another and hedge for currency risk with minimal hassle, arbitraging rate differences globally. The US has some of the developed world’s highest rates right now, so it could be very attractive to borrow cheaper in Continental Europe or Japan and lend here. If global money supply contracted sharply, limiting the amount of money able to flock here to take advantage of higher rates, then that would be one thing. But central banks outside the US aren’t mopping up reserves to a great degree. Nor is the global GDP-weighted yield curve flirting with a meaningful inversion.

Finally, it is worth noting that the yield curve isn’t a trigger. It is true that the yield curve often inverts before recessions, but the lag is quite variable. Bear markets often precede recessions, too, so even if the yield curve is indicating a recession, how much of that weakness is already reflected in stocks? Probably quite a lot, in our view, given the ubiquitous headlines exploring the concept.

We aren’t calling the yield curve meaningless. A deep US inversion with parallel moves globally would be cause for concern. But we aren’t there yet, and there isn’t a high probability it is imminent. So while we may get a shallow recession due to all this year’s supply disruptions, the likelihood that spirals due to a Fed-induced credit crunch seems remote for now.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets — July 27 - July 312026-08-03

-

Expert Commentary 3 Things You Need to Know This Week | US Jobs, Trade Balance, Earnings Reports

2026-08-03

2026-08-03 -

Market Analysis Digging Into Last Week’s Fed ‘Credibility’ Concerns2026-08-03

-

Expert Commentary This Week in Review | Fed Meeting, US GDP, Eurozone GDP

2026-07-31

2026-07-31

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today