Personal Wealth Management / Politics

Our Perspective as Russia Saber-Rattles in Ukraine—Again

Fear of regional conflict can stoke volatility, but stocks typically move on quickly.

Buckle up. Satellite images show Russian troops are amassing along the border with Ukraine, and the US has reportedly warned European allies that an invasion is possible. NATO announced its solidarity with Ukraine Monday, raising the perceived risk of Western nations getting dragged into the conflict despite Ukraine not being a NATO member. We have already seen a few articles warning an invasion and conflict would bring terrible consequences for the global economy and stocks, and if tensions ratchet up, those warnings will probably get louder and more widespread. Steel yourself against the associated fear now: Market history overwhelmingly shows regional conflict is highly unlikely to cause a bear market (typically a deep, lasting decline of -20% or worse with an identifiable fundamental cause). So while fighting is tragic, and potentially a cause for near-term volatility, we think it is a mistake to overrate the threat to stocks.

Now, of course, we aren’t in the intelligence community and have no access to “President” Vladimir Putin’s plans. This may be all a bluff. It may be yet another move designed to goad the EU into approving the Nord Stream 2 gas pipeline that bypasses Ukraine. But in the event Russia does invade Ukraine, remember: Markets have sadly dealt with a number of regional conflicts and potential conflicts in recent years. The list is long. The first Gulf War and Bosnian War in the 1990s. US-led intervention in Afghanistan and Iraq and the Hezbollah/Israel dust-up in the 2000s. Libya and Syria in the 2010s. Russia and Ukraine in 2014 over the former’s annexation of Crimea and meddling in eastern Ukraine—and a host of others. In general, if stocks registered the strife at all, they followed the same general trajectory: negativity as tensions escalated and armed conflict became an increasingly realistic possibility, then a recovery as the endgame became clear.

In cases where the endgame was armed conflict, that recovery typically arrived as or just after the fighting broke out. Not because regional war is bullish, but because the fighting ended the uncertainty over whether saber-rattling would spiral into military action. It ceased the will-they-or-won’t-they and let investors weigh the conflict’s reach. In all these cases, even when major powers were involved, the conflict occurred on a very small swath of the global economy, with no impact on commerce in the developed world or major Emerging Markets. That clarity enabled markets to move on quickly. Exhibits 1 and 2 detail two examples.

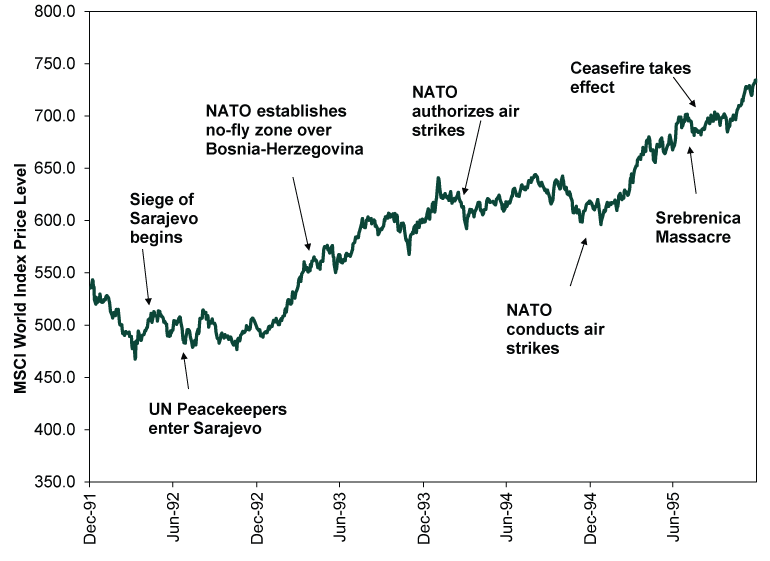

Exhibit 1: Stocks and the Bosnian War

Source: FactSet, as of 11/16/2021. MSCI World Index Price Level, 12/31/1991 – 12/31/1995.

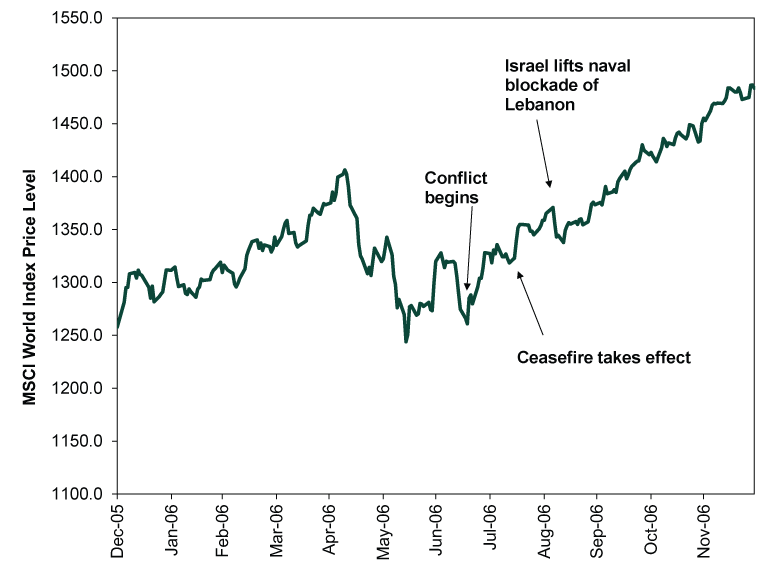

Exhibit 2: Stocks and the Israel/Hezbollah Conflict

Source: FactSet, as of 11/16/2021. MSCI World Index Price Level, 12/31/2005 – 12/31/2006.

Since good stock market data begin in 1925, only one conflict has been a bear market’s proximate cause: World War II. Only that war had a big enough footprint to wipe out a significant amount of economic activity. In 1939, when Nazi Germany’s adventurism in Continental Europe began, stocks appeared to be recovering from the bear market that began back in 1937. But Hitler’s seizure of the Sudetenland (then Czechoslovakian territory) stopped that rally in its tracks, as it forced Europe to confront the full extent of Hitler’s territorial ambitions. Stocks fell sharply as Hitler turned his focus toward Poland. When Germany did actually invade the country—and France and Britain declared war—the S&P 500 soared. The uncertainty of a failed attempt to appease Hitler was over.

Stocks headed mostly sideways for several months thereafter. But when France fell in May 1940—a surprise—the bottom fell out. The bear market continued throughout 1940 and 1941 as fighting ranged across multiple theatres. Yet a new bull market began in 1942, three years before the war’s end, as stocks learned to live with the status quo and looked ahead to a time when the global conflict was over.

So when assessing conflict as a market risk, we think it is best to think coldly and critically. Leave out feelings about the human toll. Focus on a simple question: What is the likelihood that, if fighting breaks out, it affects a large enough share of global GDP to cause a recession? Ukraine’s GDP hit $155.6 billion last year.[i] Global GDP hit $84.6 trillion.[ii] With a t-r. Ukraine is just 0.2% of world output. A global recession would need a much bigger hit, to the tune of a few trillion dollars. Even if NATO members did join the fray, as long as the fighting stayed concentrated in one pocket of Eastern Europe and didn’t engulf the entire Continent, stocks would likely move on relatively quickly—much as they did when Russia annexed Ukrainian territory in 2014.

Some analysts argue oil and gas make this time different. Russia is one of the main energy suppliers to Continental Europe, potentially making Europe’s energy supply one of the main casualties of a Russian attack, either because of European sanctions or Russian flexing. This, pundits argue, would cause an energy price spike dwarfing what the world endured in October, causing a global energy and financial crisis. We guess we can put this in the realm of the possible, but we don’t think it is automatic or even likely.

For one, consider incentives. Russian government revenues depend on strong oil and gas royalties. If Russia stopped selling oil and gas to international clients, it would drain state coffers and bring economic instability, which puts Putin’s time in office at risk. So while it could be disruptive in the near term if Russia cut gas supplies to Europe, there is a pretty large short-term incentive not to do so.

In the medium to longer term, if Russia stopped selling to Europe, global supply lines would adjust. Europe would find new suppliers. How long this would take isn’t totally clear, but in time, high prices would encourage even more production in the US, Canada, Brazil and North Africa. Russia would likely have to find new buyers if interruptions persisted for long enough.

So keep an eye on Russia and Ukraine, and mentally prepare yourself in case there is volatility, should conflict materialize. Even if it never arrives, it is always better to be ready than caught off guard. But don’t let regional war and rumors of war deter you from your long-term investment strategy. History shows you are overwhelmingly more likely to miss a bull market than avoid a decline if you do so.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis Quick Hit: The July Jobs Nothingburger2026-08-07

-

Expert Commentary This Week in Review | Record Highs, US Jobs, Yen Intervention

2026-08-07

2026-08-07 -

Market Analysis Western Oil and Gas Producers Are Ramping Up2026-08-06

-

Politics The Tenth Question Facing Alberta2026-08-06

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today