Personal Wealth Management / Market Analysis

Our Perspective on Britain’s Oil and Gas ‘Windfall Profit’ Tax

Windfall profit taxes have landed in Britain, but the market impact seems minimal.

Editors’ note: MarketMinder is politically agnostic—we aren’t for or against any party, politician or policy. Our analysis seeks only to determine political actions’ potential economic and market impact.

Thursday, bowing to public pressure, Prime Minister Boris Johnson’s government seemingly reversed a late-March decision and announced it would impose a 25% windfall profit tax on oil and gas firms—that is, it raised the tax rate on their profits from 40% to 65% temporarily, starting May 26. Perhaps it was rising prices’ impact on the voting public that changed their minds. Maybe political winds shifted amid the Partygate investigation’s release, sapping support for Johnson’s ruling Conservative Party. Maybe it was some of each. Regardless, for markets, windfall taxes aren’t great—especially for the UK’s Energy sector. But it is small in scope when viewed globally—and smaller than originally feared in Britain, which likely limits its impact.

UK Chancellor of the Exchequer Rishi Sunak designed the energy levy to fund subsidies for households facing higher energy bills as rising energy prices force Britain to ratchet up its price caps. That already happened once in April, and now energy regulator Ofgem has warned of a 40% hike looming in October—so the popularity of such a measure is understandable. Although we sympathize with households’ plight, we don’t think redirecting the Energy sector’s profits is necessarily the best way to alleviate energy price pressures.

A windfall tax discourages investment in increased output—a key to mitigating rising prices. The Energy business is highly cyclical, meaning it is prone to booms on the upswing—like now—but also busts during downturns. Years of plenty often precede prolonged profit droughts, such as during 2014 – 2016’s oil price collapse, from which the sector is only now recovering. When profits are high, companies not only boost output, they repair their balance sheets for when times are lean. We think windfall taxes limit firms’ flexibility and potentially reduces their longer-term resiliency. Note that the new tax expressly forbids firms from using past losses to reduce their windfall tax bill, which we think deprives businesses of a crucial strategy to maintain stability over time. If more capacity is the real solution, as we think it is, we fail to see how a windfall tax is a step in that direction.

The windfall tax does provide an 80% investment allowance, so companies can reduce their liability by directing profits to capital expenditures in UK oil and gas production, blunting the effect. But less of a blow is still a blow. There wasn’t a disincentive before, and now there is. Companies invest to boost profits, so forcing them to channel that in a particular direction is a headwind, if a smaller one than an unmitigated windfall profit tax. Two large Energy firms have already warned that they are re-evaluating their planned North Sea oil and gas investments as a result of the change.

Sunak bills the windfall tax as “timely, targeted and temporary,” but how long it will last isn't exactly clear.[i] The legislation includes a clause sunsetting the tax in December 2025, but the government’s official proposal mentions ending the tax sooner “if oil and gas prices return to historically more normal levels.” Then, too, a key uncertainty hanging over markets was whether levies would include electrical power generators. Sunak spared them, helping clear up some uncertainty—but he left the door open to the windfall tax’s expansion.

All that said, we don’t think this is a huge negative. Sunak expects the plan to raise around £5 billion this year, and while that might take a good chunk from UK Energy—about a fifth of last year’s roughly £25 billion in profits—analyst estimates still project the sector to double after-tax profits this year.[ii] Besides, we think markets have largely pre-priced the hit already—it looks mostly like a one-off flesh wound than a longstanding headwind.

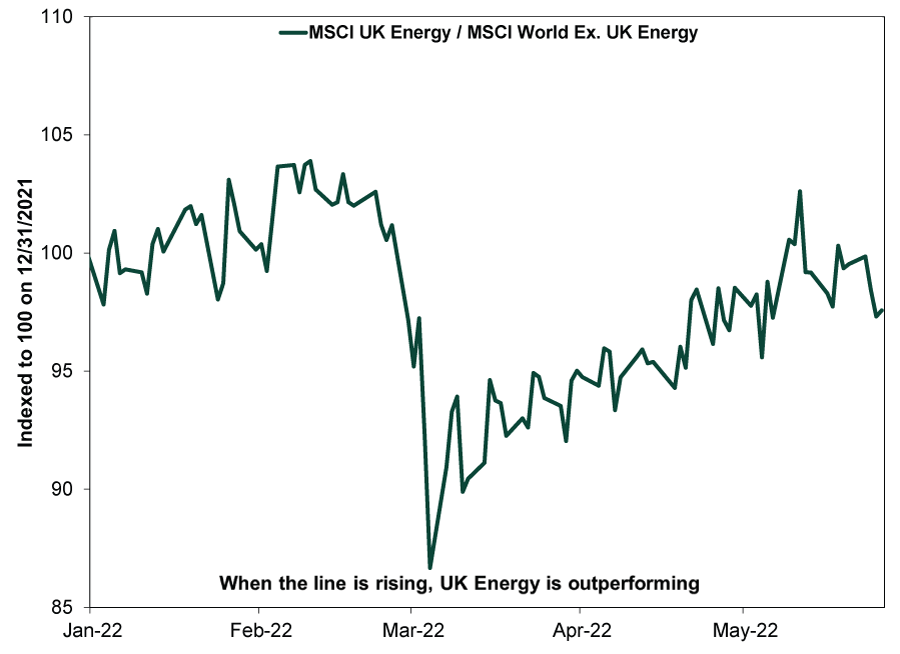

UK Energy stocks, like the rest of the world’s, have been on a tear this year. So to see the UK tax's possible market impact, consider Exhibit 1, which shows the MSCI UK Energy Index's returns relative to developed world Energy stocks outside the UK. When the line is rising, UK Energy stocks are outperforming the rest of the world’s. We wouldn't read too much into short-term moves, but late-February/early-March windfall tax talk seemed to hit UK Energy sentiment then. For example, on March 2, Spain extended its windfall tax, introduced last September, by six months. This came as speculation swirled of a potential UK windfall levy, with the UK’s main opposition Labour Party pushing for it.

Exhibit 1: Windfall Taxes Seem to Hit Sentiment

Source: FactSet, as of 5/27/2022. MSCI UK Energy relative to MSCI World ex. UK Energy returns with net dividends, 12/31/2021 – 5/26/2022.

But by March’s end, the UK had seemingly ruled out a tax. Causation is open to interpretation, but UK Energy appeared to enjoy a relative recovery through early May. Since then, however, its lag suggested uncertainty over a possible UK policy U-turn, which Thursday’s announcement confirmed.

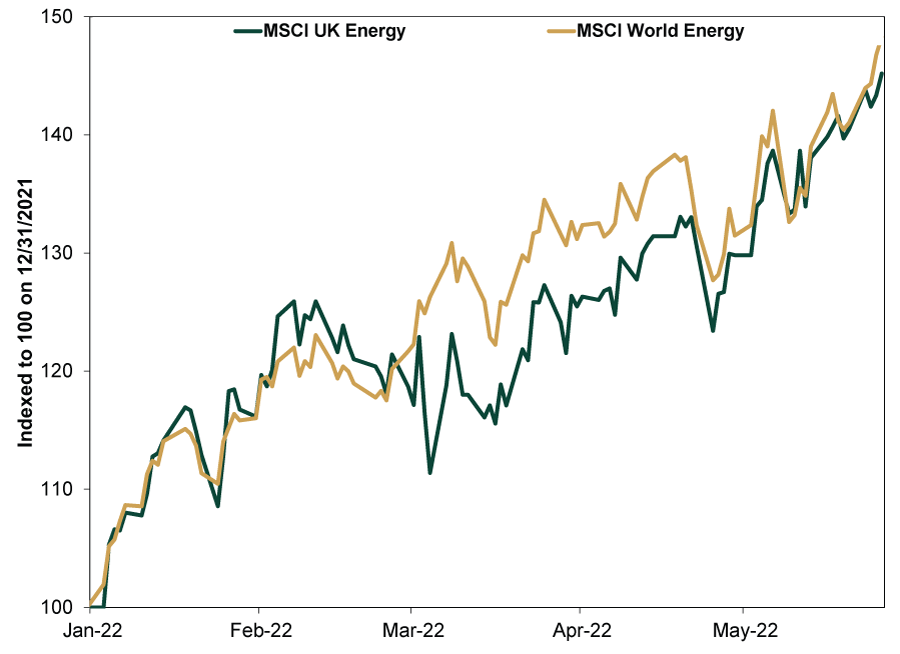

In the grand scheme of things, though, the UK’s windfall tax looks more like political theater than a punch. Despite some sentiment-driven market impact, it seems mostly a sideshow. Exhibit 2 shows UK Energy returns next to World Energy. Taxing “extraordinary” profits may make sense politically—and that appears to be shading UK Energy returns down a tad—but you have to squint to see it. Tax uncertainty appears negligible next to Energy’s main fundamental earnings drivers—oil prices and the global supply and demand behind them—which propelled the sector higher this year as energy costs spiked more than many expected.

Exhibit 2: Fundamentals Matter More

Source: FactSet, as of 5/27/2022. MSCI UK Energy and World Energy returns with net dividends, 12/31/2021 – 5/26/2022.

Just as windfall taxes aren’t likely to suppress UK Energy much, they aren’t broad enough to hit global markets, either. UK oil and gas output is only about 1% of the world’s—not huge.[iii] Similar measures from Spain and Italy made fewer ripples, with affected companies not seeing a material impact.[iv] Meanwhile, Emerging Market Hungary announced windfall taxes Thursday, too, affecting much broader swaths of its markets—including banks, telecom firms, retailers and airlines, along with Energy firms—unnerving investors there. We are watching for any wider spread. But while these moves aren’t good, in our view, their scope and effect seem too small to cause bigger global waves for now.

[i] “UK Slaps 25% Windfall Tax on Profits of Oil and Gas Firms,” Joe Mayes, Bloomberg, 5/26/2022.

[ii] “UK Hits Oil and Gas Companies With $6 Billion Windfall Tax,” Anna Cooban, CNN, 5/26/2022. Source: FactSet, as of 5/27/2022. MSCI UK Energy EPS estimates, 2021 – 2022.

[iii] Source: EIA, as of 5/27/2022.

[iv] “Enel Shrugs off Windfall Tax Impact to Confirm 2022 Forecast,” Stephen Jewkes, Reuters, 5/4/2022.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Economics Q2 US GDP’s Stealthy Strength2026-07-31

-

Expert Commentary This Week in Review | Fed Meeting, US GDP, Eurozone GDP

2026-07-31

2026-07-31 -

Market Analysis Don’t Fret the EU’s Low Summertime Gas Storage Levels2026-07-31

-

Economics On Fires and GDP2026-07-30

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today