Personal Wealth Management /

P/Es: Still Not Predictive After All These Years

Basing portfolio decisions on valuations may intuitively seem right, but markets are frequently counterintuitive.

15.3.[i] That’s the forward 12-month S&P 500 price-to-earnings ratio (P/E) as of April 30, 2014. Only a hair above its level on September 16, 2009. Stocks valued like they were in the early days of this big, US-led bull market? Bullish, right?! Yet oddly, that’s not quite how media chooses to see valuations today. Most seem to see it as a call to either underweight US stocks or run for your bubble bunker. So which is it? Are equity valuations today bullish or bearish? Answer: Neither. P/Es—no matter how you slice, dice and splice the data—are of little use in forecasting market conditions. Constantly seeking low valuations in markets is a fallacy.

Sound startling? We understand. It seems intuitive that valuations should matter for stocks’ directionality. After all, what can be more fundamental to a private business than profits? And as an investor, you’re buying a small slice of ownership in a business. How the business’s share price relates to those earnings would seem like a fair way to judge whether investors are paying too much (the stock is “overvalued”) or too little (“undervalued”). Yet markets are often counterintuitive.

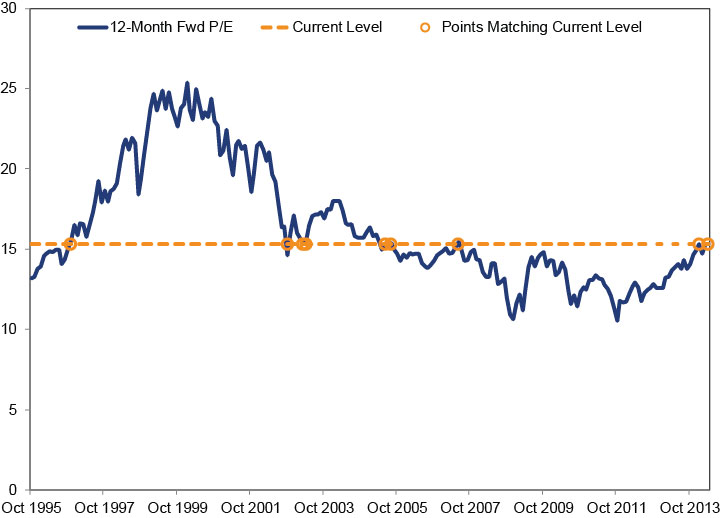

The current P/E is neither unprecedented nor especially high by historical standards. Exhibit 1 shows the S&P 500’s Forward P/E since 1995, with levels within a rounding error of today’s circled. The first occurs in 1996. About three and a half years of strong bull market (and much higher P/Es) followed. The next three are at the tail end of a bear market—fairly close to the bottom. There are several in 2004, then one in 2007. There, 15.3 seems right around the top of the market. So the same level occurs in the middle, at the bottom, in the middle and at the top of the market cycle. Random—which, in isolation, tells you nothing about what comes next. This isn’t unique to this particular reading or forward P/Es.

Exhibit 1: S&P 500 Forward 12-Month P/E Ratios

Source: FactSet, monthly 12-month forward P/E ratios, September 1995 – April 2014.

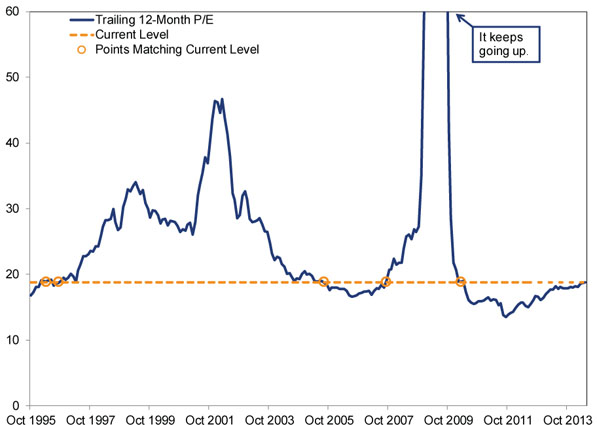

Some suggest forward 12-month P/Es aren’t the right measure, instead pointing to trailing 12-month P/Es—real earnings figures, not analysts’ projections. But those real figures are all from the past, which lacks predictive quality, too. A quick peek at Exhibit 2 should suffice to show the present 18.8 reading isn’t predictive. Similar readings have occurred at five points since 1995. The pattern isn’t stocks progressing from super cheap to super expensive—again, not intuitive. At least, not until you do the math. Stock prices and earnings don’t move concurrently. Stocks—the ultimate leading indicator—usually start falling before a recession. The numerator falls, so the P/E drops. The recession later wreaks havoc on earnings—the denominator plummets, and the P/E soars. That results in counterintuitive facts like stock prices bottoming in March 2009—when the trailing 12-month P/E was 110 (literally off this chart). Stocks then got more expensive the next three months before earnings began recovering. If you go by valuations alone, as stock prices rose, they got “cheaper.”

Exhibit 2: S&P 500 Trailing 12-Month P/E Ratios

Source: Multpl.com, monthly S&P 500 P/E Ratios. September 29, 1995 – May 19, 2014 (May 19 is estimated).

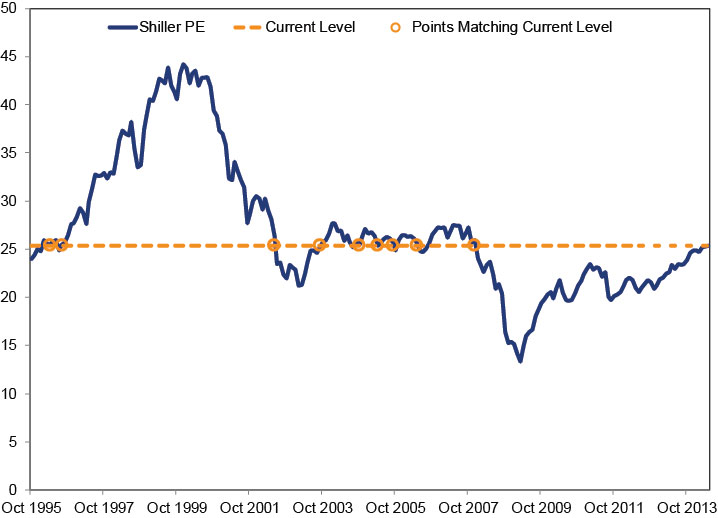

Still others suggest both the above are flawed, instead arguing earnings are just too darn volatile in the short run and must be smoothed out—blended over longer periods of time. Hence we get measures like the Cyclically Adjusted Price-to-Earnings Ratio (CAPE, or Shiller P/E after its founder, Yale Professor Robert Shiller). The CAPE smoothes those jagged earnings by averaging profits over the last decade and comparing the resulting figure to stock prices. This means forecasting partly based on earnings more relevant during the Bush/Kerry election year (the Swift Boat Race, if you will), the year Smarty Jones won the Preakness and Kentucky Derby (like California Chrome this year) and a year before Hurricane Katrina. It also means 2008-2009’s damage to earnings—which leads to the sharp upward spike in Exhibit 2—is inflating the CAPE. In our view, it is hard to argue this has much relevancy for the future.

Exhibit 3: S&P 500 CAPE Ratio

Source: Multpl.com, monthly S&P 500 CAPE ratio, September 29, 1995 – May 19, 2014 (May 19 is estimated).

Take note, too, that there isn’t anything lofty about current levels. S&P 500 CAPE hovered around 25 during much of 2003, 2004 and 2005.

Finally, consider: CAPE was not intended to forecast cyclical turning points in markets. As we’ve written, CAPE conceptually is a tool to forecast the next decade of returns (folly, but that’s a topic for another day)—hence the 10-year smoothing. But the punditry often suggests using it cyclically or strategically flipping among low CAPE areas. However, mixing the intended function and the cyclical predictiveness could imply the good times keep a’ rollin’ through 2019, with a possible downturn thereafter. We’d suggest that’s a might unforeseeable—and exuberant.

So the next time you hear or read media suggesting stocks are in a bubble or some big sector or country rotation is afoot, and it’s all based on valuations, consider: The only permanence in markets is their cyclicality. As bull markets mature, folks gain confidence and are willing to pay more for earnings. Valuations typically expand in maturing bull markets—a phenomenon that can last for quite a while—and there is no automatic ceiling. Fearing the bull must end soon, simply because valuations are creeping up, is premature.

[i] Source: FactSet, S&P 500 12-Month Forward Earnings Yield as of 04/30/2014.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Politics The Tenth Question Facing Alberta2026-08-06

-

Corporate Information How You Benefit from Fisher Investments' Transparent Fee Structure

2026-08-04

2026-08-04 -

Corporate Information How Fisher Investments' High-Touch Service Helps You2026-08-04

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets — July 27 - July 312026-08-03

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today