Personal Wealth Management / Economics

Pomp and Financial Circumstances

Rising student debt levels won't slow growth or shock markets.

Fall is officially here, folks! This means college-goers around the country are returning to school, and (right on schedule) pundits are worrying about student loan debt. US student loans exceed $1.3 trillion and have doubled since 2009, sparking concerns of a massive, unpayable burden that might shift to taxpayers or keep grads from becoming full-fledged economic contributors. This is a politically potent issue, to be sure. But the data don't suggest matters are anywhere near so dire overall: Few borrowers are troubled, and the majority will likely earn (and contribute) far more than they would absent an education. Investors needn't fear a coming wave of impoverished graduates dragging down the economy or pumping up federal debt.

Tuition costs have risen rapidly in recent years, and the federal government is under increasing pressure to step in and relieve indebted students-not just those who attended now-closed private universities like ITT Technical Institutes and Corinthian Colleges, but perhaps all borrowers. Many suggest student debt is just unaffordable and, with 92.5% of student loans ($1.26 trillion) federally issued, the government is already on the hook for most losses-losses the CBO projects will rise 30% over the next decade. The combination of rising defaults and demands for Congress to intervene has many worried that taxpayers could be on the hook for tens, maybe hundreds of billions of dollars.

Congress has reacted to recent cries for loan forgiveness in time-honored Congressional fashion: by drafting several student debtor-friendly bills that are now stalled in committee until next year at least. Said differently, after the election. Who's to say whether the 2017 Congress will resurrect the measures, or whether the new president will favor (or prioritize) them? Election-year promises and bill drafts frequently aren't worth the paper they're written on. In addition, the CBO's more pessimistic projection of $170 billion in losses over the next 10 years comes out to just over half of federal spending last month. Not to be dismissive, but student loan defaults are very unlikely to lift federal debt or deficits to dangerous levels, even if the CBO's projection proves true.

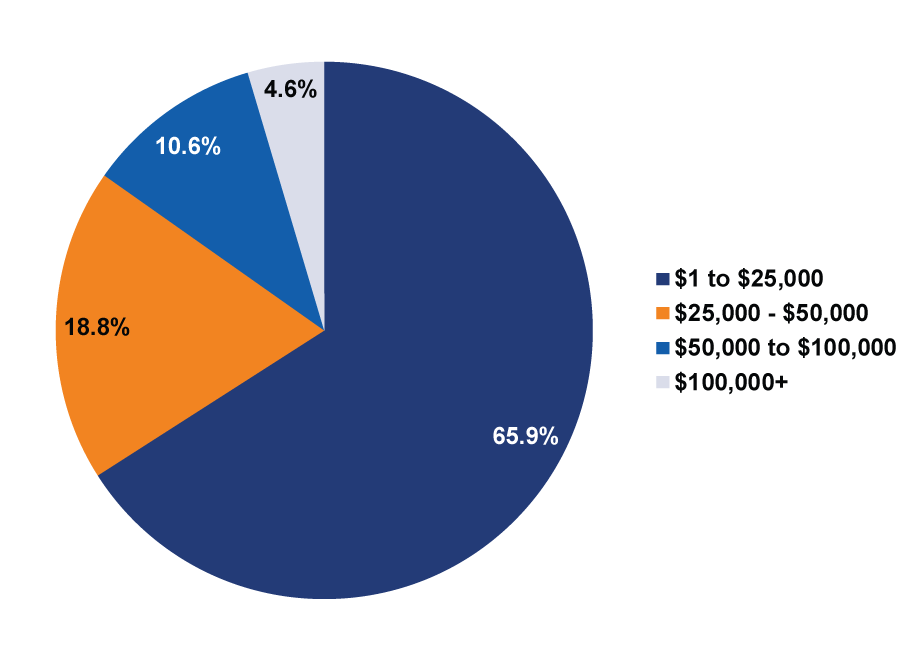

Student loan fears don't stop with federal debt and deficit worries, though. If consumer spending is over two-thirds of GDP and young people are too indebted to spend, many fear the economy will suffer. But let's weigh this theory. Although some graduates are suffering financially, student loans as a whole aren't imperiled-a fact fixation on total and average debt levels misses. First, the increase in total borrowing over the last dozen years was mainly due to higher enrollment, particularly during the recession.[i] That $1.3 trillion is spread over many, many borrowers. Median monthly payments are low, as are median debt balances: 38% of borrowers have less than $10,000 in outstanding loans. Sensationalist news stories tout rising average debt levels-but these are skewed higher by a small pool of major borrowers (more on this below).

Exhibit 1: Distribution of Student Borrowers by Current Debt Balance (in Percent)

Source: Federal Reserve Bank of New York, Student Loan Data Report, as of 9/16/2016. Distribution of Borrowers as of Q4 2015.

To be sure, delinquency rates are rising too-but this is often the result of choice, not hardship. Don't pay your mortgage, and the bank takes your house. Blow off your car payment, and it's suddenly impounded. No such consequences accompany lagging on student debt-heck, if you make consistent payments on a federal loan for 20 - 25 years,[ii] they can be canceled. If repayment depends on priorities rather than poverty, more late payments doesn't necessarily indicate grads are in dire financial shape.

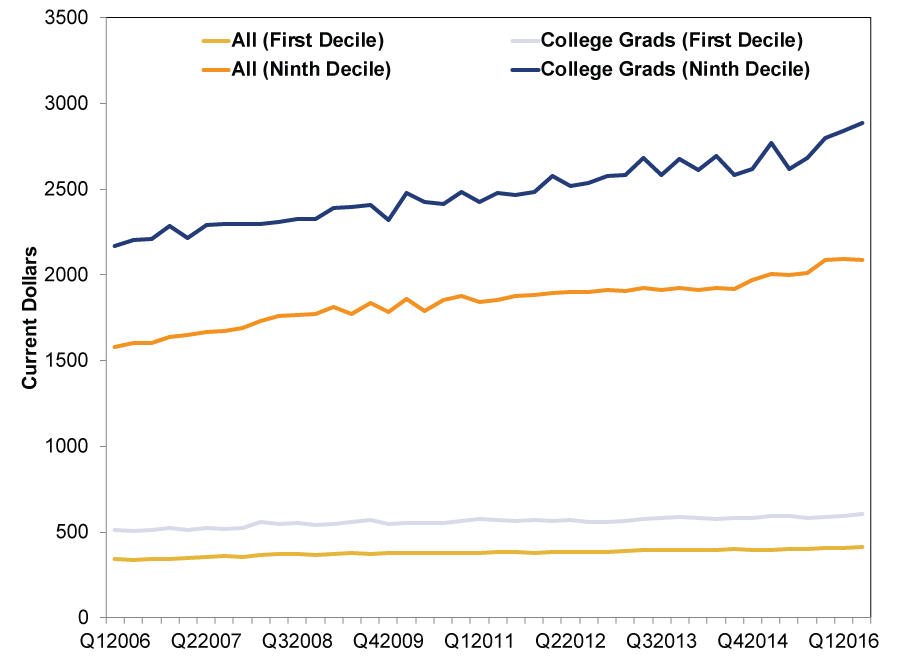

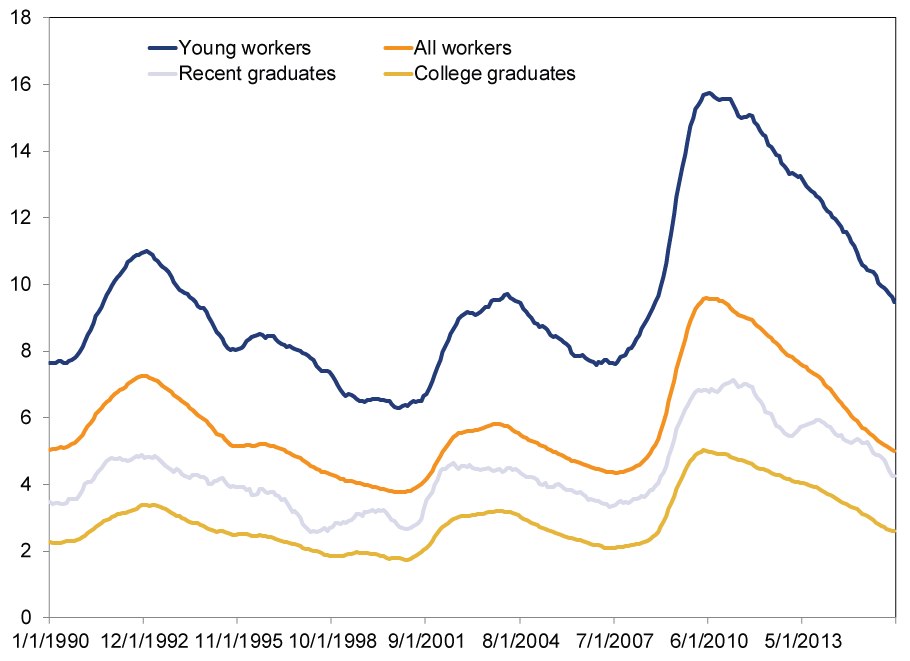

In general, they're actually more likely to be in pretty solid financial shape. The college-educated earn more on average (Exhibit 2) and are employed more often (Exhibit 3). A note on the former: the two top lines show the highest-earning ten percent (or decile, for the statistically inclined) of the college graduate population and the overall population, respectively. The lower two lines show the lowest-earning ten percent for each-in both cases, grads earn more.

Exhibit 2: Selected Median Weekly Earnings, January 2006 - June 2016

Source: Bureau of Labor Statistics, as of 9/15/2016.

Exhibit 3: Selected Unemployment Rates, January 1990 - March 2016

Source: Federal Reserve Bank of New York, as of 9/15/2016.

Defaults are concentrated among those who don't graduate, but they typically have much smaller loan balances and account for just 16% of borrowers. The lesson is clear: Don't confuse a few anecdotes about adjunct professors living in poverty after borrowing $200,000 to pursue artsy doctorates with an actual, widespread trend. The outliers get the headlines, but they aren't the norm. (Those with greater than $200,000 outstanding are 0.94% of the 44.2 million borrowers.) In reality, today's biggest debtors-who skew average debt statistics higher-are more likely tomorrow's highest earners. This helps explain why the typical borrower paid off their student loans in just 10 years in 2013, down from more than 20 in 1980.

One final set of concerns about student debt centers around borrowers' ability to buy a house, get married and have children. These are common (if far from universal) goals, and student loans may affect decisions about them-but these are personal decisions with little to no bearing on the overall economy. It's a fallacy to presume only married homeowners can earn and spend. A single renter's bills may be different from a married couple with a mortgage, but the former could easily be far better off financially.[iii] For broad equity markets, this doesn't register.

Let's take the worst case scenario-mass defaults on that $1.3 trillion pile of student debt. This is still pretty insignificant, even within the US, where total household assets stand at $103.8 trillion. If we're comparing various debt piles, US nonfinancial corporate debt (securities plus loans) exceeds $8.3 trillion. Mortgage debt is a shade under $14 trillion. Even auto loans total above $1 trillion.

Look, nothing here is to say college expenses aren't a concern, given quick-rising costs. But it takes a huge, ugly surprise to knock a global bull market off-track. Student debt in one country is negligible. It's also irrelevant for stocks today: Markets care about the next 3-30 months, while the consequences of a smaller-than-expected level of purchasing power among a limited cohort of young workers would play out over a generation. Lastly, as this New York Times article from nearly 30 years ago attests, concerns about overburdened students have been around for decades. Today's round of worrying is more of the same, not a bull-ending shock.

[i]Council of Economic Advisers, July 2016, pg 21

[ii] Depending on which income-based repayment plan you use.

[iii] Regardless, research by the Cleveland Fed shows that in many cases, student borrowers are more likely to hold a mortgage, get married and have children than non-borrowing graduates.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis The New Tariffs in Town Are Still Old News2026-07-24

-

Expert Commentary This Week in Review | Market Volatility, Tariffs, SpaceX

2026-07-24

2026-07-24 -

Economics A Summertime Check-in on US Consumers2026-07-23

-

Expert Commentary Why Ken Fisher Is Optimistic About European Stocks

2026-07-23

2026-07-23

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today