Personal Wealth Management /

Pros Falsely Fear an Optimistic Ma and Pa

Rising equity fund flows don't mean the bull's end is near.

Are mom and pop telling you to get out of stocks?

That's the question a few pundits tried to answer Monday, as data from the Investment Company Institute apparently showed retail investors "piling" into equity funds in June. And naturally, the answer was a resounding "yes!" Retail investors are notorious for piling into stocks at suboptimal times, so of course their buying should be a big fat sell signal for the rest of us. Problem is, there is no-zero-evidence mutual fund flows are a reliable indicator or even terribly high currently. They're a rough gauge of sentiment, but they aren't a timing tool.

It is true folks have a history of flocking to stocks near market peaks. But peaks aren't the only time retail investors buy. Not all new buying is evidence of heat chasing at the peak without any regard for the likelihood of a downturn. Some of it is a simple reversal of the deep pessimism of a bull's early stages, when folks who got battered during the bear swear they'll never own a stock again. As that wears off and folks realize they need at least some stock exposure to reach their long-term goals, they start wading back in. That's just normal investor behavior. Not euphoria, just a rationally optimistic move away from the bear's "it's going to zero!" hysteria.

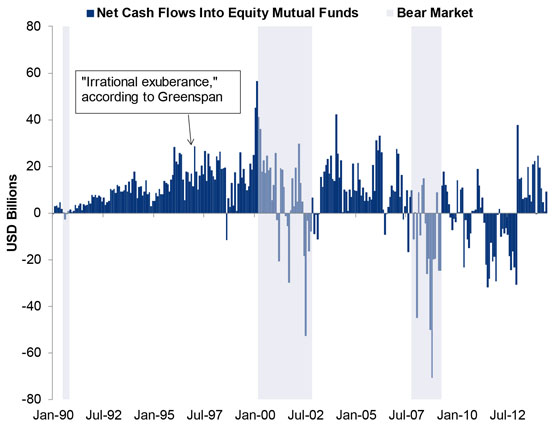

Now, as a bull wears on and approaches its peak, that optimism does morph to gung-ho-stocks-can't-lose euphoria, and that tepid wading turns to a margined-up, risk-shunning, stock-buying bonanza. Anecdotally and intuitively, the investment world accepts this as true. But it's extremely difficult to quantify, and mutual fund flows are decidedly not a good measure. Exhibit 1 shows monthly net inflows for managed equity mutual funds since January 1990. Yes, they spiked at the tech bubble's peak. But they also spiked in early 2004, 2006 and 2013. Incidentally, today's levels come nowhere close. What we've seen in recent months is about average for bull markets-just like fund flows were in late 1996, in the run-up to Alan Greenspan's infamous "irrational exuberance" speech. Rumors of a euphoric stampede into stocks, in our view, are as unfounded today as they were then.

Exhibit 1: Monthly Equity Mutual Fund Net Inflows

Source: FactSet and Investment Company Institute, as of 7/14/2014. June 2014 figure is an estimate based on ICI's weekly data.

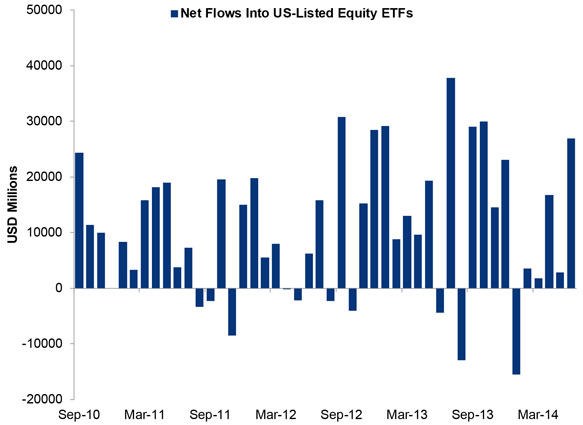

Plus, managed mutual funds represent only a slice of the retail investor universe-ETFs have stolen quite a bit of their thunder over the past several years. As Exhibit 2 shows, ETF flows are in line with recent history. Now, this is a very short window, but it's pretty much all we have to go on, since the longest available usable dataset starts in September 2010. And even this one we use with some trepidation, considering some gaps in the monthly reporting and the fact ETFs aren't as purely a ma-and-pa product as mutual funds. But it does suggest there isn't some massive spike in equity demand.[i]

Exhibit 2: Monthly Equity ETF Net Inflows

Source: ETF.com, as of 7/14/2014.

Even if the fund flow reporting were air-tight, it still wouldn't provide a full, accurate look at retail investors' behavior. Fund flows are simply too narrow-they completely ignore the counterfactual. They don't tell you where the cash for new purchases came from or what folks do with the proceeds of redemptions. If folks sold individual stocks to buy a managed fund and then ditched the fund for an ETF, that tells you about a change in product preferences-nothing else. A team at one big-name firm tried to quantify investor behavior by analyzing transactions within their firm's own accounts, but by their logic, everyone(!) sold in June and corporate stock buybacks were the only source of demand.[ii] Which seems just a wee bit suspect.

Simply, no one indicator can fully capture investor behavior. Not fund flows; not margin debt; not cash, equity and bond holdings on household balance sheets; not the savings rate; not investor sentiment surveys; not any of the others headlines hype at any given time. Try as the statheads might, there is no reliable means to turn fluffy feelings into hard numbers.

You can sense it qualitatively, though, and we see no signs of euphoria today. Restaurants didn't spend the last month airing CNBC instead of the World Cup. No one, as far as we can tell, is arguing stocks will rise forever and the business cycle is a relic. Our hairdressers, drycleaners and bartenders aren't giving us hot stock tips-they're still giving us piteous looks when we say we work in finance. Most of the punditry claims the best stocks can do over the rest of the year is a return in the low single digits. If you call for another 5% by year-end, you're a raging bull.

Some argue higher fund flows amid this rather blah sentiment is a sign investors' trading decisions are out of touch with reality, but this is backwards. Euphoria isn't mom and pop buying stocks when everyone is skeptical. Euphoria is when everyone is, you know, euphoric. Rising equity demand when sentiment is still very much in check-when few appreciate just how strong the backdrop for markets is right now-is just folks slowly realizing the world isn't as bad as they thought. It's the bull market climbing the proverbial wall of worry-and all evidence indicates that climb should last for the foreseeable future.

[i] Like, for example, they forgot to include category-specific flows data in their May 2013 report, so we had to manually calculate it based on the totals for 2013's first half. And we had to do something similar for December 2012 and December 2013, as they shunned the monthly report in favor of a full-year snapshot that didn't bother including separate December data. Now, we aren't trying to call them out-but these call the reporting into question and, in our view, suggest readers should take this with a big fat grain of salt.

[ii] Even if the methodology weren't beyond opaque and shady, we wouldn't buy the analysis. The firm in question has about $2 trillion in assets under management or custody. That's a tiny slice of investable assets in the US.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets — August 3 - August 72026-08-11

-

Market Analysis Rechewing Fed Independence Fears2026-08-10

-

Expert Commentary 3 Things You Need to Know This Week | US Inflation, UK GDP, RBA

2026-08-10

2026-08-10 -

Market Analysis Four Overlooked Costs With Dividends2026-08-10

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today