Personal Wealth Management / Economics

Putting Historic Jobless Claims Into Perspective

The bear market anticipated economic conditions’ rapid deterioration.

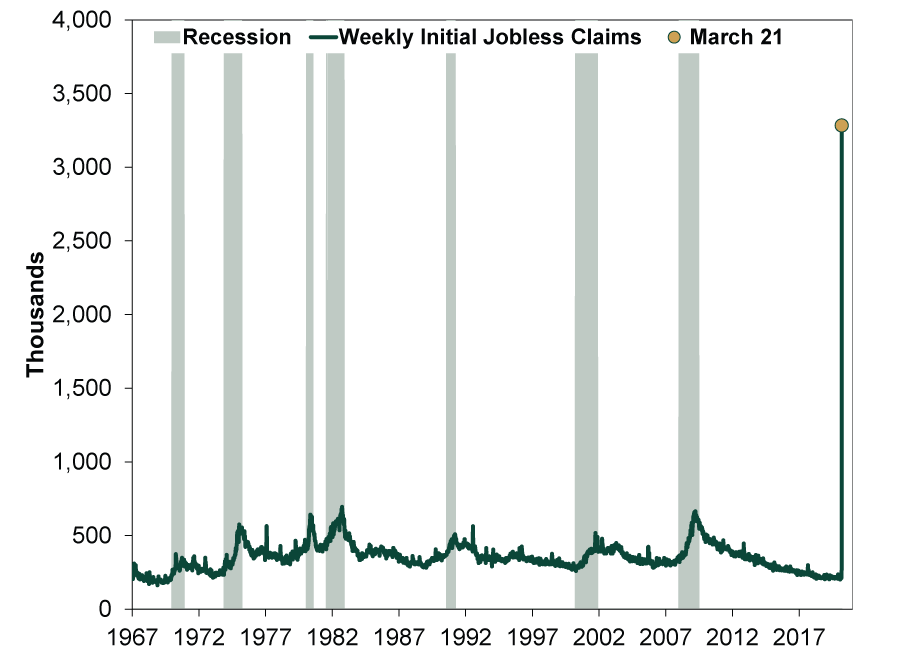

Thursday morning, the Labor Department’s widely anticipated initial jobless claims report confirmed what almost everyone expected: New claims for unemployment insurance skyrocketed in the week ending March 21—hitting 3.28 million. This far surpasses its previous 695,000 record high in October 1982 and the last recession’s late March 2009 high, 665,000. It also surged from a historically low level the prior week, illustrating the speed at which the business disruptions caused by the coronavirus response are hitting the economy. (Exhibit 1) From here, we expect most labor market metrics to deteriorate—especially if the business interruptions persist for long. For those affected, this is a personal tragedy. But for investors, it is worth remembering that employment data are late-lagging—unlikely to forestall any market or economic recovery.

Exhibit 1: Unprecedented Job Losses

Source: Federal Reserve Bank of St. Louis, as of 3/26/2020. Weekly initial jobless claims, 1/7/1967 – 3/21/2020.

Many believe this week’s record high is only the tip of the iceberg. Last week’s unemployment filing tsunami overwhelmed many states’ websites, preventing some individuals from claiming benefits. There were also more furloughs and layoffs this week, and the new coronavirus stimulus act will allow gig workers and other freelancers to file (if it passes the House in its current form). Others who are out of work may simply take a little time before filing. Hence, observers expect a high level of claims throughout April, driving the unemployment rate up massively. As such, many fear unemployed consumers can’t spend, and with US GDP roughly 70% consumption, they figure it will hamstring growth and create a downward economic spiral that saps stocks, too.

While that sounds stark, it is important to keep in mind that unemployment rises in every recession, often triggering similar fears. It has never forestalled a recovery, though. The reason is that consumption is remarkably stable historically. While consumption is a big slice of GDP, it hasn’t been very much of a swing factor. Since 1959, the only time consumer spending experienced quarter-over-quarter drops was two quarters in late 2008 and early 2009.[i] Trade and business investment typically swing much more than consumer spending—contributing hugely to cyclical shifts in the process. This is because the bulk of household spending isn’t discretionary, and savings and unemployment benefits usually help cushion any hit. Folks may forego non-essentials in a downturn, slowing consumption growth on the margin, but it rarely shrinks for long. Now, perhaps consumption will take a bigger hit this time tied to business interruptions and closures. But that highlights a key point: The economy’s issues ahead are much more about how long those interruptions last than the extent of unemployment. One can easily envision pent-up consumer demand driving a spike if those interruptions fade soon.

Stocks normally bottom ahead of improving jobless claims. In the last bear market, the S&P 500 hit its low on March 9, 2009. During the accompanying recession, jobless claims peaked shortly thereafter—on March 28, 2009. But they remained elevated for months afterwards, alongside a rising unemployment rate, falling labor-force participation rate and worries over rising joblessness driving down consumption and bringing more layoffs. Yet by the end of March, the S&P 500 had risen 18.1% from the low.[ii] By the end of the year, stocks were up 67.8%.[iii] It was only clear in hindsight, but by early 2010 most labor market metrics had begun an improvement that pushed unemployment down to near-record lows before the coronavirus hit. Because of this downturn’s unique circumstances—being driven by a pure, external, sudden stop for normal business—we think hiring could resume much faster if “social distancing” measures start to unwind soon. After all, many of today’s jobless claims not only include layoffs, but also furloughed workers just waiting to return when they are allowed to.

So, yes, these data don’t look great—and they may not for a while. But we don’t think there is much reason to believe they will prevent brighter economic days from eventually arriving.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary Why Ken Fisher Is Optimistic About European Stocks

2026-07-23

2026-07-23 -

Economics A Summertime Check-in on US Consumers2026-07-23

-

Market Analysis Why the SOX “Bear Market” Isn’t Foreboding2026-07-21

-

Politics Blunting Burnham?2026-07-21

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today