Personal Wealth Management /

QE Noise

Commentary on quantitative easing can be all over the place-we're here to help you make sense of it.

Quantitative easing (QE) is winding down, but QE chatter isn't. And there is no shortage of conflicting views, which is where we come in-to help investors see past the noise.

As a refresher: QE is the Fed buying long-term assets from banks, ostensibly trying to lower interest rates, thereby spurring demand for loans-in theory, stimulating the economy with added capital. When the Fed buys a bond, it credits the account of one of the 19 primary dealer banks with electronic credits-reserves-it hoped would underpin new lending. The first round of bond buying was announced in November 2008 and began in early 2009. A second round was announced in late 2010, after inflation trended lower. This was followed in 2012 by QE3 and what we affectionately call QE-infinity, which basically said the Fed would buy bonds at an $85 billion monthly pace until they sorta felt like not buying at that pace any longer, a point Ben Bernanke first alluded to in May 2013. The official "taper," or slowing of bond buying, was announced in December 2013, and there have been five rounds since. The bond buying is on course to cease in October, which the Fed acknowledged recently.[i]

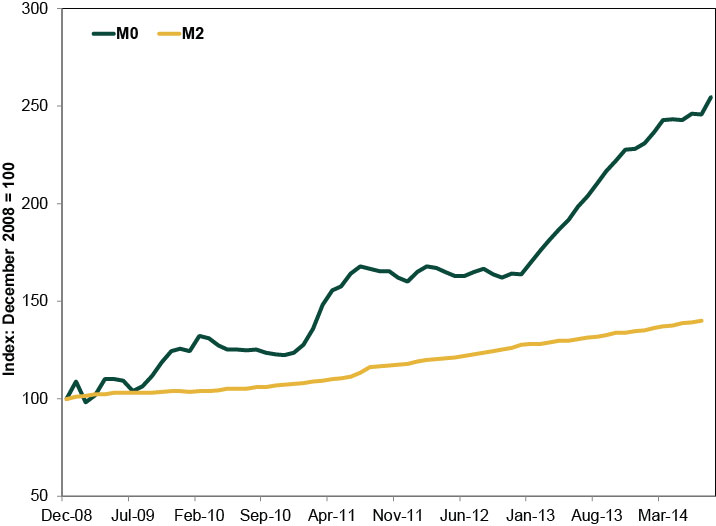

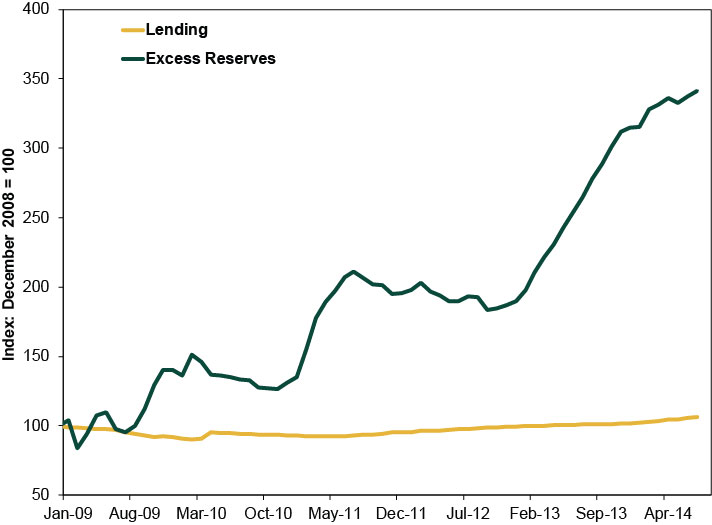

The effect of QE, in our view, has been less than favorable. As Exhibit 1 shows, while the monetary base (M0) went gangbusters, the amount of money in circulation (M2) was tepid-rising M0 alone doesn't boost economic activity if the money sits on the sidelines. As Exhibit 2 shows, while excess reserves have jumped, lending hasn't.

Exhibit 1: Cumulative Monetary Base Versus Money Supply Growth

Source: St. Louis Federal Reserve, as of 08/25/2014.

Exhibit 2: Excess Reserves Versus Lending

Source: St. Louis Federal Reserve, as of 08/25/2014. Excess Reserves of Depository Institutions. Loans and Leases in Bank Credit, All Commercial Banks.

Our views are pretty uncommon-it might be hard to square with what we say with the many competing voices. Particularly those that would seem to agree, on the surface, that QE didn't boost the real economy.

For example, one MarketWatch article argues QE didn't work because folks have hoarded $10.8 trillion in cash instead of "putting their money to work in the economy" by spending or investing, contrary to QE's aims. Now, we agree QE didn't flood markets, but that $10.8 trillion figure isn't evidence. The pace of cash accumulation didn't jump when QE began-it actually slowed down during this expansion. The article tries to scale it, comparing the $1.17 trillion rise in cash or cash-like holdings since September 2012 with the $1.24 trillion in QE over the same period-concluding "95% of QE ended up ... in a safe and boring bank account," but that doesn't hold. The money went to bank balance sheets, not consumers, and banks didn't use it to goose lending.

The above-mentioned piece attracted many eyeballs-and a direct rebuttal on Pragmatic Capitalism, which explains why QE didn't boost consumer savings. But it goes on to argue that by reducing the supply of Treasurys, the Fed forced investors into other interest-bearing investments-junk bonds on the high end, bank deposits on the low end-and that's why "consumers are spending too little to drive the recovery into a higher gear." But this, too, doesn't quite match reality-if folks have always saved and invested, why would the composition of those savings and investments impact consumer spending? The article points to lower interest on bank deposits as the culprit, but we struggle to think of a time when the deposit interest rate was ever much of a driver.

Overall, both articles suffer from two fallacies. One, they put too much weight on consumer spending. Yes, it's the biggest component of GDP, but it isn't the sole driver of growth. Heck, business investment took a good three years longer to recover from the last recession! We won't argue consumer spending has grown gangbusters this time around-spending growth during this expansion is the slowest on record-but it isn't the weakest link in GDP.

Two, both pieces flat ignore the reason why QE isn't working. The MarketWatch piece does acknowledge epically slow loan growth, but it misses the cause. QE depressed long-term rates, which flattened the yield curve-shrank the gap between short-term and long-term rates-and shrank banks' profit margins. Add in the higher regulatory capital requirements, and it's no wonder banks chose to sit tight-lending was a higher-risk, smaller-reward endeavor. This is changing now, with the yield curve having steepened since taper talk began in May 2013. Loan growth accelerated in January and is still strong-but it takes a while for this to flow through to the real economy.

In short: The US grew despite QE, not because of it. Now that QE is ending soon and lending is up, the backdrop seems ripe for the US to accelerate.

[i] Take this with a grain of salt, of course. They just said that if they keep tapering at the same pace they have been, they'll be out of things to taper by October. But that "if" depends on what the economy actually does between now and then. And how the Fed people interpret it. Maybe also what they ate for breakfast.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary 3 Things You Need to Know This Week | Q2 Earnings, ECB Meeting, Trump Accounts

2026-07-20

2026-07-20 -

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—July 13 - July 172026-07-20

-

Market Analysis Pumping Up the Yen?2026-07-17

-

Expert Commentary This Week in Review | US-Iran Conflict, US Inflation, New UK Prime Minister

2026-07-17

2026-07-17

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today