Personal Wealth Management / Market Analysis

Reflections on Corrections and China

Corrections are trying, but markets usually reward patience.

Global markets' selloff continued Monday, and by day's end, the MCSI World Index, S&P 500 and many other indexes were officially in correction territory, down -10% or more from their prior peak. The rout started in China, where local stocks fell -8.5% for the day, wiping out all year-to-date gains.[i] As fear grew, the selloff traversed the world, hitting the eurozone (-5.4%), UK (-2.7%) and finally the US (-3.9%).[ii] It is impossible for any human, technical indicator or algorithm to know where stocks will go immediately from here. They could rebound Tuesday, they could bounce around sideways, or they could tumble more-short-term moves are always impossible to predict (or time). But this volatility does look like a classic correction panic, with nothing new or surprising that markets haven't already fretted for a long time. In our view, this is not a time to sell. We believe this is a time to take a deep breath, stay cool and hang on tight so you don't miss the rebound, whenever it occurs.

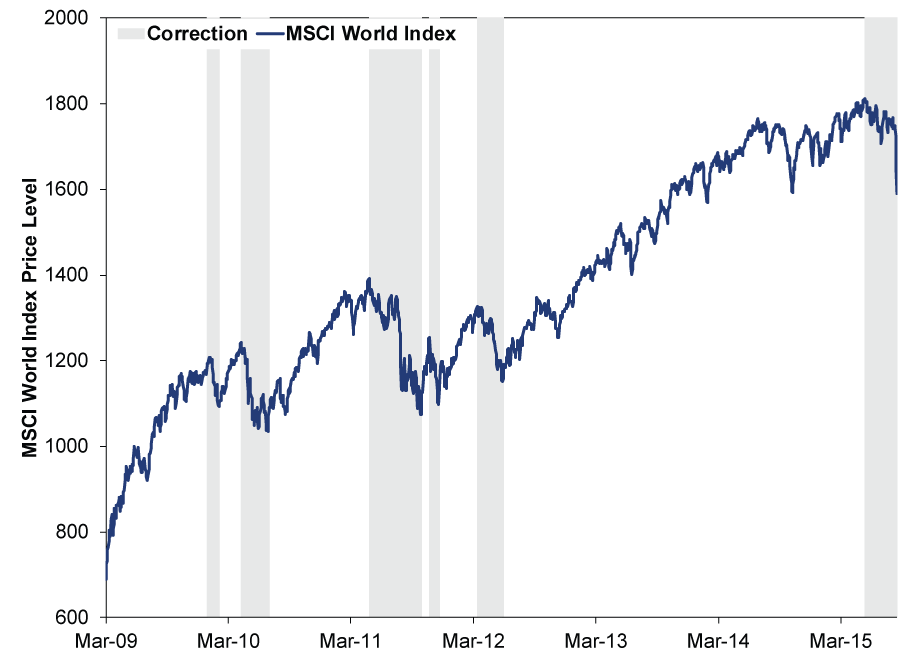

Corrections-short, sharp, sentiment-driven drops of -10% or worse-are uncomfortable and scary, but they are normal in bull markets. With the MSCI World Index down -12.2% since May 21 as of Monday's close, we now have the sixth correction of this bull market (Exhibit 1). Corrections are emotionally difficult to sit through, but they usually end as suddenly as they begin, and the recoveries are often swift and strong. Enduring these gyrations is the price we pay for bull markets' strong long-term returns. If you're investing for long-term growth, riding these ups and downs is likely necessary to reach your goals.

Exhibit 1: MSCI World Index Corrections During This Bull Market

Source: FactSet, as of 8/24/2015. MSCI World Index price level, 3/9/2009 - 8/24/2015.

World stocks' last correction ran from 4/2/2012 - 6/4/2012, when the MSCI World Index fell -13.1%.[iii] The S&P 500 came within a rounding error of a correction then, falling -9.9% from 4/2/2012 - 6/1/2012.[iv] For much of last year and this, headlines warned markets were "overdue" for another one. But now that it is here, pundits seem divided on whether it is a true correction or the start of a bear market, a deeper, longer, fundamentally driven decline of -20% or greater. We've seen plenty of sensible advice to keep calm and avoid panic-selling. But we've also seen alarmist warnings of much more trauma to come, with colorful language designed to whip up a frenzy. This is a big hallmark of a correction.

This pullback has another correction hallmark: a big scary story. Past correction stories during this bull market include the eurozone crisis and the US credit rating downgrade. This time, all eyes are on China. Many claim China's crashing local stock markets, slowing economy and recent currency devaluation are finally rippling globally, as the long-feared hard landing finally happens. After seeing a couple UK headlines reference The China Syndrome, we did a quick Google news search for "China Syndrome stocks" and got about 71,000 hits. But stocks didn't really have any new China-related information on Monday. Some stories fretted a lack of new Chinese stimulus, seemingly overlooking a couple small measures announced over the weekend and late last week. Others pointed to the Chinese government's decision not to intervene in markets Monday, instead accepting the decline (and having state-run media give it a Twitter hashtag), but in the grand scheme of things it's mostly positive if China avoids haphazard interventions and allows markets to run their course. Last month's interventions perplexed investors, and longer term, markets would welcome the sign of financial maturity.

As for China's economy, while it has slowed, this isn't new. China has slowed for years, in an orderly fashion, despite persistent hard-landing fears. We've looked hard for evidence the slowdown is materially worse now, and we see precious little. China's spate of official economic data for July slowed significantly from June, but it was in line with the longer-term trend (and numbers seen earlier this year). As for the slowdown's impact on China's trading partners, exports from many major countries to China are up year-to-date versus 2014. Some cite China's slowdown as a risk for oil and other commodity prices-implying these in turn are another risk for stocks-but this ignores the vast supply glut that has pressured oil and most metals since 2011. This is bad news for commodity-reliant economies, but these nations (among major countries, Russia and Brazil are the most troubled, with Canada and Australia feeling it to a lesser extent) are a minority of world GDP. For the vast majority of the oil-importing world, low prices are a modest tailwind. Fears otherwise seem mostly noise-searching for meaning in coincidentally falling prices.

If your long-term goals require equity-like returns over time, one of the biggest risks you can take is being out of stocks. In our view, the only time to do so is when you see a big fundamental reason not to-a reason few or no others see. Widely discussed issues like China and oil don't fit the bill. The more something gets talked about, the less power it has to sink stocks lower or for longer. Oil's rout started about 14 months ago-no surprises there today. Chinese stocks have tumbled for two and a half months, hogging the world's attention as they slid. These issues can roil sentiment, and they might keep doing so for a while longer. But as Ben Graham so famously said, in the longer run, markets weigh fundamentals, and on both of these fronts, there is more good than bad. Note, even if China slows sharply this year and grows just 5%, it would still add about $500 billion to world GDP. That is the opposite of a recession.

So stay cool, and if you're in this for the long haul, do whatever you must to avoid the temptation to make a hasty decision. Turn off CNBC, get some fresh air, call your adviser for some counsel and encouragement, spend quality time with family or friends, take the dog out for a romp-whatever suits you. And always remember, when corrections strike, markets usually reward patient investors.

[i] FactSet, as of 8/24/2015. Price return of Shanghai A-Share Composite Index on 8/24/2015.

[ii] FactSet, as of 8/24/2015. Price returns of the Euro Stoxx 50, FTSE All-Share and S&P 500 Indexes on 8/24/2015, all in local currencies.

[iii] FactSet, as of 8/24/2015. MSCI World Index price returns, 4/2/2012 - 6/4/2012.

[iv] FactSet, as of 8/24/2015. S&P 500 price returns, 4/2/2012 - 6/4/2012.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis The New Tariffs in Town Are Still Old News2026-07-24

-

Expert Commentary This Week in Review | Market Volatility, Tariffs, SpaceX

2026-07-24

2026-07-24 -

Economics A Summertime Check-in on US Consumers2026-07-23

-

Expert Commentary Why Ken Fisher Is Optimistic About European Stocks

2026-07-23

2026-07-23

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today