Personal Wealth Management / Market Analysis

Scaling a Wallop Potential: Chinese Shadow Banking

Do troubles in China’s shadow banking sector have the power to wallop the bull market?

Fears of a Chinese hard landing have morphed a lot over the last several years. Lately, they have re-focused on China’s shadow banking system, particularly now that the Chinese government is attempting to unwind large portions of that space. But do troubles there have the clout to “wallop” this bull market? Wallops are large, unforeseen events that can more or less wipe out expected global GDP growth, equivalent to about $5.1 trillion of economic activity in 2018, based on IMF estimates and forecasts. Based on the shadow banking system’s structure and an analysis of its most problematic portions, its wallop potential appears low.

Shadow banking gets its name because it encompasses the borrowing and lending that occur outside the traditional banking system—in its … shadow. Shadow banking systems exist all over the world and typically stem from inefficiencies or tight credit conditions in mainstream capital markets and banking systems. In China’s case, the traditional banking system is dominated by large state-owned banks that adhere to stringent government loan quotas and directives determining who receives credit. Furthermore, the government bars individual savers from purchasing debt instruments directly, so they need intermediaries in order to gain access to the market. In order to overcome those challenges, China’s estimated $10 trillion (~90% of Chinese GDP) shadow banking system emerged.

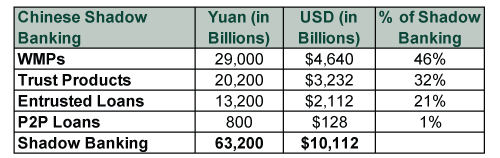

The shadow banking system primarily consists of wealth management products (WMPs), trust products, entrusted loans and peer-to-peer loans (P2P). (Exhibit 1)

- WMPs are financial instruments that typically use relatively short-term deposits (~12 months) to invest in bonds, money markets and bank deposits. However, some WMPs have invested in longer duration non-standardized debt instruments (e.g., bank loans) and other assets such as real estate.

- Trust Products are longer-term investment vehicles issued by trust companies (typically associated with a bank) that own loans, bonds, stocks and other financial assets. The key difference between trust products and WMPs is the duration of the investment period (long vs. short).

- Entrusted Loans are loans between two companies with a bank serving as middle-man (essentially connecting the two parties). While some entrusted loans have simple structures, others are more complex, allowing banks to move problematic or risky loans off their balance sheets.

- P2P loans are lending between an individual saver and borrower that is typically conducted through online platforms.

Exhibit 1: Shadow Banks Assets by Type

Source: Bank of International Settlements, as of 12/31/2016.

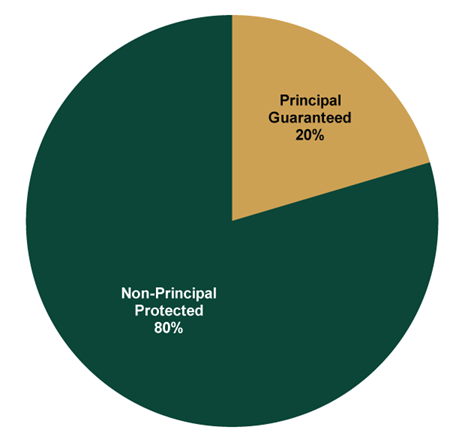

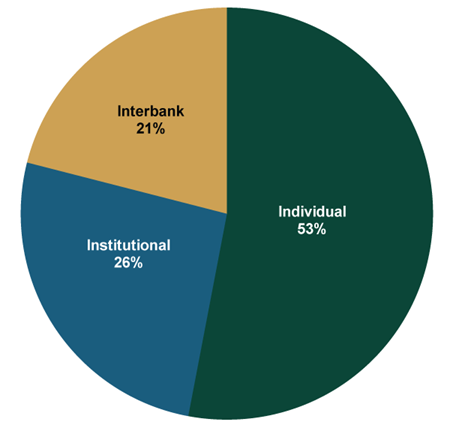

The Chinese government has two long-running goals: controlling economic activity and minimizing the risk of a financial crisis, which could disrupt social stability. Accordingly, officials have begun unwinding the shadow banking sector and moving this type of activity back into traditional financial markets. Though the aim is fostering stability, it could create some unintended consequences as the new regulations phase in ahead of the June 2019 deadline. Trust products, P2P loans and the majority of WMPs pose little risk to the Chinese financial system, as these are mostly transparent and successfully match duration—they aren’t complex long-term investments funded with short-term money. However, about 25% of WMPs, or $1.3 trillion, are invested in non-standardized debt assets or other assets, like real estate (Exhibit 2). These types of WMPs are equivalent to the commercial paper market (banks using short-term funds to meet ongoing financing needs), so the unwinding of these WMPs (which current regulations require) is like a $1.3 trillion commercial paper market disappearing in the next 12 – 18 months—all else equal, a sharp bank funding squeeze. Additionally, about 20% of WMPs come with explicit principal guarantees (Exhibit 3), while the vast majority of the rest have implicit guarantees (recently banned by the government). Major issues within this space could shake individual investor confidence, which represent about half of the investor base in WMPs (Exhibit 4), potentially resulting in bank runs.

Exhibit 2: WMPs by Investment

Source: Bank of International Settlements, as of 12/31/2016.

Exhibit 3: WMPs with Principal Guarantees

Source: Bank of International Settlements, as of 12/31/2016.

Exhibit 4: WMPs by Investor Type

Source: Bank of International Settlements, as of 12/31/2016.

Wallops don’t just have to be relatively large in size. They must also be widely unseen. Many believe the general opaque nature of the $2.1 trillion Chinese entrusted loan market (mostly kept off bank balance sheets) provides that unseen element. Considering these loans were kept off the balance sheet for a reason, they likely are of a lower quality in nature and probably mask the true amount of non-performing loans (NPLs) banks own. Chinese banks are already believed to understate their NPLs, raising the risk banks could need to raise capital, particularly if China experiences some sort of economic shock. However, investors have long been aware of—and feared—the potential for hidden problems in China’s banking system. Many take it as given that trouble lies beneath the surface. So while these products’ structures are opaque, it seems hard to argue this scenario is sneaking up on anyone.

While China’s shadow banking system is large and has some opaque elements, there appears to be a low probability of it spiraling through the global financial system to the tune of trillions of dollars. In order for it to wipe out $5 trillion of global GDP growth, practically all of the non-standard duration mismatched WMPs and entrusted loans would need to become toxic in a relatively short period of time. Then it would likely also require an additional catalyst to further magnify the impact. While this is possible, it is rather unlikely. The Chinese government has several tools at their disposal, including their $814 billion sovereign wealth fund and $3 trillion in foreign currency reserves (which are becoming less necessary as they liberalize their capital markets) they could use to address any issues that might arise. So while Chinese shadow banking merits close attention and could cause some short-term volatility, it likely doesn’t pack enough punch to derail the global expansion and end the current bull market’s run.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Politics The Tenth Question Facing Alberta2026-08-06

-

Market Analysis Western Oil and Gas Producers Are Ramping Up2026-08-06

-

Corporate Information How You Benefit from Fisher Investments' Transparent Fee Structure

2026-08-04

2026-08-04 -

Corporate Information How Fisher Investments' High-Touch Service Helps You2026-08-04

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today