Personal Wealth Management / Market Analysis

September Is Just a Month

September gets a bad rap, but history shows it isn’t inherently bad for stocks.

History shows September doesn't automatically mean trouble for stocks. Photo by Dan Istitene/Getty Images

September is upon us, and with the new calendar page comes the annual blitz of headlines proclaiming September the worst month for stocks and warning investors to sell, sell, sell. Like all seasonal saws, however, it’s rather perilous investing advice—no month, season or any set period is inherently bad or good for stocks. As ever, long-term investors should steer clear of the hype and focus on forward-looking fundamentals.

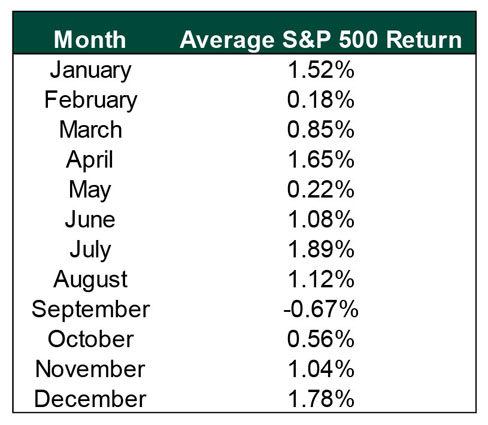

September’s reputation stems from a simple fact: September has the worst historical monthly average return in the S&P 500. Even though it has been positive 51.7% of the time since 1926, it’s the only month with an average negative return (Exhibit 1).

Exhibit 1: Average Stock Returns by Month

Source: Global Financial Data, Inc., S&P 500 total return from 12/31/1925 to 8/31/2013.

Observers have divined many creative reasons to explain why. Some say summer months are light on trading as investors take vacations. Once investors return to work in September, they dump the securities on the “to sell” list they wrote over the summer. Others say September’s bad reputation is a self-fulfilling prophesy—investors think the month will always be bad, so they always sell, and stocks always fall (even though they don’t!).

However, reality is far less colorful. The simple reason for September’s sad-looking average returns is since 1926, we’ve seen a handful of really awful Septembers. Two were during the Great Depression—1930 (-12.72%) and 1931 (-29.72%). Another followed in 1937 (-13.81%), and September 1974 dropped -11.52%. The Tech-led bear market had two bad Septembers—2001 (-8.08%) and 2002 (-10.87%), and September 2008 (-8.91%) is likely still fresh in most investors’ minds. All of these have something major in common: They were during big bear markets. None were isolated incidents—stocks didn’t magically tank because the calendar turned. Much deeper fundamental negatives were at work. That they happened to yield especially awful returns in September is mere coincidence, and this coincidence is what skews the average. Without these data points, historical September returns would look different. Or, if you prefer, keep them and simply calculate the median monthly market return for the month of September. Since 1926, it’s 0.10%. That means since then, we’ve seen an equal number of returns above and below.

So why do folks continually fall for this and other seasonal myths? Blame your brain: It’s programmed to. Looking for patterns is part of our evolution—it’s how our stone-age ancestors survived. We look for patterns to explain the unknown, and if we find even a hint of correlation, we decide it’s a rule. So September becomes the worst month, May is time to sell and go away, January predicts the year and Santa Claus brings December rallies.

But correlation is nothing without causation! If there is no repeatable fundamental cause for the apparent relationship, then it isn’t an actionable relationship. It’s mere coincidence—an interesting observation. Not what long-term investors want guiding their portfolio decisions.

Even if September’s historical returns were convincingly, repeatedly poor, “Sell in September” wouldn’t be actionable. To assume it works is to assume past performance dictates stocks’ future returns. It doesn’t! Stocks move on forward-looking fundamentals—investors’ expectations of future corporate profitability. And currently, fundamentals are better than most appreciate.

This doesn’t mean September 2013 is surefire positive. Volatility could very well continue. But short-term wobbles are impossible to predict and time with any certainty. For long-term growth investors, the opportunity cost of sitting out September is too big to ignore, in our view. Volatility is ever-present, September or not—but as long as fundamentals exceed expectations, staying disciplined and keeping a longer perspective is the right move.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Corporate Information How You Benefit from Fisher Investments' Transparent Fee Structure

2026-08-04

2026-08-04 -

Corporate Information How Fisher Investments' High-Touch Service Helps You2026-08-04

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets — July 27 - July 312026-08-03

-

Expert Commentary 3 Things You Need to Know This Week | US Jobs, Trade Balance, Earnings Reports

2026-08-03

2026-08-03

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today