Personal Wealth Management / Market Analysis

Social Security Shortfall

Americans fear Social Security is insolvent and have since just about always.

In an election season, one topic sure to be used as a political bludgeon is the solvency (or lack thereof) of Social Security. Each party will attempt to frame the other as sure to torpedo the survivability of this long-standing entitlement. And they'll both claim something needs to be done, NOW, to save the program.

After all, in the Social Security Board of Trustees' Annual Report to Congress, they conclude the combined assets of the Old-Age and Survivors Insurance and Disability Insurance (OASI and DI) will be depleted in 2033, three years sooner than projected in 2011. The report suggests that without any changes to Social Security-and presuming the underlying economic forecasts underpinning tax revenue estimates are right-the system will only be able to pay approximately 75% of scheduled benefit payments after 2033.

But before panic sets in, let's consider how dubious these assumptions are-and that both the economic assumptions and program structure are changeable.

Accurate forecasting on any topic is clearly difficult-particularly when looking out two decades. You can see this in past long-term governmentally produced forecasts, which are frequently wide of the mark-like federal government surplus projections for the next decade minted in 2000. (Juuuuuuuust a bit outside.) What's more, when was the last time the government ever successfully forecasted a looming recession? Baked into any forecast produced by any government body are a lot of assumptions-typically assumptions handed to them by politicians. What isn't included in these forecasts is any analysis of whether the assumptions are at all reasonable. Often, they're not.

Just because the government's long-range forecasts are often (or always) faulty doesn't guarantee Social Security's solvency. Legislative changes will undoubtedly be needed at some point. So let's explore a bit of the history and structure of the program to identify details often unexplained to taxpayers-details providing windows of opportunity for change.

Social Security's trust funds are funded by tax dollars-specifically, Federal Insurance Contributions Act taxes, or FICA, for short. Social Security collects these taxes from 158 million workers yearly and distributes benefits to about 55 million individuals. 85 cents from each tax dollar paid fund current benefits. The other 15 cents go into a "trust fund" used to pay people with disabilities and their eligible family members.

Now, contrary to some beliefs, these trust funds are by no means a "lockbox." They're not even a passbook savings account. By law, surplus funds are lent to the federal government through purchases of special-issue Treasury bonds for its general use. That means the money is spent. Which means the current workers' payroll taxes fund the benefits of today's retirees through a pay-as-you-go system (the aforementioned 85 cents noted), not liabilities-we're not borrowing to fund these payments. So, when today's young workers reach retirement age and are ready to collect benefits, their kids and grandkids-the workers of tomorrow-will fund their Social Security benefits. (One reason why future Social Security "liabilities"-payments due under the present program-are not, by any workable definition, debt.)

But this pay-as-you-go system also raises fears tied to demographics-that beneficiaries will become too numerous for workers to support. Particularly as the broad generation known as the "Baby Boomers" move further into retirement. But what's rarely discussed is that the Boomers aren't the largest generation in the US-the Millennial Generation (Gen Y) is more populous by almost 15 million. So combining Generations X and Y, millions and millions of working-age people will contribute payroll taxes to support the Baby Boomers' benefits. Moreover, discussions of the long-term demographic impacts of this often leave out immigration and naturalization.

But if that isn't sufficient to maintain the program, Congress isn't powerless to change aspects of Social Security. While some posit politicians don't have the political gumption to do it, Congress has previously made alterations on more than one occasion-so the "third rail" of American politics doesn't seem totally untouchable. Amendments made in 1956, 1961, 1962, 1965, 1972, 1977 and 1983 all were aimed at retaining Social Security solvency. Many times, these changes seemed ultra-minor. But small changes can have a bigger effect than anticipated.

For example, prior to 1972, benefits weren't automatically indexed for inflation. That year, amid a debt ceiling debate, Congress passed legislation providing for a one-time 20% boost to Social Security benefit levels and enacted an inflation index based on CPI.

The 1972 Cost of Living Adjustment not only indexed for prices, but also wages. Congress felt this maintained the purchasing power of benefits already awarded (price-indexing) and accounted for future entrants' higher wages. But this also gave new entrants double credit-resulting in skyrocketing benefit costs. At the time, the Trustees estimated Social Security would be unable to fully cover benefits by 1979.

To combat the declining Social Security trust fund, in 1977, Congress passed and President Carter signed legislation fixing the "double-indexing" error (among other small changes). No doubt, folks were upset about what they perceived as lost benefits. But ultimately, the changes went through, and (obviously) Social Security did not run insolvent in 1979.

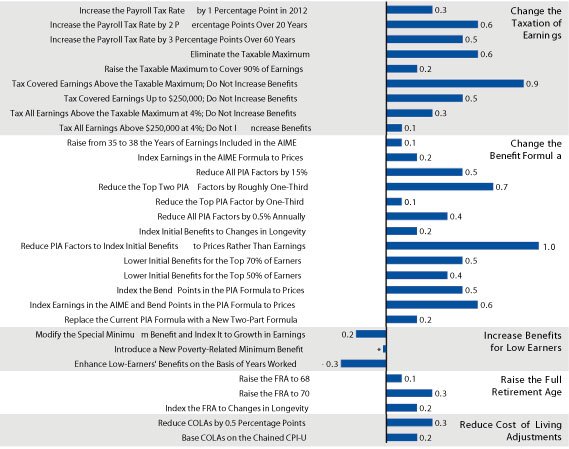

Looking forward, similar solutions (widely known on Capitol Hill) could be enacted. In fact, as the Congressional Budget Office indicated in its 2010 report, small benefits reductions or revenue increases (through quicker payroll growth, wage growth or tax rates) could dramatically prolong the program's full funding. The report outlined several theoretical adjustments and dozens of combinations as possible ways to keep Social Security strong, as detailed in Exhibit 1.

Exhibit 1: Policy Options And Estimated Impact

* = Between -0.05 percentage points and zero.

Source: Congressional Budget Office, Social Security Policy Options, July 2010. Figures in the bar chart represent the estimated percentage change in Social Security's actuarial balance associated with various policy options.

In the Social Security Board of Trustees' 2012 annual report, they once again recommended Congress work on legislation to fix the funding issue. So, until Social Security's issues are perceived to be more pressing, I wouldn't expect Congress to vote on any fixes. Ultimately, however, these government programs aren't some social contract-they're legislated entitlements. They've been amended and likely will be again-all through a simple vote.

In my view, the reality is fretting over the funding status of Social Security now is an exercise in futility. It's too long range, hinges on too many changeable and shifting inputs and is unlikely to materially impact the economy or stocks at any point in the foreseeable future.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis Why the SOX “Bear Market” Isn’t Foreboding2026-07-21

-

Politics Blunting Burnham?2026-07-21

-

Expert Commentary 3 Things You Need to Know This Week | Q2 Earnings, ECB Meeting, Trump Accounts

2026-07-20

2026-07-20 -

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—July 13 - July 172026-07-20

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today