Personal Wealth Management /

Switzerland Declares Currency Neutrality

The Swiss National Bank ceased artificially depressing the franc's value Thursday, sending currency markets on a wild ride. But the long-term impact of this is basically nil.

Fancy metalwork adorns the edifice of the Swiss Central Bank. Photo by Bloomberg/Getty Images.

The Swiss National Bank (SNB) is discontinuing the minimum exchange rate of CHF 1.20 per euro. At the same time, it is lowering the interest rate on sight deposit account balances that exceed a given exemption threshold by 0.5 percentage points, to −0.75%. It is moving the target range for the three-month Libor further into negative territory, to between -1.25% and −0.25%, from the current range of between −0.75% and 0.25%.

So began SNB President Thomas Jordan's statement published Thursday, which surprised currency traders and some supranational monetary "referees" by ending the bank's three-year old exchange-rate floor against the euro. The newly unleashed franc surged by 13% against the euro and 9% against the dollar-and left many observers scratching their heads and pondering Jordan's motivation. But while short-term gyrations could continue (literally always true, for any or no reason) we'd suggest the longer-term impact here is teensy.

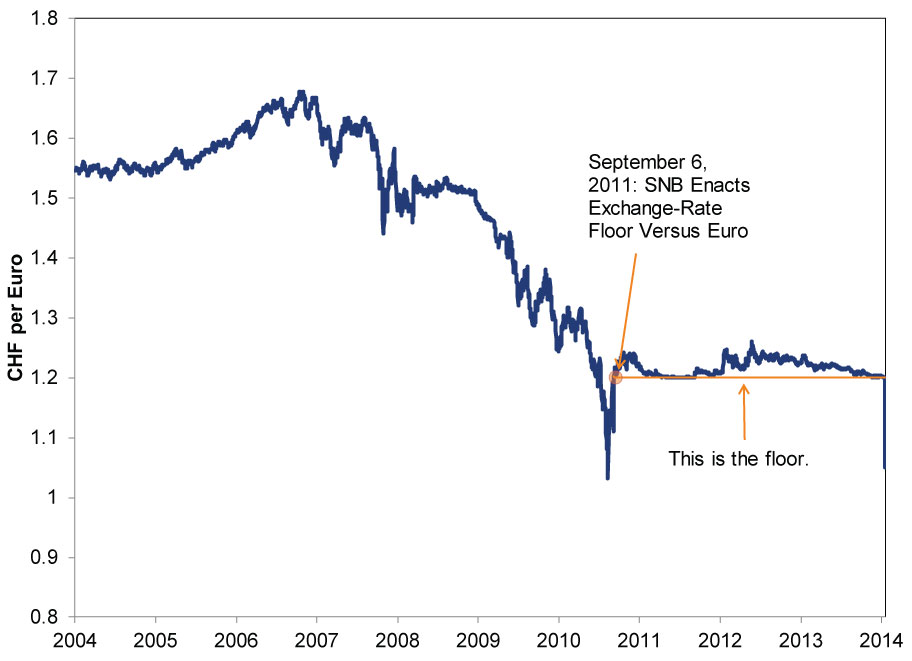

In September 2011, near eurozone fears' peak, the SNB feared a flood of capital would flee the euro and buy the franc, driving its value up-and hampering Swiss exporters' competitiveness. Hence, it enacted a minimum exchange rate-a floor-of 1.20 CHF per euro to stem a fast rise as traders sought refuge. The SNB would sell francs and franc-denominated assets and buy foreign currency (read: euro) denominated assets if the euro fell toward parity with the franc. The maneuver basically worked-since its September 6, 2011 unveiling, the franc has traded between a low of 1.200683 and high of 1.261382 per euro, a narrow bandwidth shown in Exhibit 1.

Exhibit 1: Swiss Francs Per Euro, 12/31/2004 - 01/15/2015

Source: FactSet.

So success! Or not. Currency floors (and pegs) are typically unstable, difficult for central banks to maintain. When a nation allows free capital flows, it cannot defend fixed exchange rates indefinitely. In Switzerland's case, the euro's steady decline versus most major currencies required the SNB to massively increase its balance sheet, affecting its independence to conduct monetary policy. Many observers thus expected the SNB to eventually dial back the program, although most expected a gradual move much later on, considering the SNB lauded the floor as a key part of policy about 30 days ago.

Hence the shocked responses. In the most widely circulated quotation we found on the subject, Swiss watchmaker[i] Swatch's CEO Nick Hayek emailed, "Words fail me," continuing, poetically, "Jordan is not only the name of the SNB president, but also of a river... and today's SNB action is a tsunami; for the export industry and for tourism, and finally for the entire country." And it may cause dislocations for Switzerland to be sure, but this is roughly 1% of global GDP we are talking about-not major. The impact here isn't large enough to affect the bull market materially.

Now, the story doesn't exactly end there, because some eastern European borrowers (home buyers, banks, businesses) have borrowed in francs due to lower interest rates. Those loan repayments became sharply more expensive Wednesday for a borrower who hasn't hedged, which includes basically all mortgages. But even this isn't large enough to cause major issues. The two nations with the most exposure-Hungary and Poland-have about €50 billion of exposure to franc-denominated loans. Hungary also implemented a nationwide fixed exchange rate for franc-denominated mortgage payments in 2011, nullifying the immediate effect of Wednesday's move. But also, there is a vastly larger pool of foreign currency-denominated loans in Eastern Europe that are euro-denominated. These borrowers? Unaffected.

Another meme holds this is a shot in a currency war, an utterly backwards thesis. A currency war is a competitive devaluation, a race to have the weakest currency. Switzerland intentionally strengthened the franc, which is the opposite. Did they surrender? Declare neutrality? Or is there just no currency war underway? We have long argued central bank policy is principally and rightly governed by domestic considerations. It seems the SNB is giving up on being an exception to that general rule.

We are guessing this is one of those mega-headline grabbing, but ultimately fleeting fears, like 2009's Dubai World default fears; 2010's muni default fears; 2011's nuclear fallout fears; 2012's Iran/Israel tensions; 2013's Syria fears; and 2014's false Fragile Five fears.

Stock Market Outlook

Like what you read? Interested in market analysis for your portfolio? Why not download our in-depth analysis of current investing conditions and our forecast for the period ahead. Our latest report looks at key stock market drivers including market, political, and economic factors.

[i] Hence the name, we think.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary Why Ken Fisher Is Optimistic About European Stocks

2026-07-23

2026-07-23 -

Economics A Summertime Check-in on US Consumers2026-07-23

-

Market Analysis Why the SOX “Bear Market” Isn’t Foreboding2026-07-21

-

Politics Blunting Burnham?2026-07-21

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today