Personal Wealth Management / Economics

The Fed Passes. Again.

Six years and six months since the bull market began, the Fed still hasn't hiked rates.

"To support continued progress toward maximum employment and price stability, the Committee today reaffirmed its view that the current 0 to 1/4 percent target range for the federal funds rate remains appropriate."

And there it wasn't, folks. The fancy verbiage above is how the Fed communicated Thursday it would again pass on hiking the fed-funds target rate for the first time since 2006. Most media types seized on two new sentences in the statement: "Recent global economic and financial developments may restrain economic activity somewhat and are likely to put further downward pressure on inflation in the near term" and "The Committee ... is monitoring developments abroad"-claiming this meant China and possibly the recent volatility forestalled rate "liftoff." Others, however, noted that the dot plot of Fed policymakers' rate forecasts showed 13 of 17 still thought rates would rise by year end. So whatever the reason this time, we guess it will be, lather, rinse, repeat come October and possibly December. That means we get at least another month of unnecessary media handwringing over a potential rate hike. Not hiking interest rates is frustrating-we would vastly prefer they just get on with it already. In our view, a rate hike now wouldn't wreak havoc-it would help sentiment climb the wall of worry by proving widely held fears of an initial hike wrong.

An initial rate hike just doesn't matter as much as the vast ocean of pixels the media has spilled over it claims. It doesn't ensure equity markets will be volatile. It is unlikely to present a risk to the bull. Whether rates are in a 0% - 0.25% bandwidth or slightly higher likely has no material economic impact, on banks or otherwise. It does not ensure the dollar strengthens more (itself a misperceived fear to begin with), as markets typically price in widely held fears like this. It doesn't necessarily drive up long-term rates on government or corporate debt, and it likely won't cause a panic across the Emerging Markets (EMs), as the EM central bankers quoted here rightly note.

In our view, the US economy can take a hike: It grew at a 3.7% seasonally adjusted annual rate in the most recent quarter; forward economic indicators are in lengthy uptrends; loan growth is rising; the yield curve (which shows the difference between short-term and long-term interest rates and is a proxy for bank lending's profitability) is steep; and loan officer surveys show loan demand is rising. These metrics are those most directly targeted by monetary policy. Many measures-like the strengthening dollar and recently rising short-term Treasury yields-allude to markets expecting a hike.

Now, the fed-funds futures market disagreed in the days before Thursday, highlighting a simple point: In its much-ballyhooed zeal to bring "transparency" to Fed decision making with dot plots, frequent speeches and verbose policy statements, the Fed has delivered the opposite. That amounts to a whole lot more communication. But more doesn't mean clearer, and that is the definition of transparency, last we checked.

The result of more communication is actually more confused Fed obsessing by the media. In recent weeks, pundits analyzed virtually every topic through the lens of what it all meant for the Fed. For weeks, our regular coverage of more than 100 global financial news websites and blogs has been choked by the Fed and articles proclaiming THIS is what the Fed should, could, or will do, and here are umpteen reasons why. It reached a crescendo this week. About half the coverage seemed to want a hike, half didn't. But the added coverage, words, plots and charts didn't reveal any real insight into what the Fed might do. It's all a distraction from what actually matters: the overall healthy and growing US economy.

The presumption the Fed must be transparent operates on the notion its decisions are vital to the economy's health. And, to an extent, that's true. But that extent is much more limited than many seem to presume. Yes, the Fed has a history of overshooting or acting too drastically and overconfidently, thereby quashing economic growth. But the notion an initial rate hike from around zero to something just higher than around zero amounts to a drastic error is overdone. Overshooting typically happens well into a tightening cycle. There is no history of an initial hike quashing growth or a bull market, and here is a collection of data and charts to prove it.

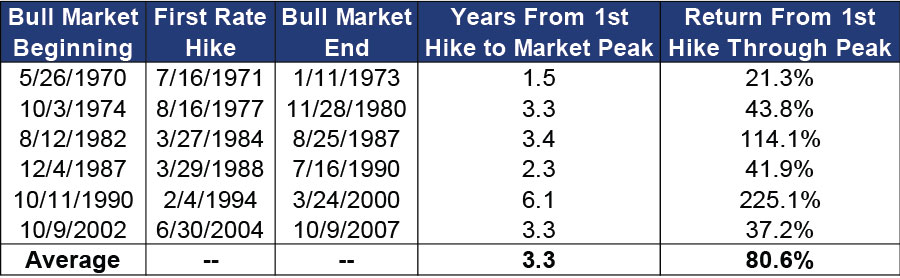

In Exhibit 1, we show the date of the first rate hike in bull markets since 1970 and the time and S&P 500 Index return to the bull market's eventual peak. As shown, the first rate hike has never ended a bull market.

Exhibit 1: Bull Markets Continue Past the First Rate Hike

Source: FactSet, as of 7/24/2015. S&P 500 Price Index returns.

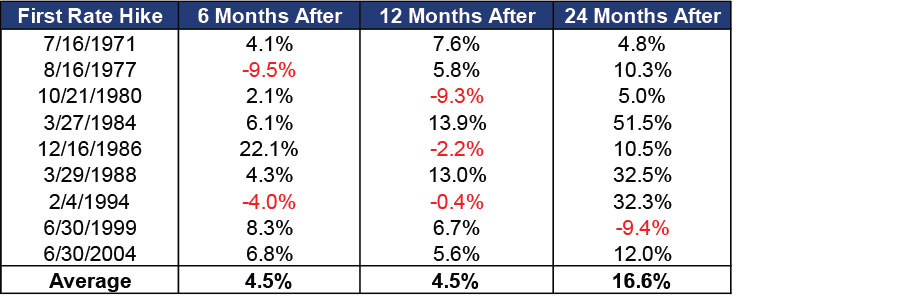

Now then, some bull markets like the 2000s had multiple tightening cycles. Exhibit 2 displays initial rate hikes in a tightening cycle and the subsequent 6, 12 and 24 months following the initial hike. As shown, results are usually positive. And, as the messy chart in this article shows, there isn't even a historical trend of heightened volatility after an initial hike. Only 1980's hike occurred right before a bear market began, and it is something of an outlier because the Fed wasn't targeting the fed-funds rate then. They began tightening a year earlier, inverting the yield curve before they even hiked.

Exhibit 2: Returns 6, 12 and 24 Months After Initial Rate Hike In Tightening Cycle

Source: FactSet, as of 7/24/2015. S&P 500 Price Index returns.

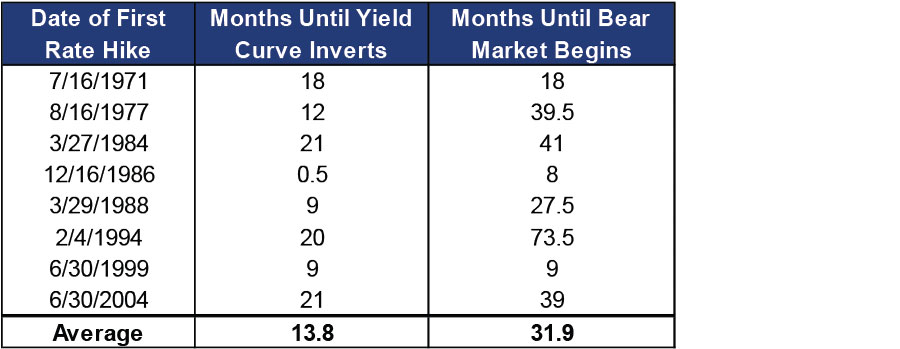

Which brings us to why initial hikes rarely materially affect stocks and the economy. For one, the Fed normally hikes when they have confidence the economy is growing, not when it is teetering on the brink of recession. No, they aren't perfect by any stretch. But, more fundamentally, short-term interest rates alone don't have much fundamental impact on the economy or credit availability. This is tied more to the yield curve. Banks borrow short term (think: deposit accounts and overnight funding markets) to fund longer-term loans. The rate they charge is their revenue. So when long-term rates exceed short rates, bank lending is quite profitable-incentivizing banks to make loans. Lending is key to businesses accessing capital, so the yield curve is an excellent forward indicator of economic activity. For decades, economists have generally agreed the opposite condition-an inverted yield curve, when long rates are below short-term rates-is a reliable indicator weak economic conditions (including recessions) are approaching. It doesn't tell you exactly when, but it gives you some indication fundamentals in credit markets are far from ideal.

When the Fed first hikes interest rates, the yield spread is usually quite wide, so one rate hike doesn't materially choke off lending. Exhibit 3 shows the length of time between the initial rate hike and the yield spread turning negative.

Exhibit 3: Time Between First Rate Hike and Yield Curve Inversion

Source: FactSet, as of 1/9/2015.

Presently, the difference between fed-funds and the 10-year Treasury yield is more than 2 percentage points. Barring a massive hike, , one or even a few rate hikes won't close that gap materially, even if long rates don't budge.

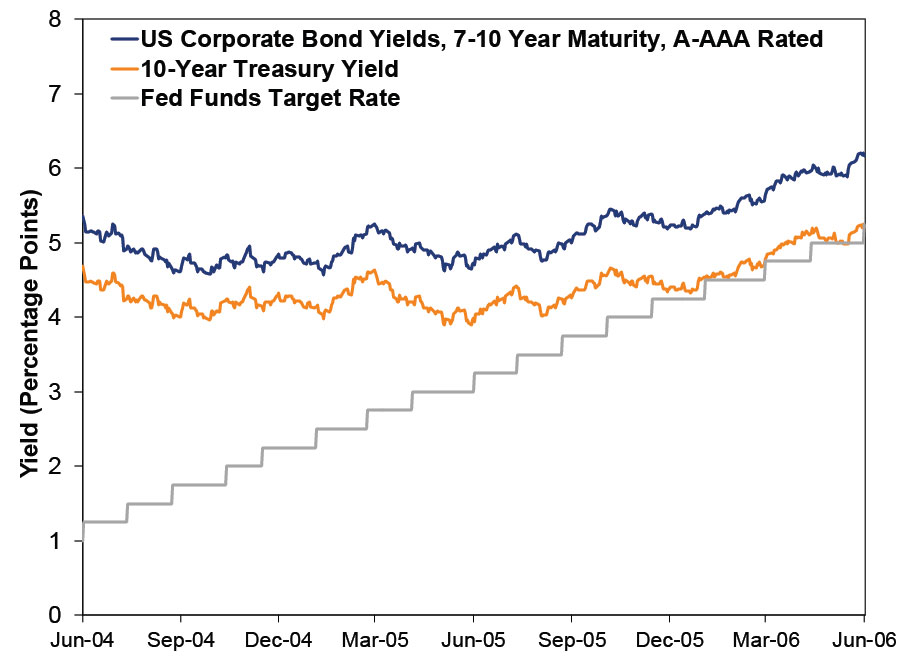

Which brings us to another fallacy: That rising short-term interest rates will send long-term rates skyward (on corporate and US government debt). They may rise, they may not! Exhibit 4 shows US A- to AAA-rated long-term bond yields, 10-year Treasury rates and the fed-funds target rate during the 2004 - 2006 tightening cycle. The Fed hiked 17 times, yet neither corporates nor Treasurys saw materially higher rates. Besides, if long rates always moved in lockstep with short rates, the yield curve would never invert. Yet, as shown above, it does.

Exhibit 4: Corporate Rates, Treasury Rates and the Fed Funds Target Rate, June 2004 - June 2006

Source: FactSet, as of 9/15/2015.

When false fears grab attention, the most bullish outcome is for them to happen fast, proving the fears false and allowing sentiment to brighten. That didn't happen Thursday, but it doesn't mean the bull won't continue. It just means we'll likely have to deal with even more handwringing and misguided Fed fears next month or in December. We'd recommend trying to stay above that fray.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Economics Quick Hit: Durably Broad-Based Growth2026-07-29

-

Market Analysis On the Chop in the Oil Market2026-07-29

-

Politics Takaichi Raises Japan’s Wall of Worry2026-07-27

-

In The News Why Kevin Warsh should think twice about hiking interest rates — even as anxiety over the Iran war grows2026-07-27

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today