Personal Wealth Management / Market Analysis

The Fed’s ‘Strategy Refresh’ Mirage

The Fed’s new inflation targeting approach is less than meets the eye.

For a decade now, the annual central bank conclave at Jackson Hole has been one of the most-watched financial events, with commentators salivating over the potential for major announcements from the Fed or its global friends. This year, COVID rendered the event one big Zoomfest, with no boon for that lovely mountain town’s hospitality industry. But the content didn’t disappoint Fedwatchers, as Chair Jerome Powell introduced the Fed’s new monetary policy framework. Some hail this as a landmark shift, but we think that vastly overrates it. Actually, we don’t think it changes much at all—for the economy or markets.

Specifically, the Fed updated its “Statement on Longer-Run Goals and Monetary Policy Strategy.” To see the difference, you can track changes here, but there were two main shifts in how it pursues its mandate to foster maximum employment and price stability. Before, “deviations” from the Fed’s estimate of maximum employment and its 2% y/y inflation target guided policy decisions. Very roughly, if employment exceeded a shadowy threshold and inflation topped 2%, the Fed would theoretically raise interest rates. If employment and inflation were lower, that implied rate cuts (or at least holding them steady).

The new language supposedly means the Fed will address maximum employment “shortfalls” and target “inflation that averages 2 percent over time.” The popular simple interpretation is that the Fed won’t consider high employment as reason to hike rates anymore. Nor would inflation topping 2% for a month or two necessarily be grounds for a move. But we think the statement and explanation from Fed Chair Jerome Powell show some, ummmm, problems with that interpretation. It isn’t clear what “averages” means. Powell didn’t explain how it is calculating it. Also, what does “over time” mean? (Two months? Six? A year? More?) To us, this vagueness counters the popular notion that the change automatically means rates staying lower for longer.

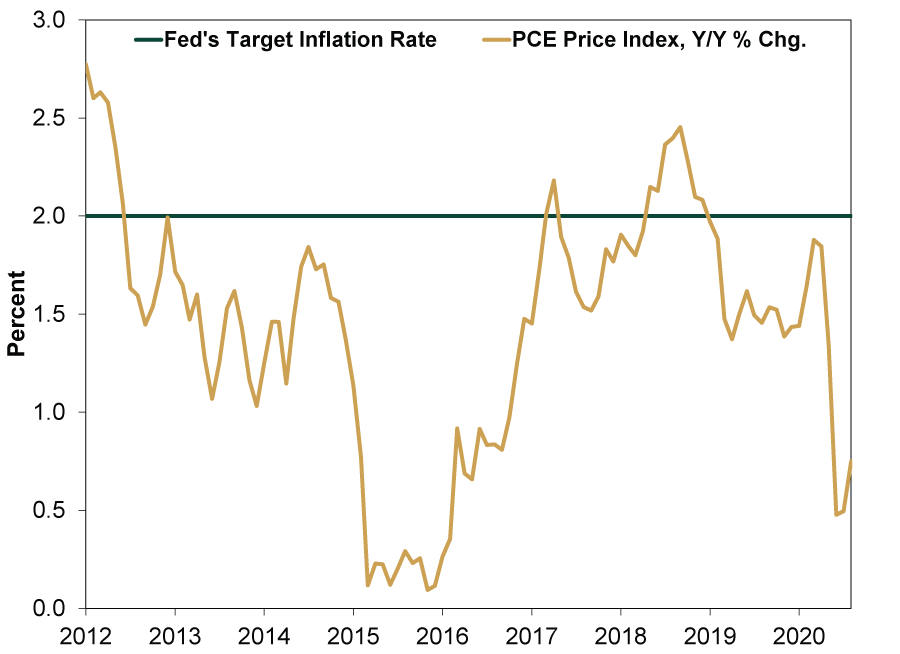

Our interpretation of this move is rather different. We think it reads more like the Fed is effectively ditching its 2% y/y inflation target, which it hit exactly three times since it became official in 2012. (Exhibit 1) For the most part, inflation chronically undershot.

Exhibit 1: Fed “Control” Over Inflation Is Spotty

Source: Federal Reserve Bank of St. Louis, as of 8/27/2020. Personal consumption expenditures price index, January 2012 – June 2020.

Averages are made up of extremes. So an average of 2% inflation “over time” could technically entail periods of deflation and high inflation, depending on the Fed’s definition. But one thing it doesn’t need to entail in pretty much any scenario is inflation consistently at 2%. We aren’t saying swapping the explicit target for something nebulous and squishy is good or bad. It is just funny to us how few Fedwatchers mention implementing an undefined target means you have no target at all.

Another under-noticed factor: The changes imply less confidence in the Phillips Curve—the theoretical tradeoff between inflation and employment—which is something it questioned for years as ultra-low unemployment didn’t generate fast inflation in the most recent expansion. We don’t think it is a mystery—inflation is caused by too much money chasing too few goods. Low unemployment may prompt companies to raise wages to attract talent, but they typically factor in inflation when doing so. Therefore, inflation causes rising wages, not the other way around, debunking the wage-price spiral. Tossing it out of the equation seems sensible to us.

In our view, the Fed’s new strategy seems mostly like window dressing and doesn’t help predict monetary policy moves. There is scant evidence 2% inflation was an obvious rate hike trigger anyway. Inflation was near zero in late 2015 when the Fed embarked on its last tightening cycle. Making a squishy rule it never much followed even squishier doesn’t lend great clarity into how Fed heads will set policy now.

Getting hung up on Fed jawboning isn’t terribly productive for investors. The risk of Fed error is omnipresent, but you always have to judge its actions after they are announced, and this move doesn’t change that. Nor does it yield any insight into its likely behavior.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary Why Ken Fisher Is Optimistic About European Stocks

2026-07-23

2026-07-23 -

Economics A Summertime Check-in on US Consumers2026-07-23

-

Politics Blunting Burnham?2026-07-21

-

Market Analysis Why the SOX “Bear Market” Isn’t Foreboding2026-07-21

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today