Personal Wealth Management / Economics

The Folly of Dissecting Fedspeak

The Fed never really penciled in four rate hikes this year.

Here is a big fear you might have seen recently: The Fed jumped the gun by hiking rates last December, and unless they back off from plans to hike four times this year, the economy and stocks are doomed. Well, they met Tuesday and Wednesday, didn't hike rates, and didn't change their forward guidance. Markets tumbled after Wednesday's statement release, and headlines blamed the Fed for not ruling out a March rate hike, even though it had a slightly dimmer view of the economy. As ever, it's impossible to pin any day's stock price movements on any one thing. But the broader obsession with the Fed allegedly penciling in four rate hikes this year seems blown out of proportion. One, a Fed that doesn't make knee-jerk reactions to market volatility is probably a more measured, thoughtful, confidence-inspiring Fed. Two, the Fed hasn't penciled in a darn thing.

The Fed did make some adjustments to its statement. Where December's statement described growth as "moderate," this one said it "slowed late last year." Consumer spending and business investment are now "moderate" instead of "solid." Gone was a statement calling risks to the economy and labor markets "balanced." In its place: "The Committee is closely monitoring global economic and financial developments and is assessing their implications for the labor market inflation, and for the balance of risks to the outlook." Most headlines interpreted this as a souring outlook. One called it a mea culpa for projecting four rate hikes this year. But it seems awfully presumptuous to speculate about the Fed's motivations when no one on the FOMC has actually said anything. Janet Yellen didn't give a press conference. We have zero interviews or soundbites. Reading between the lines thus strikes us as a fool's errand. For all we know, maybe the Fed just didn't want to sound tone deaf.

Parsing Fed statements and guidance won't get you anywhere, ever. Every move they make depends on data. Not forecasts, not internal projections, not a reading of the public mood. Just the FOMC's collective interpretation of the latest readings of economic growth, job growth, inflation and signals from global markets. (OK, maybe with a smattering of politics-as we'll explain.) This has always been true, and Janet Yellen and her Fed-head predecessors have always taken great pains to emphasize it.

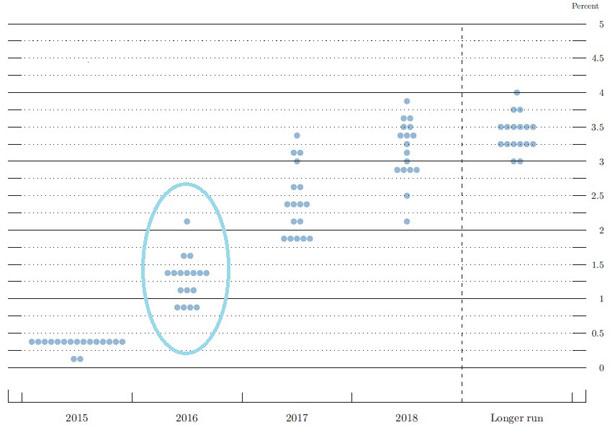

None of this conflicts with the Fed's supposed four-in-2016 rate hike forecast. Actually, the Fed never said it would hike four times. The world broadly misinterpreted its December 2016 projections. As usual, the Fed released its infamous "dot plot," which shows where each Fed Governor or regional President predicts the midpoint of the fed-funds target range will finish each of the next few years. For 2016, that dot plot looks like this:

Exhibit 1: FOMC Participants' Assessments of Appropriate Monetary Policy: Midpoint of Target Range or Target Level for the Federal Funds Rate (December 2015)

Source: Federal Reserve. "Economic Projections of the Federal Reserve Board Members and Federal Reserve Bank Presidents Under Their Individual assessments of Projected Monetary Policy, December 2015."

These dots are all over the map. Four Fed people think rates will finish 2016 under 1%. One thinks they'll top 2%. Seven think they'll be between 1.25% and 1.5%. That also happens to be the median forecast (rounded to 1.4%), and page one of the Fed projections lists the median forecast for various items. Hence, it attracted many eyeballs. And people did math: If the current fed-funds midpoint rounds to 0.4%, and they hike in 25 basis-point increments, then a midpoint of 1.4% would be four hikes away. And that, folks, is how "four in 2016" became a meme.

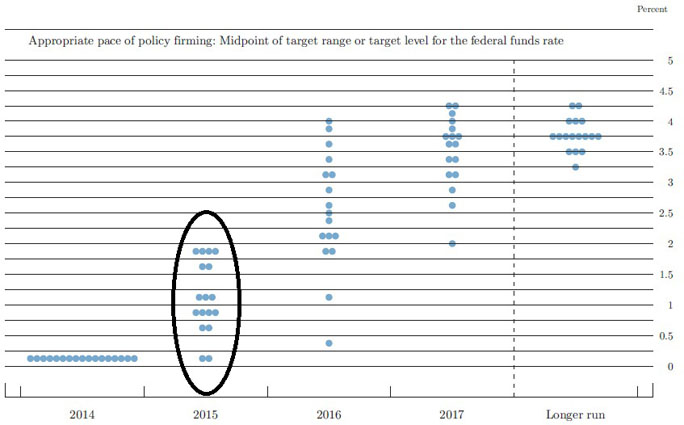

Thing is, those dot plots aren't carved in stone. The dots are movable! They move quarterly, as it happens, every time the Fed updates them. For instance, here is how the dots for 2015 looked in December 2014:

Exhibit 2: FOMC Participants' Assessments of Appropriate Monetary Policy (December 2014)

Source: Federal Reserve. "Economic Projections of the Federal Reserve Board Members and Federal Reserve Bank Presidents, December 2014."

That is worlds different from where we ended up. The median projection was 1.125%. Back then, the fed-funds target range was 0-0.25%, and the midpoint was 0.25%. Guess what: Using the same logic folks now employ, that was a projection for four rate hikes. In reality, they hiked once-at the year's very last meeting.

We fail to see why anyone should consider the current "forecast" any more telling.

How many times-if any-the Fed hikes this year will depend on what happens from here on. How fast the economy grows, how inflation and inflation expectations evolve, how unemployment behaves, (ideally) what the yield curve looks like, how fast money supply and bank lending grow, and what the global risks to US growth look like. It will also depend on how 10 Fed people interpret all these data-interpretations based on their varying biases and opinions. Contrary to what they say, it is also likely to be influenced by the appearance Yellen and Co. want to present to the victor of November's Presidential election. After all, Yellen is up for reappointment next year.

There is no way to foretell any of this. Nor is there any way to know now whether hiking or not hiking would be more beneficial at any point this year. Trying as this may be, we must all wait, see how things progress, and weigh each decision when they make it.

That probably doesn't sound terribly comforting, so here is a silver lining: There is really no point in fretting the Fed today. The first few rate hikes in a tightening cycle are usually economic non-events. The yield curve today remains positively sloped, giving the Fed some breathing room. Given the election, Yellen has a pretty big incentive to take it slow-maybe wait until economic data improve and the stock market correction reverses before hiking again, so she can say "hey look the first one went ok after all!" Doing nothing could shore up her street cred and improve her job-retention chances.

Whether the Fed next hikes in March, April, June or any other month, the risk they overshoot and invert the yield curve seems quite low-and that is what ultimately matters most for markets and the economy. As long as long rates remain comfortably above short rates, banks will have plenty of incentive to lend, boosting money supply and helping the economy continue growing.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Politics Blunting Burnham?2026-07-21

-

Market Analysis Why the SOX “Bear Market” Isn’t Foreboding2026-07-21

-

Expert Commentary 3 Things You Need to Know This Week | Q2 Earnings, ECB Meeting, Trump Accounts

2026-07-20

2026-07-20 -

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—July 13 - July 172026-07-20

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today