Personal Wealth Management / Market Analysis

The FOMC’s Rorschach Test

It was a Fed-filled week, here's a look back.

Wednesday was one of those days the financial press just goes nuts for. They live blog. Feature exclusive video. Previews lead up to it. Prognostications and analyses, fact boxes[i] and listicles detail what you should take away. It, we are told, is a really big deal. However, in our view, "It" is really just noise, and something investors would be well served to tune out.

In this case, "It" is the Federal Reserve's policy statement and the presser that takes place at the end of the biquarterly meeting of the Federal Open Market Committee, the (usually) 12-member committee that sets US monetary policy.[ii] The meeting has taken on a new aura in recent years, not because (as we are often reminded) the Fed did a lot of stuff in the years after 2008. But rather, because one of the specific things it did was release individual Fed member forecasts of expected economic conditions, unemployment and interest rates. The media loves forecasts, especially coming from a mysterious body so widely claimed to sit at the helm of the US economy, steering output and markets along the way. But this was a media dustup, pure and simple, and when the release of September's statement came, markets basically yawned. And moved on.

The run up to the meeting was rife with talk of "risky" semantics-a will-they-or-won't-they debate over whether the words "considerable time" would be in the statement. As in, would the statement keep this Hemingway-esque phraseology:

"The Committee continues to anticipate, based on its assessment of these factors, that it likely will be appropriate to maintain the current target range for the federal funds rate for a considerable time after the asset purchase program ends, especially if projected inflation continues to run below the Committee's 2 percent longer-run goal, and provided that longer-term inflation expectations remain well anchored."

Gripping stuff. The two bolded words' absence, some analysts claim, would imply the Fed would hike rates sooner. Their presence, later.[iii] So when the statement was released and the furious rampage of "Control-F" searching turned up the two magic words, the release was labeled dovish. The Fed, presumably, "is in no hurry to raise rates." So deep breath. And then everyone moved on to review the members' forecasts.

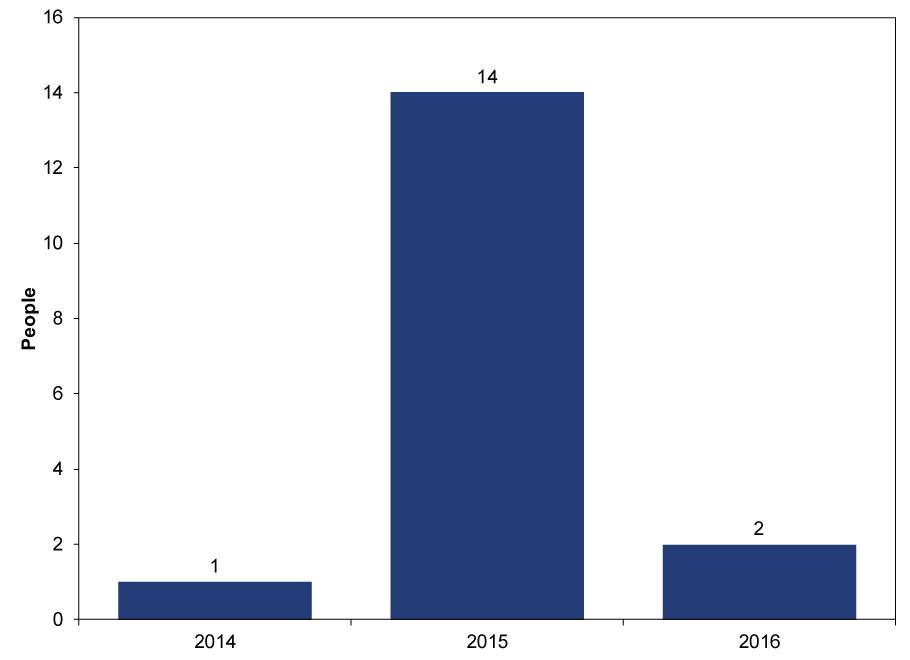

The first reviewed forecasts were of the timing of the initial rate hike. Viewers of the report were treated to this bar graph, which showed little change from the last.

Exhibit 1: FOMC Member Forecasts of Year of Initial Hike

Source: US Federal Reserve.

The majority of the FOMC (14 of 17 members-these surveys include non-voting members of the board) see rates rising next year, which has been the case since late 2012. No surprise. So media turned to the dot plot.

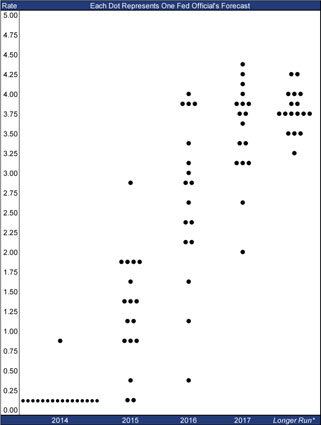

The dot plot is the individual Fed member's forecasts of interest rates, turned into a Rorschach-test-looking graph depicting Fed members' assessments of the trajectory of the economy and interest rates over the next few years. See what you can makeout of Exhibit 2.

Exhibit 2: The Fed's Dot Plot

Source: US Federal Reserve. Each forecast is in increments of 1/8th of a percentage point. *Longer run is a period of undetermined length beginning in 2018 at the earliest. It also looks like a carrot.

The media take on this is that it shows the Fed expects to hike rates faster than previously expected, based on that 2015 cluster between 1.125% and 1.375%. Some presume this poses a risk-that economic growth could be imperiled by such a quick rise. But before you formulate your own forecast based on the shapes above, consider: They are a moving target. Which some media sources already suggest, noting this faster pace won't be followed, rendering poring over all these charts completely unnecessary. (Perhaps that downward arrow formed by the 2017 dots was a subliminal message?)

This last point actually applies to literally all these forecasts. They are all subject to change. And there is little to suggest they won't change. Heck, even some of the officials making the forecasts won't be there by the time the forecast period is up, in all likelihood. And some new ones will come in! Who might have wildly different forecasts, designed to make you see a horse with a hat on in their dot plot.

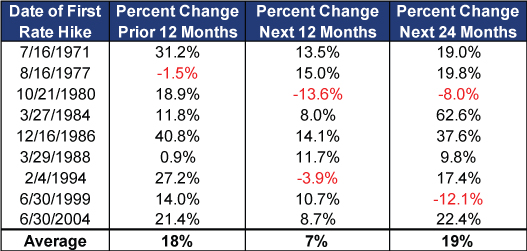

We are sorry to disappoint, but there is nothing to glean from the Fed's latest marketing effort, a chance to show the US how on the ball they are now, unlike 2008. For investors, that might seem like a let-down. But the thing is, stocks historically haven't been much impacted by the initial rate hike of a cycle. In the 12 months before, and the 12 and 24 after, markets tend to continue doing what they did before that first rate hike. (Exhibit 3) There just isn't much benefit in driving yourself crazy by reviewing the Fed's ink splotches.

Exhibit 3: MSCI World Returns Before and After an Initial Rate Hike

Source: Global Financial Data, Federal Reserve, as of 07/24/2014. MSCI World Index price returns in the 12 months before and the 12 and 24 months after the initial hike of the last nine tightening cycles.

Stock Market Outlook

Like what you read? Interested in market analysis for your portfolio? Why not download our in-depth analysis of current investing conditions and our forecast for the period ahead. Our latest report looks at key stock market drivers including market, political, and economic factors.

[i] Which are ironically packed with speculation and opinion, the opposite of facts.

[ii] There are currently two vacant seats, which some actually and oddly think is President Obama's chief economic mistake.

[iii] Bizarrely, no one questioned the grammatical implications of omitting those two words only. Like, "it likely will be appropriate to maintain the current target range for the federal funds rate for a after the asset purchase program ends ..." makes no sense. Which raises a non-goofy question, what would they have replaced it with? That stone, too, was left unturned.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary Why Ken Fisher Is Optimistic About European Stocks

2026-07-23

2026-07-23 -

Economics A Summertime Check-in on US Consumers2026-07-23

-

Politics Blunting Burnham?2026-07-21

-

Market Analysis Why the SOX “Bear Market” Isn’t Foreboding2026-07-21

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today