Personal Wealth Management / Market Analysis

The Next Big Fed Fear

First folks feared the end of quantitative easing, then the first rate hike. Up next: the shrinking of the Fed's balance sheet.

Fed head Janet Yellen will soon have more big decisions to make. Photo by Chip Somodevilla/Getty Images.

The Fed hasn't even begun hiking rates yet, and already some folks have moved on to the next big Fed fear: unwinding quantitative easing (QE). Though the Fed stopped adding to its balance sheet last October, it has continued reinvesting the proceeds from all maturing bonds to keep it at the same level, around $4.5 trillion. But in its September 2014 meeting minutes, the FOMC "indicated that it expects to cease or commence phasing out reinvestments of principal on securities held in the System Open Market Account after it begins increasing the target range for the federal-funds rate," and that rate hike now looms. Since conventional wisdom holds that QE pumped up stocks for nearly six years, some now fear a Fed balance-sheet taper could puncture this bull market. This gives QE far too much credit, in our view. Stocks rose despite QE, not because of it, and while Fed mistakes are always a risk, a slow unwinding of its balance sheet needn't spell disaster.

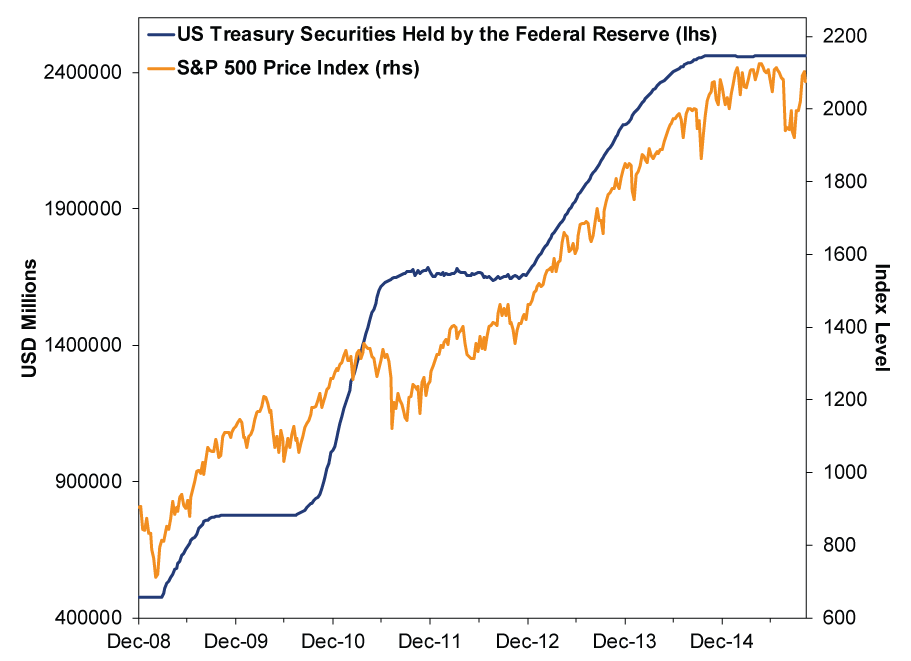

Exhibit 1, which recreates a chart we've seen (in various iterations) a few times over the past few months, shows why folks are getting worried. It is also a shining example of correlation without causation-and graphical funny business.

Exhibit 1: Stocks and QE

Source: Federal Reserve Bank of St. Louis, as of 11/18/2015. US Treasury Securities Held by the Federal Reserve and S&P 500 Price Index, weekly (ending Wednesday), 12/31/2008 - 11/11/2015.

Why funny business? Well, for one, the Fed's QE program included mortgage-backed securities as well as Treasury bonds, so this is an incomplete look.[i] Two, it's the S&P 500 Price Index, which excludes dividends, a big piece of total return. Three, the Y-axes have mismatching scales. It isn't hard to fiddle with Y-axes to make two lines look more alike than they should.

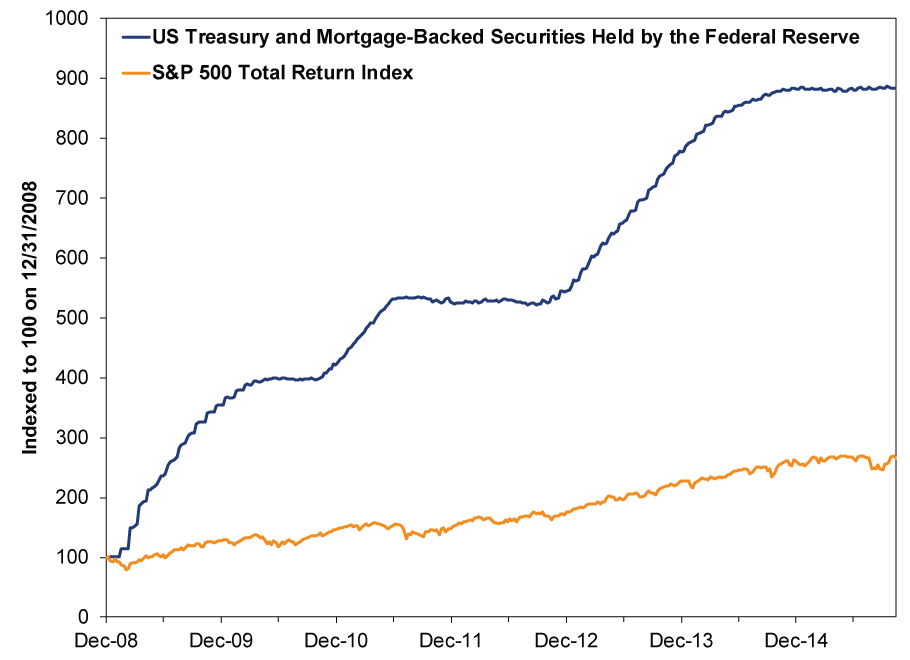

Exhibit 2 shows what we consider a proper version of Exhibit 1: Total QE and the S&P 500 Total Return Index, both indexed to 100 in order to show the cumulative percentage change in each.

Exhibit 2: Stocks and QE, for Real This Time

Source: Federal Reserve Bank of St. Louis and FactSet, as of 11/18/2015. US Treasury Securities and Mortgage-Backed Securities Held by the Federal Reserve and S&P 500 Total Return Index, weekly (ending Wednesday), 12/31/2008 - 11/11/2015. Indexed to 100 on 12/31/2008

When you view it this way, it is far less striking. The Fed's balance sheet increased nearly eightfold. The S&P 500, meanwhile, rose about 166%-not at all shabby, but not 800%.[ii] Also, stocks are actually up in each of the three cases the Fed ceased adding to its balance sheet. The S&P 500 rose 3.6% between March 2010 and QE2's launch on November 3, 2010.[iii] They rose a more robust 13.6% between QE2's end June 30, 2011 and QE3's launch on September 13, 2012.[iv] And in this latest go-round, US stocks are up over 5.8% since the Fed stopped adding to its balance sheet last October 29.[v] While those numbers may not blow you away, they should shatter the notion that stocks can't rise if the Fed isn't buying bonds aggressively.

If the Fed unwinds its balance sheet in a way that amounts to severe monetary tightening, then there could be trouble. While this is possible, it is far from certain, and given how tentatively the Fed has moved under Chair Janet Yellen, it would be quite out of character for the FOMC to decide to sell the farm overnight. Most Fed people have referred to simply letting bonds mature and naturally drop off the balance sheet. Those September 2014 Fed minutes even referred to gradually phasing out bond reinvestment, which would imply continuing to roll over some maturing bonds while letting others roll off. None of this tells you what the Fed will do, but it does suggest balance sheet normalization will be gradual.

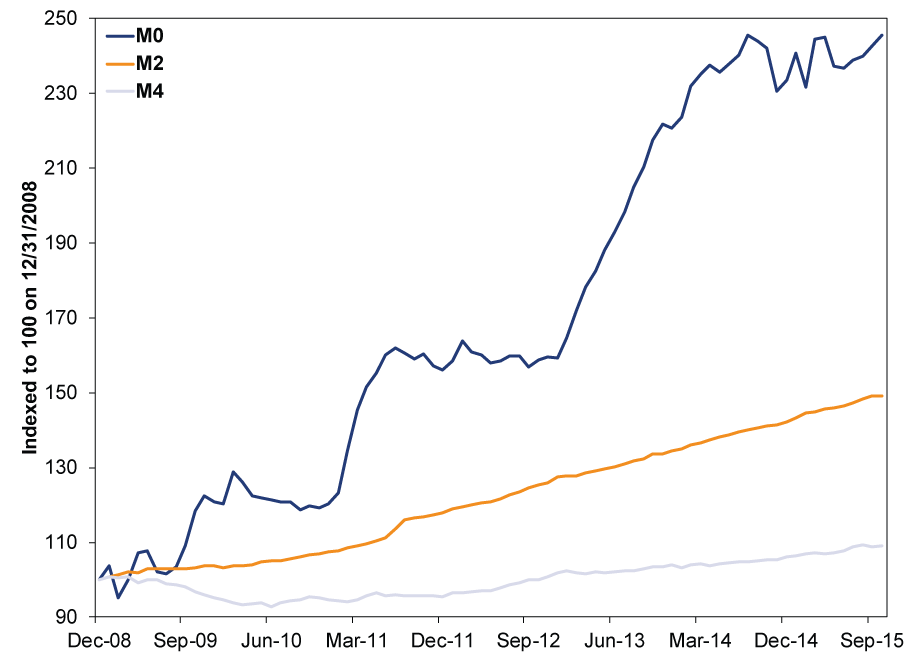

If so, that vastly reduces the risk of a sudden move. Also (bizarrely) working in the Fed's favor is the fact that very little of this QE money backed new lending. Most of it stayed on deposit at the Fed, gathering dust[vi]. As Exhibit 3 shows, this boosted the monetary base (M0), but not broader measures of money supply (M2 and M4).

Exhibit 3: Money Money Money

Source: Federal Reserve Bank of St. Louis and Center for Financial Stability, as of 11/18/2015. M0 (aka St. Louis Adjusted Monetary Base), M2 and Divisia M4, monthly, December 2008 - October 2015.

M0 grew about 145%. M2 grew about 49%. M4, the broadest measure, grew just 9%. M4 also accelerated after the Fed began tapering QE, as did loan growth.

This is all to be expected when you consider QE's impact on the yield curve. Fed bond-buying reduced long rates, flattening the long end of the curve and shrinking the spread between short- and long-term rates. Over 100 years of theory and evidence show a steep curve boosts growth, and a flat curve squashes it (a negative or inverted yield curve is usually a harbinger of recession in developed countries). Government yields are reference rates for interest rates in the banking world, so the yield curve is a proxy for banks' business model: They borrow at short-term rates and lend at long-term rates, and the spread between the two (aka their net interest margin) represents their profit on the next loan made. Banks aren't charities-they are for-profit institutions, and profits are their incentive to lend more. Slim profits when the yield curve was flatter encouraged banks to hunker down and take less risk. When the yield curve steepened and lending became more profitable, banks could begin lending more enthusiastically, to a wider swath of borrowers. That gave more businesses access to the financing they needed to invest and grow, a big reason US GDP has accelerated, overall and on average, since the QE "taper" began in January 2014.

While the Fed isn't adding to its balance sheet, refinancing activity makes it a major player in the market still and exerts some pressure on long-term rates. If the Fed stops buying, all else equal, it would remove one force weighing on long-term rates. That's especially important as the Fed hikes short-term rates. If long rates rise, it would prevent the yield curve from flattening, keeping conditions ripe for expansion. None of this is a given, as there are many other sources of US Treasury demand, but it's a point almost no one considers.

As with any Fed decision, investors will have to weigh the Fed's actions as they occur. All of the will-they-won't-they over ending QE and hiking short rates proves Fed moves are unpredictable. Basing portfolio decisions on a projection of what the Fed might do before they do it is fruitless and can do more harm than good. So, we'll all have to wait and see what they do. But for now, there is no reason to fear the Fed's shrinking its balance sheet will automatically imperil this expansion and bull market.

[i] Some versions show all of QE or all Fed balance sheet assets. We did it this way, because that's how it was portrayed in the most recent iteration we could find.

[ii] We feel compelled to point out that this calculation uses 12/31/2008 as the starting point, not the bear market's 3/9/2009 trough. The Fed bought its first QE securities in January 2009, so it would be inaccurate to begin our comparisons in March.

[iii] Source: FactSet, as of 11/18/2015. S&P 500 Total Return, 3/31/2010 - 11/3/2010.

[iv] Source: FactSet, as of 11/18/2015. S&P 500 Total Return, 6/30/2011 - 9/13/2012.

[v] Source: FactSet, as of 11/18/2015. S&P 500 Total Return, 10/29/2014 - 11/17/2015.

[vi] And 0.25% in annual interest.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary This Week in Review | Global PMIs, SpaceX, RMD Planning

2026-07-10

2026-07-10 -

Market Analysis Trim Your Angst on Economic Measurement Tweaks2026-07-09

-

Politics Long-Term Forecasts and Court Verdicts: The Latest in British and French Politics2026-07-09

-

Corporate Information How You Benefit from Fisher Investments' Transparent Fee Structure

2026-07-08

2026-07-08

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today