Personal Wealth Management / Market Analysis

The Paper Crunch

As the debate rages over how to regulate credit derivatives, let's look back at another time when a burgeoning market (then stocks) forced Wall Street to change how it did business.

Sometimes a year's leitmotif is all-pervasive, worming its way into happenings from Wall Street, to Main Street, to Watts. In 1968, the theme was upheaval and chaos. Martin Luther King, Jr. and Bobby Kennedy were assassinated as inner-city riots swept the nation. Meanwhile on Wall Street, a bear market was in the works as a number of securities firms flirted with collapse. But it wasn't the bear pushing companies to the brink—it was paper. A lot of it.

By the late sixties, the extended post-war expansion had the stock market growing weed-like—an estimated 20 million Americans were investing. An average 6 million shares traded daily by the end of 1965, 7.5 million by 1966, 10 million by 1967, and 13 million by 1968. June 13, 1968's 21 million shares traded trounced the previous single-day record of 16 million on October 29, 1929.[i] Yet, in contrast to all that quick growth, the mechanics of stock trading had barely budged in a couple centuries. Specialists still set prices on the trading floor; end-of-day reconciliation was by hand; every transaction required a stock certificate to transfer ownership; runners physically carried certificates firm to firm.

What should have been a welcome challenge proved too much for Wall Street's bulky back offices. Soon firms were setting up "suspense accounts" to hold the bits and pieces the paper trail couldn't identify. The NYSE was forced to take Wednesdays off and close early just to cope. Paperwork accumulated like snowdrifts—an open window and breath of wind would throw a hell of an expensive ticker tape parade. At its worst in 1968, $4 billion worth of securities were undelivered on their due date.[ii]

The pace was too much for the ponderous human mind to conceive let alone organize. But where flesh and bone were failing, a few pioneering computer scientists thought silicon might do better. Automated trading systems had first been studied in the fifties. Joseph Reilly, Chairman of the Committee on Floor Transactions at the Amex, was a major proponent of automation and proposed a new $3 million system in 1960. The way he saw it (quite accurately as it would turn out), as markets flourished in the sixties, the Amex could little afford not to automate. But Reilly's proposition was perfectly ill-timed. After assuming chairmanship of the Amex (an ideal position to push automation), scandal hit the exchange, with an SEC investigation hard on its heels. Automation was set on the back burner—not to be resurrected until it was too late.[iii]

As the major exchanges dragged their feet in the sixties, techies developed systems independently. Alan Kay devised AutEx in 1968. The system allowed operators to electronically transmit orders and fulfill them by phone. Jerome Pustilnik's Instinet went a step further by allowing users to remain anonymous and execute orders within the system. Instinet and AutEx signed up some institutional clients early on for over-the-counter transactions, but they faced significant headwinds at the NYSE. Automation threatened the specialists in charge of setting prices on the NYSE floor—the new technology would supplant human brokers with an electronic intermediary. It was the beginning of a decades-long struggle, ultimately resulting in today's lightning quick digital marketplace.

But more was needed in the interim. That's where the newly created Central Certificate Service (CCS) came in. Like a bank clearing house for checks (or recent proposals for credit derivatives), the CCS was a clearing house for stocks and central repository for certificates. Shares could now be held in "street name" on the books of securities firms. Transfer took place electronically by way of three IBM 360 computers and 500 office workers, netting positions daily and drastically reducing the paper backlog. [iv] (The CCS was eventually subsumed by the Depository Trust and Clearing Corporation (DTCC) in 1973.)

Automation and central clearing houses allowed the stock market to grow leaps and bounds in the coming decades. But they weren't enough to save the scores of securities firms facing bankruptcy or merger in the late sixties. The subsequent wave of failures forced a final notable change to Wall Street's archaic and unwieldy business model—one by one, the Street went public. The paper crunch proved traditional private partnerships just weren't scalable. Each year a few partners retired and took their slice of the pie with them. There was no way to know just what a firm's capital position would be year to year—capital improvements were therefore slow and unpredictable. And of course, the bankruptcies themselves left a sour taste. Owning shares in a public firm meant limited personal risk, multiple options for raising capital, and as far as expansion was concerned—sky was the limit.

The first firm to push the issue was Donaldson, Lufkin, and Jenrette. There was no law against a public firm becoming a member of the NYSE—just decades and decades of tradition. When Dan Lufkin was elected to the NYSE board of governors in 1969 and announced his firm was going public, he was greeted by a verbal barrage, punctuated by heckles of "Judas!" But he was determined—DLJ put their stock on the market in April 1970. Little did they know at the time, but one of the biggest names in the industry, Merrill Lynch, had the public model in mind too. Merrill soon followed DLJ into the public arena—with Charlie Merrill's successor, Don Regan, later exclaiming, "Those bastards stole my thunder!"[v]

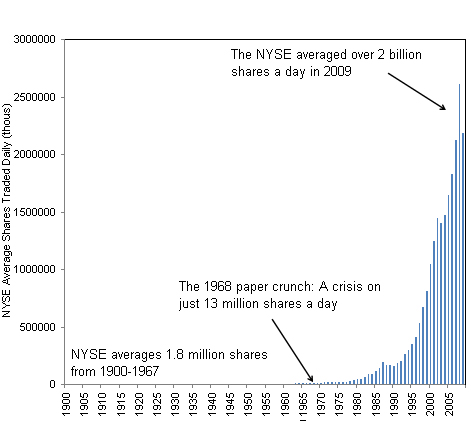

Over the next few decades, more securities firms went public and central clearing houses smoothed stock trading. But most dramatic of all—those fledgling attempts at automation grew into a formidable electronic marketplace, supporting billions of transactions round the clock. (The chart below depicts NYSE average daily share volume through 2009.[vi] Amazingly, the global market accounts for even more.) Stocks have come pretty far since stacks of paper first forced markets to marry microchips. Which is a good reminder: Not all change is bad change—and tradition for the sake of tradition should never trump pragmatism.

[i] NYSE daily share volume: https://bit.ly/aIaDkn

[ii] Greaves, CW. Forbes, "Forbes Sixtieth Anniversary Issue: 1917-1977." Page 96.

[iii] Sobel, Robert. AMEX: A History of the American Stock Exchange. Weybright and Talley, New York, 1972. Pages 245-246, 267.

[v] Eric J., Weiner. What Goes Up. Little, Brown and Company, 2005. Pages 108-125.

[vi] NYSE daily share volume: https://bit.ly/aIaDkn (1900-2003) and https://bit.ly/9DNlFy (2004-2009).

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Politics The Tenth Question Facing Alberta2026-08-06

-

Market Analysis Western Oil and Gas Producers Are Ramping Up2026-08-06

-

Corporate Information How You Benefit from Fisher Investments' Transparent Fee Structure

2026-08-04

2026-08-04 -

Corporate Information How Fisher Investments' High-Touch Service Helps You2026-08-04

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today