Personal Wealth Management / Market Analysis

The Real Lesson From Britain’s ‘Austerity’ Error

Last decade’s ‘austerity’ wasn’t quite what headlines imply.

Is the UK government about to repeat a terrible mistake? That question is stealing quite a few headlines in Britain as focus shifts from cushioning lockdowns’ economic impact to reining in 2020’s massive public deficit. Some pundits are lamenting the prospect of a capital gains tax hike, which one government commission recommended. But the vast majority are preoccupied with the potential for spending cuts, which they see as a repeat of the 2010s’ “austerity.” Conventional wisdom says big spending cuts under former Prime Minister David Cameron and his Chancellor, George Osborne—which continued under Osborne’s successor, Phillip Hammond—doomed the UK economy to a decade of lackluster growth. Cutting spending now, they argue, would repeat this error and cause the rest of the world to leave the UK in the dust after the pandemic fades. We don’t think it is worthwhile trying to predict what the government will do or how it will affect the UK economy, as there are just too many unknowns and human inputs. But a brief look at recent history might offer investors some helpful perspective.

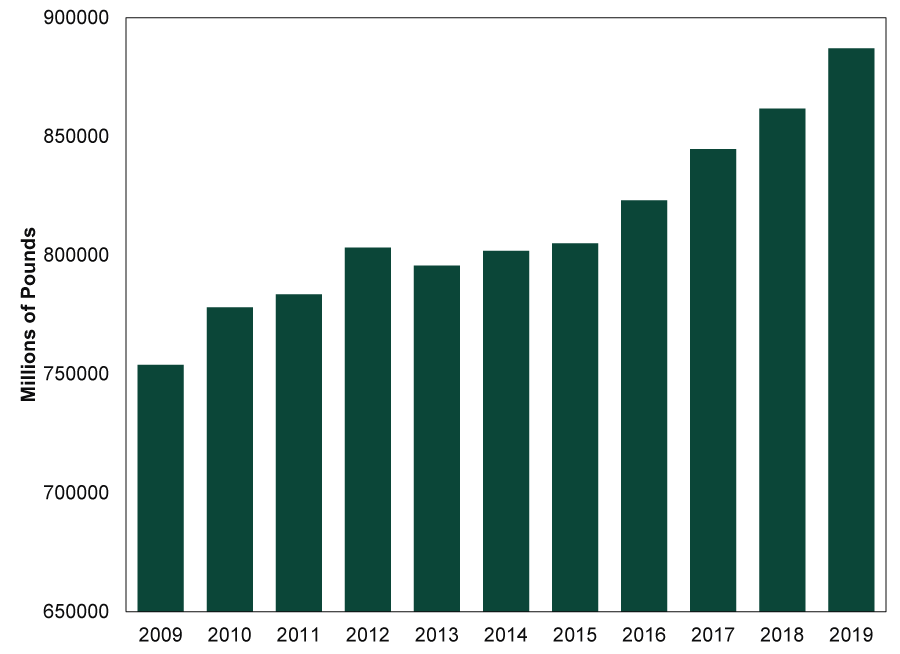

It is true that Osborne and Hammond stressed deficit reduction while in office, and they used the word “austerity” a lot. But as Exhibit 1 shows, their actions didn’t amount to austerity as most of the world would recognize it. There were no draconian spending cuts. Heck, annual spending fell in just one calendar year, 2013, and by only £7.6 billion from the year before—a -0.9% drop.[i] What actually happened is that Osborne edited his predecessor, Alistair Darling’s, plans and reduced the projected rate of public spending increases. Spending still rose, just not by as much as the prior government intended. We guess you could argue these fit under the loose definition of “budget cuts,” but editing a forecast isn’t a spending cut if actual spending doesn’t drop.

Exhibit 1: The UK’s Not-So-Austere Decade

Source: Office for National Statistics, as of 12/2/2020. UK Government Annual Total Managed Expenditure, 2009 – 2019.

One rebuttal we have heard when pointing this out over the years is yah, but a lot of that spending is transfer payments—those don’t count in GDP, so you should narrow your focus to get a better look. Fair enough, although much of the last decade’s commentary centered on benefit cuts as a major economic drag, hence our look at the total including transfer payment. But even looking at the government spending component of GDP, the picture doesn’t really change. That, too, fell in 2013 only, and not by much—just -0.5% from 2012.[ii]

The interesting thing about all this is that 2013 is when UK GDP finally accelerated after a fitful few years and flirtation with double-dip recession. GDP grew 1.3% in 2011 and 1.4% in 2012.[iii] In 2013, it sped to 2.2%, followed by 2.9% in 2014 and 2.4% in 2015.[iv] So if GDP accelerated the one year the UK had some actual austerity, it would be shortsighted not to ask why—and if there was another headwind during the earlier, lackluster years.

We think there is a simple answer to this: quantitative easing (QE). The BoE’s QE program ran from early 2009 to … drumroll … November 2012. Broad money supply and lending—particularly business lending—were negative for a big chunk of that stretch. They improved when QE stopped, which we don’t think is a coincidence. Through QE, the BoE purchases long-term UK government bonds, aka gilts. Those purchases drive long rates down. At the same time, the bank pinned short rates at 0.5%. When long rates fall while short rates stay steady, the yield curve flattens. That isn’t great for banks, which borrow at short-term rates and lend at long-term rates, making the yield curve spread a strong influence on their net interest margins (which is banking jargon for profit margins on new loans). Banks aren’t charities, so every lending decision considers risk and reward. Small margins reduce the potential reward for taking risk, which saps the incentive to lend to all but the most creditworthy firms. As a result, we think QE discouraged banks from lending enthusiastically to UK businesses. Like the US, the UK has a fractional reserve banking system, which means banks create most new money through lending. So when lending sags, so does broad money supply, which hamstrings economic growth overall. That, in a nutshell, is what we think happened in the UK—and when QE ended, broad money supply improved, the economy got more fuel, and GDP grew faster.

This is mixed news for investors today, we realize, considering the BoE is once again engaged in a massive QE program. Letting it expire next year—while letting businesses reopen—would bring a big economic net benefit, in our view, as it would likely let the UK’s flat yield curve steepen. (That viewpoint applies to the US, eurozone and Japan, too.) On the bright side, the 2010s also showed that while QE is an economic headwind, it doesn’t automatically derail bull markets. But overall and on average, we think the real repeat error is continuing the QE experiment, regardless of what Chancellor Rishi Sunak and his team decide to do on the public spending front.

[i] Source: Office for National Statistics, as of 12/20/2020.

[ii] Source: FactSet, as of 12/2/2020. UK General government spending growth in 2013.

[iii] Source: FactSet, as of 12/2/2020. Real UK GDP growth in 2011 and 2012.

[iv] Ibid. Real UK GDP growth in 2013, 2014 and 2015.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Politics Blunting Burnham?2026-07-21

-

Expert Commentary 3 Things You Need to Know This Week | Q2 Earnings, ECB Meeting, Trump Accounts

2026-07-20

2026-07-20 -

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—July 13 - July 172026-07-20

-

Market Analysis Pumping Up the Yen?2026-07-17

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today