Personal Wealth Management / Market Analysis

The Real War on Coal

What should investors make of proposed emission standards for coal-fired power plants?

Will new EPA regulations be a proverbial lump of coal for investors? Photo by Jeff J. Mitchell/Getty Images.

The so-called “War on Coal” heated up last Friday, when the EPA announced tougher emissions standards for new US power plants. Technically, the standards apply to coal and natural gas-fired plants, but officials have admitted coal plants are far likelier to breech the limit, causing some to suspect the government has picked coal to “lose.” We’ll not weigh in on the politics here, though—as ever, our focus is on the market implications of potential regulatory changes. And in this case, the likely impact on Materials and Utilities stocks seems muted. Coal has been losing a vastly different war for years, and the EPA’s new limits likely don’t much alter the fuel source’s course.

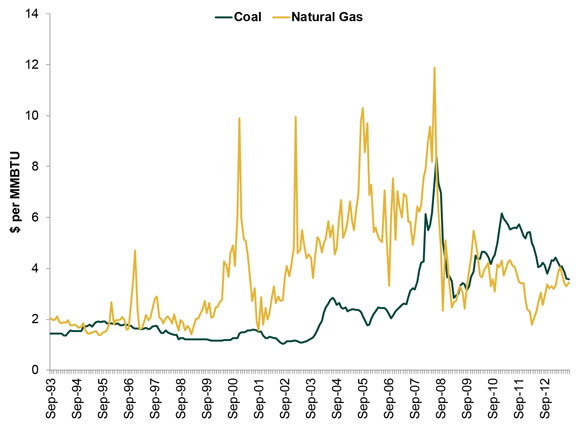

Coal’s real adversary isn’t regulators—it’s natural gas. Specifically, it’s the sheer economics of the shale gas boom. Thanks to the vast domestic supply, coal has long had a cost advantage over other fuel sources. However, advances in technology over the past decade unlocked massive amounts of natural gas, and the supply explosion has eroded coal’s benefits. Natural gas prices have plummeted—at points in 2012, gas was just below $2 per MMBTU. Today, they’re up to around $3.60, but that’s still far below where prices were a decade or so ago—and very competitively priced with coal, which has trended higher over the past decade. (Exhibit 1)

Exhibit 1: US Monthly Spot Price of Coal and Natural Gas

Source: Global Financial Data, as of 9/24/2013.

As a result, coal is poised to play a far smaller role in electricity generation. Exhibit2 displays additions to US electricity generation capacity from 1985 to 2011 and projections for 2012 through 2040. Natural gas has swamped coal since the mid-1990s, and its new market share is projected to widen over the next several decades. Yes, like all long-term forecasts, we’d suggest taking it with a grain of salt—any number of new supply developments could alter the energy landscape between now and 2040. But that natural gas’s massive supply and low relative cost caused coal’s expected market share to diminish long before the alleged coal crackdown materialized tells you just how feckless the new regulations likely are.

Exhibit 2: Additions to Electricity Generation Capacity, 1985 – 2040

Source: Energy Information Administration.

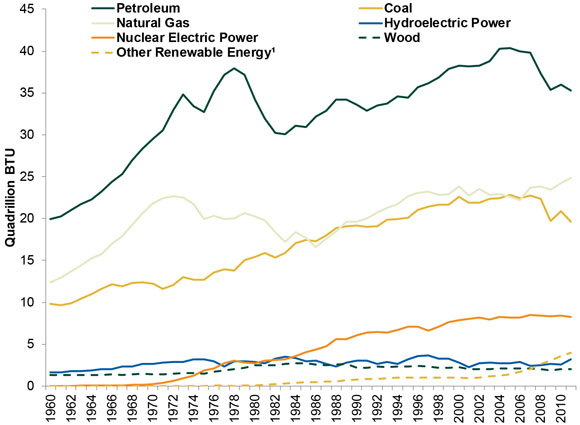

Coal isn’t losing ground just in terms of new capacity. As its cost advantage has evaporated, its share of electricity generation has (predictably) followed. As shown in Exhibit 3, coal has historically had an iron grip on electricity output in the US. Yet in recent years, it has declined while natural gas has risen. By year-end 2011, the US had 87 more natural-gas fired plants than in 2003—and 135 fewer coal-fired plants.i Today, natural gas powers about 25% more of our energy than coal does. (Exhibit 3)

Exhibit 3: US Primary Energy Consumption by Fuel Source, 1960 – 2011

Source: Energy Information Administration.

Since 2002, annual deliveries of natural gas to electric utilities grew from roughly 5 trillion cubic feet(tcf) to 9 tcf—with the jump from 7 tcf to 9 tcf coming between 2010 and 2012. Natural gas’s rise is accelerating. Meanwhile, coal deliveries to utilities fell. As did total coal production. According to the Energy Information Administration (EIA), coal production measured by rail cars loaded fell -7.8% y/y as of July 28, 2013. Beyond a short-lived, post-recession bounce back, coal production has barely rallied with the growing economy. Coal has been declining for a while.

Hence, jitters over the potential carbon cap seem overwrought—the issue is more political than economic, in our view. Yes, the Obama administration on more than one occasion has argued for reduced reliance on coal as a means of generating electricity, with a goal of reducing carbon emissions. And yes, the EPA’s press release hinted restrictions targeting these existing power plants may soon follow. But market forces are already prodding electricity generation away from coal to natural gas, just as they’re shifting providers from petroleum to gas. Oil has lost even more market share than coal in recent years—yet no one talks about a war on oil! It’s all political. Markets have a much stronger track record than governments of making outdated industry go the way of the dodo.

Still, the domestic coal industry is under pressure—natural gas’s ascension is a headwind. Yet all is not lost for America's coal producers. Coal is still heavily in demand abroad, particularly in Emerging Asia, where it will likely take some, if not many, years before the power grid shifts away from the cheap, easy to import substance. It likely does add to the pollution of Beijing, for example, that China is very reliant on coal-fired utilities, but there isn’t a readily available alternative. Europe, too, is consuming vast amounts of coal—particularly in Germany, which needed a cheap replacement for nuclear after Chancellor Angela Merkel’s government took plants offline in the wake of Japan’s Fukushima-Daiichi nuclear disaster. Japan, too, is burning more coal than ever. As a result, US coal exports at levels not seen since 1991. Granted, this has not fully offset declining US consumption, but global demand can help support coal production in America's heartland regardless of what US regulators decide. And it likely can continue doing so for quite a while, given other nations are only beginning to explore for shale gas—it could take years for prospective shale developments in the UK, Germany, China and elsewhere to match output from the US’s Marcellus, Haynesville and Barnett shale developments.

Not that coal producers are a surefire winner for equity investors over the next 12-18 months—Materials companies, in general, face a host of pressures. However, fears tougher emissions standards will cause the industry’s demise should prove overwrought.

i Source: Energy Information Administration. “Annual Electric Generator Report” for 2003 – 2011.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Economics Don’t Doubt the Old World2026-07-16

-

Market Analysis Business Friendly Bureaucracy or No, Britain is Growing2026-07-16

-

Market Analysis On the June Inflation Cooldown2026-07-14

-

Expert Commentary 3 Things You Need to Know This Week | US Inflation, China GDP, US Retail Sales

2026-07-13

2026-07-13

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today