Personal Wealth Management / Economics

The Record-Setting May Economic Data That Should Bore You

May’s PMIs tell a widely known story, in our view.

May purchasing managers’ indexes (PMIs) have rolled in, and some readings are historic. While we enjoy a nice milestone as much as anyone else, PMIs are still backward-looking, and the latest batch reveals basically nothing new or surprising. We think markets are looking far beyond what these data show—and investors should, too.

PMIs are surveys in which services and manufacturing businesses indicate whether activity across a range of categories rose or fell from the prior month. Readings above 50 mean over half of responding companies reported growth, implying broad expansion, but that isn’t airtight since PMIs don’t measure growth’s magnitude. So while we don’t know how robust May’s manufacturing growth was, PMIs suggest factory activity was very broadly growing, with a couple of exceptions.

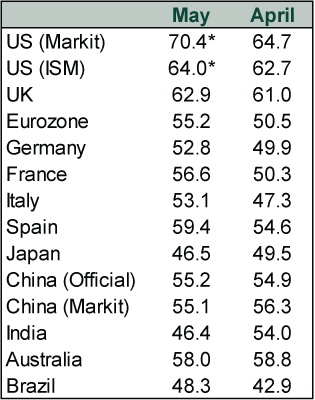

Exhibit 1: May and April Manufacturing PMIs

Source: IHS Markit, the Institute for Supply Management and the National Bureau of Statistics of China, as of 6/3/2021. * denotes series high.

While record readings grabbed headlines, some common themes emerged, as manufacturers in the US, UK, eurozone and Australia highlighted similar developments. Business was burgeoning thanks to reopenings and strong demand, but firms groused about well-known headwinds including delivery delays, soaring materials costs and capacity constraints. Record-setting aside, May’s numbers simply added to an ongoing trend: The COVID-driven demand for goods (and the components that comprise them) remains robust, leading to well-known shortages for semiconductors, timber and other “stuff.” However, this was notably a developed market trend: Factory activity hasn’t been as strong in Emerging Market countries still struggling with COVID outbreaks, including Brazil, Mexico and India. Brazilian manufacturing output did pick up after falling for two straight months, but Mexico’s PMI has been in contraction since February 2020. India’s PMI dropped from April’s 55.5 to 50.8 in May—barely expansionary—as the country grappled with a tragic second COVID surge. China, meanwhile, is back to its longer-running trend of moderate growth, which we think is a good preview for the rest of the world once the initial post-lockdown boom fades.

May’s services PMIs were generally not as robust as manufacturing’s, but this isn’t a big surprise given COVID restrictions’ disproportionate impact on services. While many factories shut during last year’s first lockdown, they stayed open through subsequent waves even as restaurants and retail shuttered again.

Exhibit 2: May and April Services PMIs

Source: IHS Markit, the Institute for Supply Management and the National Bureau of Statistics of China, as of 6/3/2021. * denotes series high. Notes: China’s official PMI includes both services and construction. IHS Markit doesn’t produce services PMI for Canada, Taiwan, South Korea and Mexico.

May’s services readings align with nations’ current COVID status—a seemingly obvious point. If businesses were closed or restricted due to virus measures—and those measures go away—reporting an uptick in activity and orders naturally follows. That was the case for both the US and UK, which credited strong demand to reopenings and vaccine rollouts. Eurozone services businesses have trailed their American and British peers—no shock given the Continent’s lagging vaccine distribution. In contrast, services activity fell where COVID restrictions returned. Japan’s services PMI remained in contraction as the country reinstated a state of emergency, and India’s PMI fell below 50 for the first time in eight months as the government reinstated COVID restrictions.

For investors, these data provide confirmation and color, but little else. Analysts have been anticipating—and yapping about—a reopening-driven boost since last year. Supply shortages and bottlenecks, delivery delays, capacity constraints and higher material costs aren’t great—but these issues have also hogged headlines for months. Ongoing COVID outbreaks are tragic, but their economic impact is well-known at this point. India’s crisis is likely affecting all facets of its society, including the economy. Japan, too, is grappling with rising cases—and headlines commonly wonder if the rescheduled Olympics are at risk. For both the good and bad stories, May’s PMIs confirm a reality familiar to nearly all. The findings rehash the top stories on the nightly news.

Rather than dwell on the latest numbers, we suggest looking ahead. Beyond the reopening pop these surveys and other data suggest Q2 GDP is highly likely to show in much of the West. Beyond the lingering COVID-lockdown issues in Japan and India. Beyond the temporary supply chain hit that is showing up virtually everywhere. There is nothing wrong with the data, but backward-looking numbers that confirm what we all already knew and expected should play next to no role in your view of stocks going forward.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis The New Tariffs in Town Are Still Old News2026-07-24

-

Expert Commentary This Week in Review | Market Volatility, Tariffs, SpaceX

2026-07-24

2026-07-24 -

Economics A Summertime Check-in on US Consumers2026-07-23

-

Expert Commentary Why Ken Fisher Is Optimistic About European Stocks

2026-07-23

2026-07-23

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today