Personal Wealth Management / Market Analysis

The UK’s New National Lockdown

Long-term investors benefit from considering a couple of key factors, in our view.

As if the world weren’t already on course for the saddest Halloween in recent memory, UK Prime Minister Boris Johnson announced on Saturday that England will enter a four-week lockdown on November 5. It is presently scheduled to end on December 2, but Johnson warned Monday it could extend well into 2021 if conditions warrant. The aim is, of course, noble—slowing COVID’s spread. But from the standpoint of near-term UK economic growth, this is obviously not good news. It will likely lead many to fear for UK stocks. However, for markets, we see a few mitigating factors that are worth keeping in mind if and when more countries or US states adopt stricter restrictions.

The first important consideration: This full lockdown isn’t quite as stringent as measures adopted in March. Yes, non-essential businesses (e.g., stores, hair salons and other personal services) must close, restaurants can serve takeout only, households can’t mix and people must limit travel to essential activities. But schools remain open—unlike in the spring. Factories remain open as well—another difference. Fiscal assistance is already in place. We aren’t going to call this “lockdown lite” or argue it is some whopping positive. But it is a mite better than the widely feared worst-case scenario where everything closes and the government has no help in place.

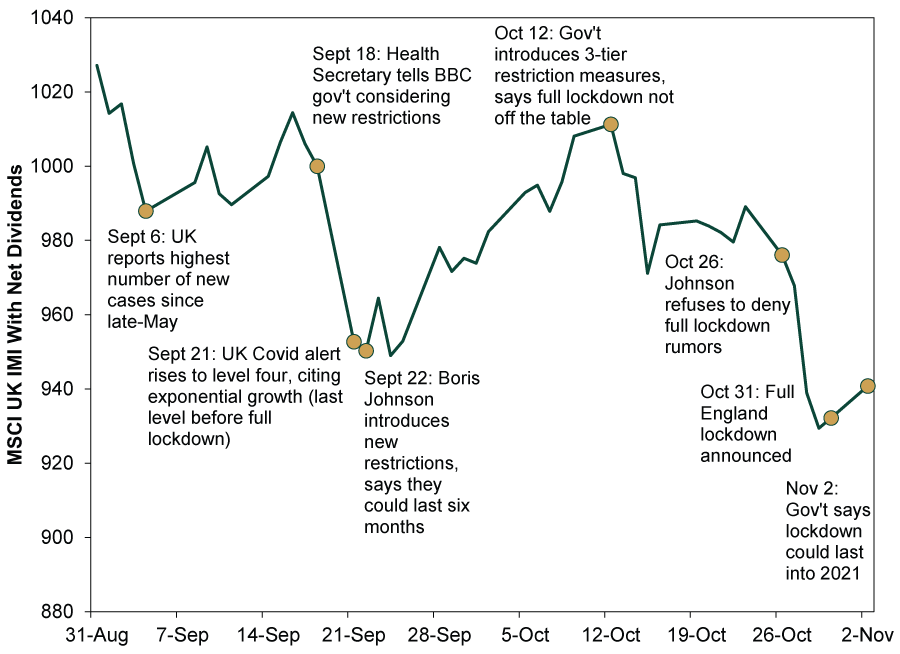

Second, and crucially for stocks, Saturday’s announcement wasn’t a surprise. We guess the fact UK stocks rose on Monday is one piece of anecdotal evidence supporting this, although we are loath to read into one day’s market movement. More compelling, in our view, is the timeline of UK COVID chatter over the past three months. As Exhibit 1 shows, the discussion flipped from reopening to potential new closures back in early September, and rumors of full lockdown have floated for about a month. France and Germany’s decisions to adopt nationwide measures last Wednesday further heightened UK lockdown fears. With the timeline laid over the MSCI UK Investible Market Index since the end of August, we think the extent to which stocks have been grappling with a potential new lockdown becomes clear.

Exhibit 1: Three Months of UK Lockdown Chatter and Market Movement

Source: FactSet and BBC News, as of 11/2/2020. MSCI World UK IMI with net dividends in USD, 8/31/2020 – 11/2/2020.

Note, however, that our belief UK markets have largely incorporated lockdown risk doesn’t much affect our expectations from a relative return standpoint. UK stocks have trailed during this young bull market not just because of lockdown risk, but also because of the country’s heavy tilt toward value stocks and large Financials exposure. Not only are Financials value-heavy, but UK banks face headwinds from the flat yield curve and potential for negative interest rates. Brexit uncertainty probably also continues weighing in the near term, although that is fading fast as yearend approaches. So by all means, keep a close eye on lockdown policies in the UK and globally. But at this juncture, we don’t think investors benefit much from letting any of this influence portfolio positioning.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis The New Tariffs in Town Are Still Old News2026-07-24

-

Expert Commentary This Week in Review | Market Volatility, Tariffs, SpaceX

2026-07-24

2026-07-24 -

Economics A Summertime Check-in on US Consumers2026-07-23

-

Expert Commentary Why Ken Fisher Is Optimistic About European Stocks

2026-07-23

2026-07-23

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today