Personal Wealth Management / Economics

The Well-Known Lesson From Q4 Eurozone GDPs

While GDP is backward-looking, the reaction is worth noting for investors.

Q4 GDPs for several eurozone nations have come out over the past week. Some noted the bloc’s return to pre-pandemic levels of output, but most focused on the slowdown due to Omicron. January’s purchasing managers’ indexes (PMIs) added more evidence of COVID measures’ impact, with some (correctly, in our view) noting growth will likely pick up as restrictions ease. To us, the broad discussion of restrictions’ economic impact shows how familiar society is with the script today. We believe surprises move markets most, and at this point, restrictions lack shock power.

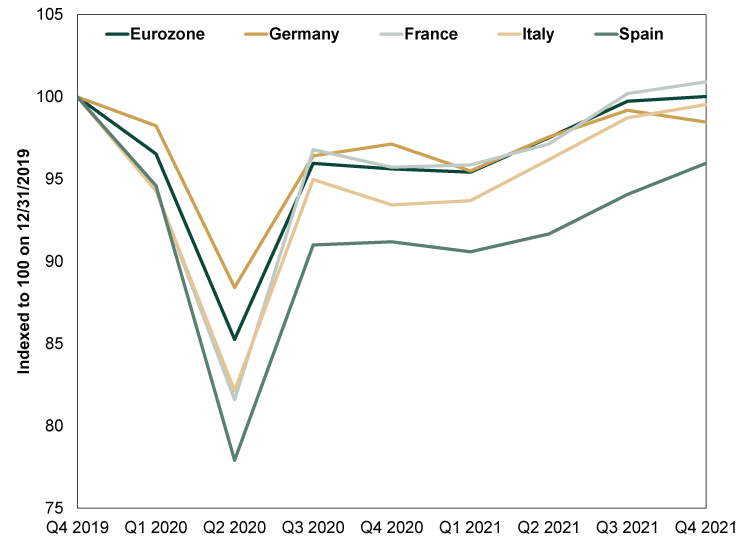

Eurozone GDP grew 0.3% q/q in Q4, missing expectations of 0.4% but enough to bring output above pre-pandemic levels.[i] (Exhibit 1) The bloc’s second-biggest economy, France, grew 0.7% q/q, while Spain (2.0%) and Italy (0.6%) also reported growth.[ii] However, Germany, long viewed as Europe’s economic engine, contracted -0.7% q/q.[iii]

Exhibit 1: The Big Four’s Post-Pandemic GDP Climb

Source: FactSet, as of 1/31/2022. Real GDP for eurozone, Germany, France, Spain and Italy, indexed to 100 on 12/31/2019.

That German dip grabbed the most attention. Though the Federal Statistical Office hasn’t reported the underlying components yet, the agency blamed the contraction on Omicron-related restrictions.[iv] Some experts expect economic struggles will continue in early 2022, and a few even forecast recession. Considering Germany is the largest eurozone economy, some think as it goes, so goes the region. But near-term German economic weakness doesn’t mean contraction is coming for the broader eurozone, much less the global economy. For one, the country’s heavy industrial base makes it uniquely vulnerable to supply chain problems. Since both manufacturing and exports comprise a larger share of German GDP than in France, Italy or Spain—as well as the broader eurozone—bottlenecks and shortages weigh more heavily on German growth.

Moreover, a local or regional economic soft patch won’t necessarily have broader global fallout. Japan endured recessions (using the popular definition of two consecutive quarterly GDP contractions) in late-2010 – early-2011, 2012 and 2019. In 2012, headlines bemoaned the UK’s “double-dip” recession (when GDP contracts for at least two consecutive quarters following a brief recovery from an earlier recession) after GDP shrank in Q1. However, all that fretting was misplaced after the ONS’s regular annual GDP revision in 2013 showed output was actually flat in Q1 2012—wiping away that downturn. At any rate, even when the world thought Britain had double dipped, UK stocks rose 9.0% that quarter—they were unfazed by the phantom recession.[v]

Even when US GDP contracted in 2011 and 2014, that didn’t spell trouble for the global economy or markets. Now, 2011’s Q1 and Q3 contractions did coincide with stock market corrections—short, sharp, sentiment-driven declines of about -10% to -20%—during the summer and autumn. However, fears surrounding the US debt ceiling and associated credit rating downgrade chatter, along with the eurozone’s debt crisis, played a bigger part in knocking sentiment, in our view, than US GDP’s small contractions. Furthermore, there was no correction in Q1 2014, when GDP dipped more than either of 2011’s brief contractions.

Now, Q4 2021 GDP won’t tell you much about the eurozone’s 2022 economic prospects, but pundits’ reaction can tell you about sentiment—and the handwringing over Germany’s contraction suggests skepticism remains prevalent. However, many analysts also expect growth to resume and even pick up once restrictions ease—and that has started happening. This week, France began lifting COVID measures, and Italy relaxed restrictions for travelers from EU countries. Denmark, though not a euro member, just became the first EU country to lift all COVID restrictions. Now, whether restrictions ease altogether or linger is impossible to handicap—human decisions defy prediction. But markets are much better at weighing the extent of the damage now than they were two years ago. Many now also know restrictions’ impact is fleeting. Forward-looking stocks have recognized this since March 2020, when a new bull market began despite nearly the entire West being in lockdown. Markets knew that even if restrictions returned—as they did in Europe in late 2020 and early 2021 and again this past December and January—they wouldn’t automatically pack the type of wallop from early 2020.

Restrictions could always hurt sentiment, as stocks can fall for any or no reason in the short term. But in our view, pundits’ recognizing that COVID restrictions may be a headwind—but one with a fleeting impact—is further evidence of progress towards a post-COVID future.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis The New Tariffs in Town Are Still Old News2026-07-24

-

Expert Commentary This Week in Review | Market Volatility, Tariffs, SpaceX

2026-07-24

2026-07-24 -

Expert Commentary Why Ken Fisher Is Optimistic About European Stocks

2026-07-23

2026-07-23 -

Economics A Summertime Check-in on US Consumers2026-07-23

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today