Personal Wealth Management / Market Analysis

The Yuan’s Rise Doesn’t Doom the Dollar

The dollar's status as the world's primary reserve currency is neither in jeopardy nor is it the benefit many folks think.

Is the yuan (or renminbi, if you so fancy) set for its international debut as a global reserve currency? According to the IMF, China's currency is "no longer undervalued," perhaps paving the way for inclusion in its Special Drawing Right (SDR) currency basket, possibly as soon as this year. Some nations-hello Hungary!-are gobbling up Chinese bonds in their foreign exchange reserve stockpiles. The flurry of yuan activity has sparked yet another round of fears the yuan will soon dethrone the dollar as the world's primary reserve currency, stripping America of the privileges most-held reserve currency status allegedly affords. Yet this doomsday yarn seems as unlikely to become reality as it did when fear first swirled six years ago. Even if the yuan did become number one, the implications for the US are slim. Primary reserve currency status doesn't prop the dollar or US debt.

The SDR (the IMF's bailout currency unit) basket is the blueprint for many nations' foreign exchange reserves. Investors see it as the IMF blessing a currency as deep, liquid and stable, a green light for foreign exchange (forex) reserve inclusion. The US is currently top banana in forex reserves and has been for decades, but China is seen as waiting in the wings-and if the IMF deems the yuan SDR-ready, many fear central banks nationally will ditch dollars for yuan overnight.

This seems quite far-fetched to us. For one, the yuan is not freely convertible worldwide. Its value is also pegged to the dollar, making it inherently unstable-not because the dollar is unstable (it isn't[i]), but currency pegs are. (See Switzerland, January 2015.) Though officials intend to free it up fully and open the capital account, the timing is fuzzy. It might happen this year, or it might take 10. This is one item the IMF is watching carefully. Two, nations don't hold paper money in reserves-they want stable[ii] assets with some return, and that usually means treasury bonds. The US has more government bonds in circulation than any other country with $13.1 trillion.[iii] Compare that to Japan[iv] ($8.7 trillion), the UK[v] ($2.2 trillion) and Germany[vi] ($830 billion). China trails most of these countries, with its gross central government debt amounting to about $1.3 trillion as of Q2 2013.[vii]

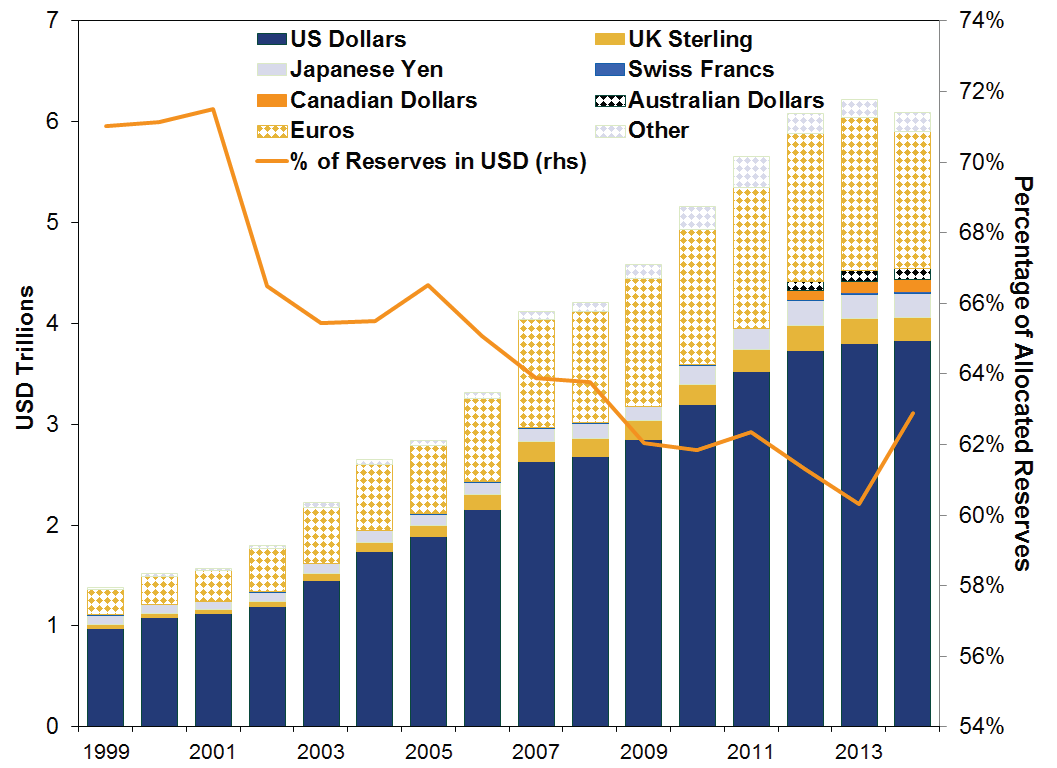

All that said, China probably will eventually gain forex reserve market share, though it wouldn't be the first currency to steal a bit of the dollar's thunder. Consider the humble euro, which has gone from 18% of reserves in 1999 to 22% last year. Meanwhile, the dollar's share fell from 71% to 63%. Yet actual USD holdings almost quadrupled, rising from just under $1 trillion to more than $3.8 trillion-the dollar just has a smaller share of a much bigger pie. There is no reason this can't continue as the world keeps growing.

Exhibit 1: Currency Composition of Allocated Foreign Exchange Reserves

Source: IMF, as of 6/4/2015.

Now, China has made progress toward a ready-for-prime-time currency. For example, it approved 32 foreign institutional investors into its bond market this year so far, up from the 34 approvals total last year, broadening its bond market's global accessibility. It will also reportedly roll out the Chinese International Payment System later this year, a worldwide system for "hassle-free" yuan payments-currently, the yuan accounts for just about 2% of payments across the world[viii]. The government has also steadily eased restrictions on cross-border capital flows, though it still has a ways to go. As former Fed head Ben Bernanke noted, "To move in that direction, China will have to continue to liberalize its capital account, current trading regimes, and strengthen and deepen its bond markets and other asset markets." While these are all long-term plusses for China's emergence in global markets, addressing them overnight could cause foreign fund flows to gyrate as market forces take over, and they might not be keen to test the economic impact while it's already trying to buoy slowing growth. The government also has a track record of moving methodically with reforms, using localized pilot tests before going national. They are about to test an open capital account and free yuan convertibility in the Shanghai free trade zone-and reforms there haven't exactly gone national at warp speed.

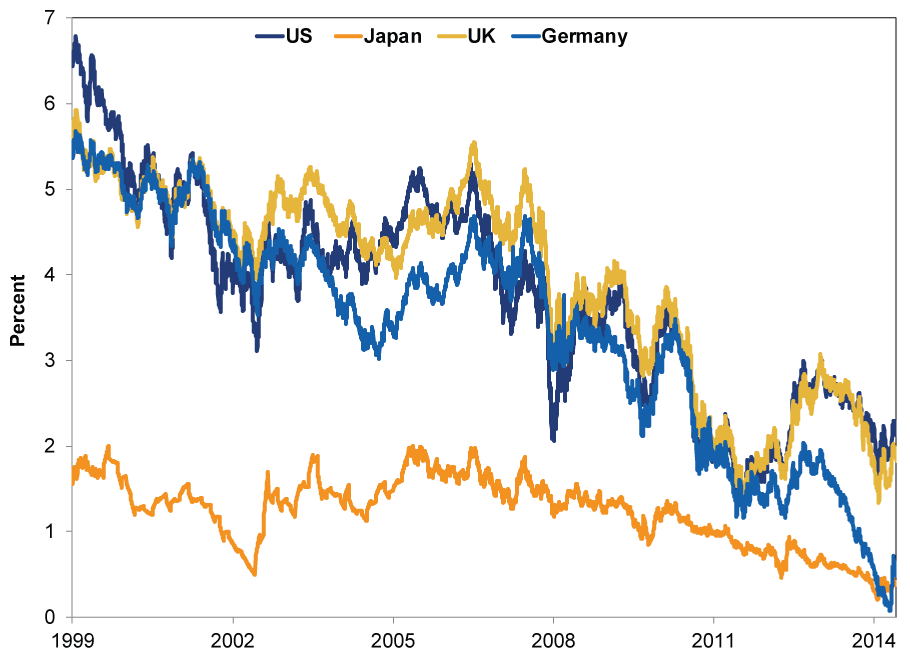

Whether China moves slowly or quickly, however, losing forex reserve market share isn't a negative for the US. The last 15 years are living proof. Many fear reserve currency status is the only thing keeping US Treasury yields down and debt sustainable, but that's a myth. If reserve currency demand were a huge interest rate driver, you'd expect US rates to be the world's lowest. Yet, among the countries[ix] privileged enough[x] to be in the SDR, US yields haven't been the lowest in the past 15 years-not even close. Being the world's primary reserve currency doesn't determine interest rates. (Exhibit 2) Heck, US interest rates actually fell as the dollar lost market share. They've also fallen since 2008, while the percentage of net US debt held in forex reserves steadily declined from 57.8% then to 29.3% now.[xi] Clearly, the US doesn't rely on foreign central banks to finance debt, which happens to be more affordable than ever. Domestic investors and international individual and institutional investors are a much bigger source of demand-and the total supply and demand landscape is what determines interest rates.

Exhibit 2: 10-Year Government Debt Yields for the US, UK, Japan and Germany

Source: FactSet, as of 6/8/2015. 10-year government debt yields from 12/31/1999 - 5/29/2015. The German benchmark bond 10-year yield is being used as a proxy for the eurozone, since no eurozone bond exists.

Rather than fret the yuan's rise, we'd cheer it. A freer currency in the world's second-largest economy is a plus for world trade, and stocks like robust world trade. Ditto China's emergence as a bigger player on global markets, which gives investors more opportunities. These are all very long-term positives, not swing factors in the here and now, but stocks always prefer more globalization, not less.

[i] To the extent anything in capital markets is ever stable, that is.

[ii] Ibid.

[iii] Source: US Treasury, as of 6/8/2015.

[iv] Japanese Ministry of Finance, as of 2/20/2015.

[v] UK Debt Management Office, as of 2/20/2015.

[vi] Deutsche Bundesbank, as of 2/20/2015.

[vii] Source: The World Bank, as of 6/9/2015. Gross central government debt isn't perfect, since it doesn't show much is actually marketable, but it's the best we can get since China doesn't report a more timely and detailed breakdown to the IMF or World Bank.

[viii] Ascendance on this front is another, related reserve currency fear, and it is equally baseless. The US gets nothing at all from the dollar's widespread use in international trade. Uncle Sam doesn't get a brokerage fee.

[ix] Four currencies are in the IMF's SDR basket: the dollar, the pound sterling, the yen and the euro. Obviously the eurozone is not a country-it is a 19-member bloc using the euro as its common currency.

[x] We are being sarcastic. As Bernanke noted, "If the yuan becomes an SDR currency it won't have any effect on the average Chinese. It's mainly symbolic."

[xi] IMF and Federal Reserve Bank of St. Louis, as of 6/8/2015. Forex claims in US dollars as a percentage of US net public debt.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary Why Ken Fisher Is Optimistic About European Stocks

2026-07-23

2026-07-23 -

Economics A Summertime Check-in on US Consumers2026-07-23

-

Market Analysis Why the SOX “Bear Market” Isn’t Foreboding2026-07-21

-

Politics Blunting Burnham?2026-07-21

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today