Personal Wealth Management / Market Analysis

Thoughts on Stocks’ Latest Pullback

New restrictions hit sentiment, but they remain a far cry from early 2020’s sweeping lockdowns.

Stocks had another rocky day Monday, bringing the S&P 500’s pullback to -3.0% in three trading days.[i] While short-term negativity can strike for any or no reason, most headlines blamed the Omicron variant’s surging case counts and a wave of new restrictions in Europe, not to mention anecdotal evidence of the virus curbing economic activity in major US cities. The prospect of stalling consumption and more supply chain hang-ups seemingly have investors globally in the doldrums. As ever, we don’t think it is possible to predict short-term volatility or how governments will respond to rising cases, as the political calculus varies from country to country. However, we do have compelling evidence that renewed restrictions don’t automatically sink stocks.

The variant may be different, but COVID policy throughout Europe this autumn looks a lot like it did a year ago, when the UK and most of the Continent were battening down the hatches in hopes of containing COVID’s second wave. The partial lockdowns ramped up in October, November and December 2020, and most countries extended them in full or in part through April 2021. They weren’t a repeat of the draconian, global measures in early 2020, but they were enough to deliver a temporary setback to the recovery. In the UK, GDP growth slowed from 17.4% q/q in Q3 2020 to 1.1% that Q4, then output contracted -1.4% in Q1 2021.[ii] German GDP followed a similar path, progressing from 9.0% q/q in Q3 2020 to 0.7% in Q4 and -1.9% in Q1 2021.[iii] As did Spain, growing 16.8% q/q in Q3 2020 before slowing to just 0.2% in Q4, then shrinking -0.6% in Q1 2021.[iv] France and Italy each contracted in Q4 2020 and barely grew in Q1 2021. The broader eurozone, which is about 15% of global GDP, shrank -0.4% in Q4 2020 and -0.2% in Q1 2021—a mild but true double-dip recession.[v]

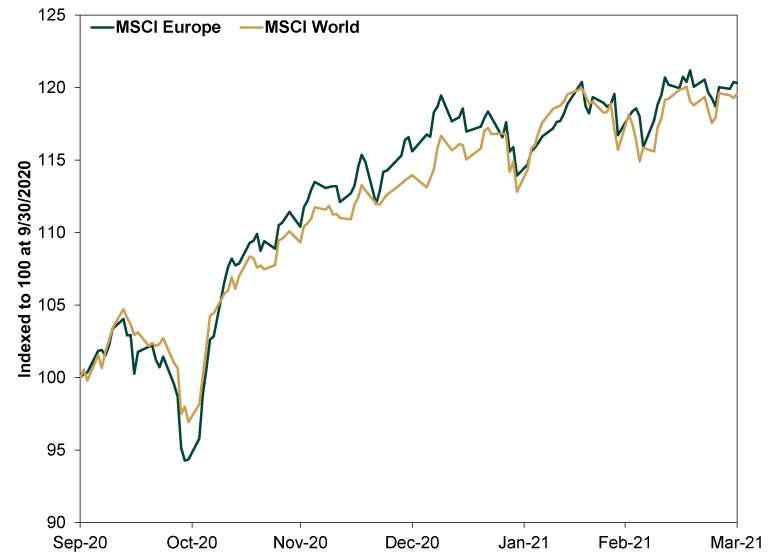

Yet stocks moved on well before that damage became apparent, finishing 2020 with a bang. As Exhibit 1 shows, European and global stocks did endure a brief pullback in October 2020, falling -9.4% and -7.4%, respectively.[vi] But they bounced fast, hitting new highs a week and a half after their lows. Even with its deeper pullback, the MSCI Europe Index soared 20.3% from 9/30/2020 to 3/31/2021, edging out the MSCI World Index’s 19.6%.[vii] Stocks quickly priced in the new restrictions’ likely impact, then moved on.

Exhibit 1: European and Global Stocks During COVID’s Second Wave

Source: FactSet, as of 12/20/2021. MSCI Europe and MSCI World Index returns with net dividends, 9/30/2020 – 3/31/2021.

Note, that doesn’t mean we think stocks will repeat this feat during the Omicron wave. COVID restrictions are but one variable at play right now, and any number of things could bog down sentiment. Again, short-term wobbles are unpredictable. But it does show new restrictions—even those causing economic contraction—aren’t auto-bearish. Plus, as it stands, this year’s restrictions largely remain looser than restrictions a year ago, which were much looser than early 2020’s lockdowns. The likelihood of a return to those dark days still looks very, very low.

Reacting to fearful headlines and short-term volatility is always an error, in our view. Capturing market-like returns over time—and achieving stocks’ long-term growth—is all about having the discipline to avoid getting fooled by temporary rough patches. This bull market hasn’t had a correction yet (a sharp, sentiment-fueled drop of -10% to -20%), and its ride higher has been unusually calm. Maybe that changes and this is the start of correction number one (or maybe not). If it is, remember corrections are normal and expected in bull markets, and their unpredictable nature makes them impossible to time with precision—at the beginning or end. Those who try often get whipsawed, selling after a decline and missing the recovery. If you are investing for long-term growth, those missed returns can be a setback.

So stay cool. Bull markets end one of two ways. Either they finish climbing the wall of worry and run out of steam when investors are euphoric, or something hugely bad and unseen wallops them beforehand. Neither condition is present today, in our view—rather, sentiment has downshifted amid a slew of false fears. We think that is a call for patience and discipline, lest you make a counterproductive knee-jerk reaction.

[i] Source: FactSet, as of 12/20/2021. S&P 500 price return, 12/16/2021 – 12/20/2021.

[ii] Source: FactSet, as of 12/20/2021.

[iii] Ibid.

[iv] Ibid.

[v] Source: FactSet and World Bank, as of 12/20/2021.

[vi] Source: FactSet, as of 12/20/2021. MSCI Europe Index return with net dividends, 10/12/2020 – 10/29/2020 and MSCI World Index return with net dividends, 10/12/2020 – 10/30/2020.

[vii] Ibid. MSCI Europe and MSCI World Index returns with net dividends, 9/30/2020 – 3/31/2021.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis The New Tariffs in Town Are Still Old News2026-07-24

-

Expert Commentary This Week in Review | Market Volatility, Tariffs, SpaceX

2026-07-24

2026-07-24 -

Expert Commentary Why Ken Fisher Is Optimistic About European Stocks

2026-07-23

2026-07-23 -

Economics A Summertime Check-in on US Consumers2026-07-23

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today