Personal Wealth Management / Economics

Three Years On, China’s Yuan Still Can’t Touch the Dollar’s Reserve Currency Status

What entering the IMF’s reserve currency basket did—and didn’t—do for the yuan.

Three years ago today, the IMF added China’s yuan to the basket of currencies underpinning its Special Drawing Rights (SDR)—its proprietary reserve accounting unit and means of extending credit to countries in need. At the time, the IMF touted it as “an important milestone in the integration of the Chinese economy into the global financial system.” Many investors took a less benign view, seeing the IMF’s move as threatening to end the dollar’s status as the world’s leading reserve currency—sending interest rates spiking and rendering US debt unaffordable. That was always a false fear, in our view, as the US gets next to nothing from having the world’s preferred reserve currency. Regardless, the yuan is still nowhere near unseating the dollar—and it isn’t likely to make a quantum leap anytime soon.

After World War II, the US used its newfound superpower status to help redesign aspects of international finance. The result was the World Bank, IMF and a standard that pinned the dollar to gold—and the world’s other currencies to the dollar. In the 1960s, then-French Finance Minister (later President) Valery Giscard d’Estaing referred to this dollar-centric system as an “exorbitant privilege.” He claimed it inflated demand for dollars and dollar-denominated assets—think Treasury bonds—affording the US government lower interest rates and more latitude to borrow. Even after the world ditched the gold standard in the 1970s, the dollar remained the principal reserve currency globally. Many folks have feared this status eroding over the years, thinking it would spell default on US debt. Earlier in this bull market, the yuan’s inclusion in the SDR was widely feared as a trigger event—after all, China’s economic clout has been rising. Many pundits thought adding the yuan to the SDR would drive central banks to add boodles of it to official reserves—at the dollar’s expense.

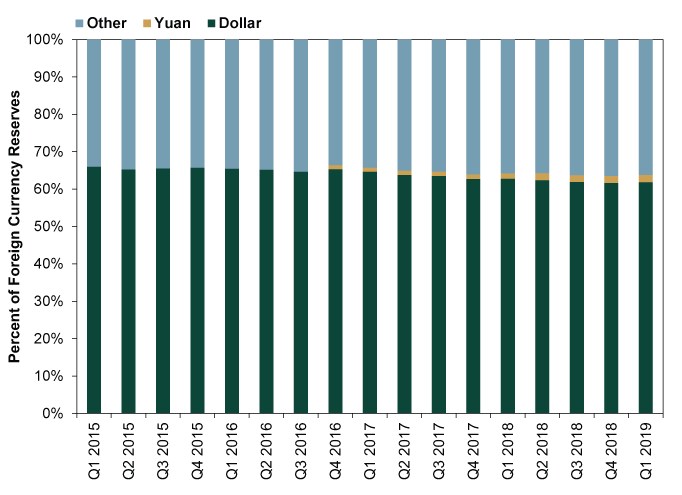

Yet the yuan has gained precious little market share since then. As Exhibit 1 shows, the yuan hardly rates in countries’ foreign exchange reserves.

Exhibit 1: The US Dollar Still Dominates Global Foreign Currency Reserves

Source: IMF, as of 9/19/2019. US dollar, yuan and other currencies’ percentages of allocated foreign currency reserves, Q1 2015 – Q1 2019.

Meanwhile, data from the Bank for International Settlements show the yuan’s share of foreign exchange turnover hasn’t much changed. US dollars were part of 88.3% of transactions in April, up from 87.6% in 2016, while Chinese yuan were only part of 4.3%, versus 4.0% three years ago. Maybe that changes going forward and the yuan takes some share from the dollar. But even if it does, that doesn’t necessarily mean the dollar is being used less in an absolute sense. With expansion, a bigger market means dollar usage can still grow even if it were a smaller percentage of transactions.

What matters for a currency’s reserve status isn’t what the IMF thinks of it, but whether it is freely convertible with sufficiently deep and liquid markets. The yuan doesn’t fit those criteria. The Swiss franc and Canadian dollar do—hence, they are in countries’ forex reserves despite their omission from the SDR.

Once upon a time, Chinese officials’ goal was to liberalize the yuan. In 2012, China made plans to loosen capital controls and make Shanghai into a global financial center. Those plans included eventually making the yuan fully convertible. They didn’t have a timetable, but for a few years, officials made progress. That April, they widened the yuan’s trading band, allowing it to rise or fall one percent on either side of the midpoint fixed by the central bank for that day. Three years later, authorities announced deposit insurance on up to 500,000 yuan and a pilot program allowing yuan to trade with few restrictions in China’s free-trade zones.

But in August 2015, China’s attempt to let the yuan float more freely backfired. The currency plunged, triggering fears of devaluation. To strengthen the yuan and stanch people potentially fleeing it, China tightened capital controls. In January 2016, regulators set daily and annual quotas on how much yuan people could exchange, limiting foreign exchange transactions. Restrictions added that November included capping corporate investments abroad. In January 2017, regulators announced measures amounting to tighter scrutiny of domestic and overseas money transfers exceeding 50,000 yuan (down from 200,000 previously), as well as tighter rules governing outbound investment by state-run firms. Just last month Chinese regulators announced they would more strictly curtail banks’ ability to send funds overseas if they deem the capital outflows “abnormal.”

China’s capital controls were well-known by the time the IMF deemed the yuan SDR-worthy, leading some to wonder why it moved forward. In all likelihood, it was aspirational. As the IMF said at the time, it “recognizes and reinforces China’s continuing reform progress.”[i] China had long sought inclusion in the SDR basket, deeming it an important milestone in the yuan’s journey toward the global stage. Adding it gave the IMF a bit of leverage to continue nudging Chinese officials toward full convertibility. Most global monetary observers agree that the freer and more integrated into the global financial system China’s capital markets are, the better it is for the global economy in general, as currency pegs are inherently unstable. If the yuan were to come under extreme pressure in the future—causing the peg to break—the shock to the world’s second-biggest economy could ripple globally.

The long-term benefits of a freer yuan aren’t the only reason we never bought into the yuan-dethroning-the-dollar fears. One, the yuan never looked likely to ascend to the top of the reserve currency food chain overnight. It is only 10.9% of the SDR basket, compared to the dollar’s 41.7%, euro’s 30.9%, yen’s 8.3% and pound’s 8.9%.[ii] Even then, forex reserves never mimicked the SDR basket. Before the IMF added yuan, the dollar was 41.9% of the SDR and 65.2% of total allocated forex reserves.[iii]

Most importantly, the notion that the US has low borrowing costs because of the dollar’s reserve status is false. For one, the US Treasury presently pays the highest long-term borrowing costs in the developed world. The Canadian dollar, Swiss franc and Swedish krona aren’t IMF reserve currencies, yet all have 10-year bond rates below the US’s.[iv] Featuring prominently in global trade doesn’t do anything for the dollar, either. It isn’t as if the Treasury gets a brokerage fee. The loonie, franc and krona are fine currencies despite not having anywhere near the dollar’s presence in global trade. America’s low rates are due to the US’s creditworthiness and investors’ desire to hold US Treasurys, which have the world’s deepest, most liquid markets. That alleged “exorbitant privilege” just doesn’t rate.

[i] “IMF Adds Chinese Renminbi to Special Drawing Rights Basket,” IMF News, 9/30/2016.

[ii] Source: IMF, as of 9/30/2019. SDR currency weights, 9/30/2019.

[iii] Source: IMF, as of 9/30/2019. SDR currency weights and US dollar percent of total allocated foreign exchange reserves, 9/30/2016.

[iv] Source: FactSet, as of 9/30/2019. Canada, Switzerland, Sweden and US 10 year bond government bond rates, 9/30/2019.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets — July 27 - July 312026-08-03

-

Market Analysis Digging Into Last Week’s Fed ‘Credibility’ Concerns2026-08-03

-

Expert Commentary 3 Things You Need to Know This Week | US Jobs, Trade Balance, Earnings Reports

2026-08-03

2026-08-03 -

Expert Commentary This Week in Review | Fed Meeting, US GDP, Eurozone GDP

2026-07-31

2026-07-31

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today