Personal Wealth Management / Market Analysis

To Gauge the Global Economy’s Health, Strip Out Commodities

Falling commodity prices are skewing global economic data downward, but they are not actually a net negative economically.

According to some big institutions with loud megaphones like the Fed and IMF, the world economy is weak, and they are worried about it. The media and punditry also took their turn, seizing upon recent data as evidence, from persistently low inflation in the US, UK and eurozone to China's most recent trade numbers. However, a closer look reveals the real story underlying these headline figures seemingly isn't a fragile world economy-it's falling commodity prices.

At first blush, the numbers look lackluster, and if you stop there, we can see why some might conclude a slowdown is in the offing, pressuring stocks. For example, pundits attributed some of equity markets' Tuesday slide to weak Chinese September trade. While exports fell a less-than-expected -3.8% y/y[i] (-1.1% y/y in RMB), imports dropped a whopping -20.5% y/y[ii] (-17.7% y/y in RMB). Yowza! At the same time, headline CPI readings remain low-and some countries are in deflation.[iii]UK September CPI fell -0.1% y/y, the second negative read this year. Eurozone August CPI slowed to 0.1% y/y from July's 0.2% y/y and, Thursday, the US Bureau of Labor Statistics reported September CPI fell -0.2% m/m-0.0% y/y-both downticks from August.

On the surface, these figures don't look great, but there is a benign cause worth taking into account: Falling commodity prices have skewed the year-over-year comparisons. Consider China's import numbers. While a -20.5% y/y import drop sounds huge,[iv] it isn't a huge outlier from the recent trend.

China's year-over-year import figures have been negative since November 2014. From January - May this year, they were often in the high negative teens.[v] Not coincidentally, last fall was when commodity prices really went off a cliff. And consider: Growth in import volumes was "comparable to the same time last year ," according to one Chinese analyst. China's iron ore imports are near record highs, and crude oil imports are rising. Demand hasn't fallen off a cliff-prices have.

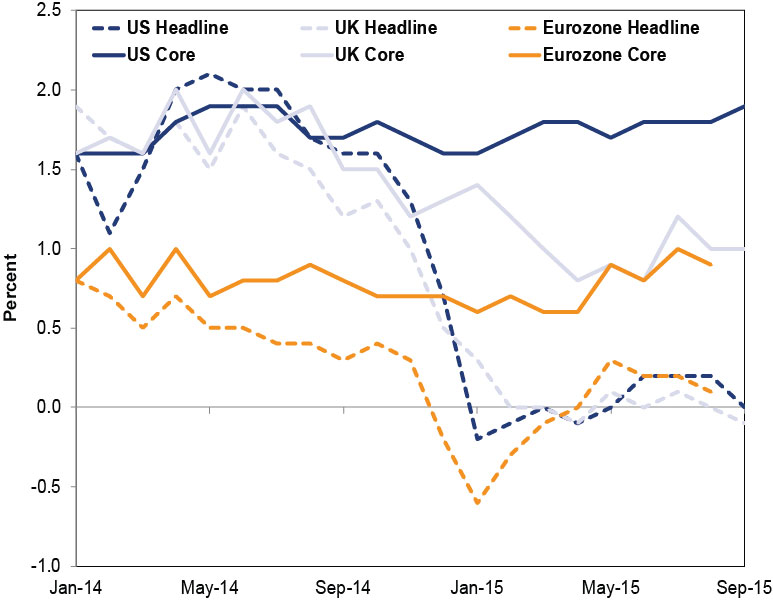

Falling commodity prices haven't just impacted trade. We see it in other data, too, including inflation and retail sales. Consider Core CPI, which strips out volatile components like energy and fresh food. UK Core CPI rose 1.0% y/y in September. Eurozone Core CPI rose 0.9% y/y in August. And US Core CPI sped to 1.9% y/y in September.[vi]

Exhibit 1: Headline and Core Inflation for the US, UK and Eurozone

Source: St. Louis Federal Reserve, Office for National Statistics and Eurostat, as of 10/14/2015. From 12/31/2013 - 9/30/2015. September 2015 readings for the eurozone not available yet.

While some interpreted September US retail sales (0.1% m/m) as a sign of tepid consumer spending, consider: Retail sales are a slice of total consumer spending-services comprise much more. And if you strip out gasoline station sales-which are down -17% in the last year-retail sales rose 0.4% m/m. That's better than near-flat. Other measures of spending show similar trends.

These data all reflect the decline in commodity prices over the past several years. Oil has grabbed the most headlines ever since its sharp decline began last summer, but commodities overall have been hit hard, largely due to a supply glut. Global supply has outpaced global demand, leading to falling prices. It takes a while to work through excess supply, and since Energy and commodities prices influence inflation gauges, China imports a lot of commodities and consumers spend at gas stations, this skews data worldwide.

While falling commodity prices hurt commodity producers, they are a positive for commodity consumers, mitigating input costs for firms and freeing up cash for consumers. For example, consider recent consumer spending stats for China's "Golden Week" national holiday. Restaurant and retailers' sales amounted to 1.082 trillion yuan[vii]-equivalent to Kuwait's total economic output in 2014. Domestic entertainment spending boomed and four million tourists traveled abroad, with Japan, South Korea and Thailand the most popular destinations. Low inflation boosts real wages, benefiting consumption-dominated economies like the US, UK and the eurozone.[viii] China has been shifting toward this direction, and the numbers from "Golden Week" serve as a nice counterpoint to fears of what a slowing Chinese economy means for the world.

In our view, this suggests many still aren't pricing in the oversized impact commodity prices are having on the data, leading to inaccurate conclusions about global macroeconomic conditions. Yes, commodity-oriented economies are hurting. But not all the world is commodity-oriented. You just have look closely at the data to see it.

[i] Source: FactSet, as of 10/13/2015. In USD.

[ii] Source: FactSet, as of 10/13/2015. In USD.

[iii] We'd argue this hasn't been very effective, but that's a topic for a different article.

[iv] It's both double-digits and a roundish number-easy to digest for readers

[v] In USD.

[vi] Note that core CPI in the US excludes food and energy prices, in the UK and eurozone it excludes food, energy, alcoholic beverages and tobacco.

[vii] Or about $170 billion.

[viii] And for those who think this hasn't been happening in the US, consider this report and the fact personal consumption expenditures excluding energy goods are growing nicely.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary This Week in Review | Global PMIs, SpaceX, RMD Planning

2026-07-10

2026-07-10 -

Market Analysis Trim Your Angst on Economic Measurement Tweaks2026-07-09

-

Politics Long-Term Forecasts and Court Verdicts: The Latest in British and French Politics2026-07-09

-

Corporate Information How You Benefit from Fisher Investments' Transparent Fee Structure

2026-07-08

2026-07-08

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today