Personal Wealth Management / Market Analysis

Uncertain About the Costs of Uncertainty

How do you measure that which is uncertain?

The shutdown is in week three, the debt ceiling is hours away, and—miraculously—the Senate seems to have reached a deal. Whether it passes both houses remains to be seen, though, so “uncertainty” persists. As does uncertainty over how the economy could fare if the deal collapses. Or, we guess, even if it does pass. After all, the debt ceiling will come again, and it’s not the only source of uncertainty in the world. Risk is something corporations and stocks can handicap, since it’s possible to plan for a known risk. Uncertainty is another matter—one reason stocks tend to dislike high levels of uncertainty. As a result of these perfectly valid theoretical points, one intrepid gang of academics has tried to quantify just how much economic policy uncertainty exists with hypothetical studies on what could have been if fiscal policy were different in recent years. They then apply their findings to assess what may be should the debt ceiling deal fail—a very slippery slope, in our view. Simulations on assumed circumstances may make for interesting academic debates or bar talk, but they have little, if any, bearing on reality—and shouldn’t be used to guide investment decisions.

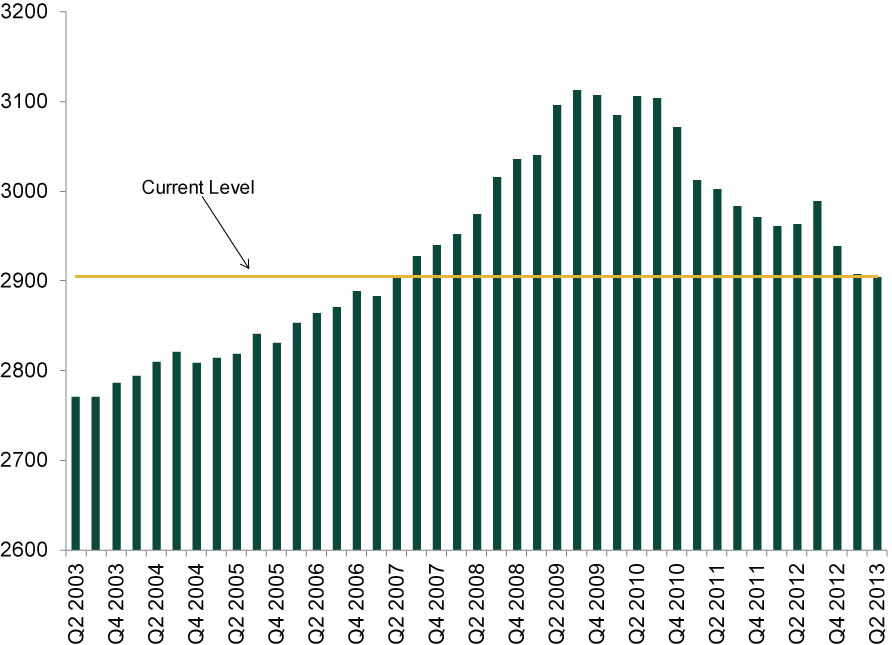

The report in question aims to quantify how much US fiscal policy has impacted economic growth in recent years. It starts with the obvious: Government spending cuts detracted from growth and employment. True! Though not necessarily the epic fiscal contraction the report suggests. As shown in Exhibit 1, current spending (adjusted for inflation) is in line with 2007 levels. With that in mind, a better interpretation of the cuts’ impact may be that officials have reversed the increased spending from 2009-2010’s fiscal stimulus, but the economy is still growing. Perhaps the spending simply shifted to the private sector. There’s no counterfactual to prove the point beyond a reasonable doubt.

Exhibit 1: Real Government Consumption Expenditures & Gross Investment Since 2003

Source: St. Louis Federal Reserve, as of 10/15/2013.

But a bigger issue than this framing is the use of hypothetical scenarios with unclear assumptions and inputs to estimate how “fiscal uncertainty” has weighed on the private sector—and applying the same approach to gauge how a debt ceiling breach could shock markets.

Using a modified version of the Economic Policy Uncertainty Index, the report concludes since 2009, fiscal uncertainty shaved GDP growth by 0.3 percentage point per year and erased some 900,000 jobs. Though the exact methodology isn’t provided, the approach seems flawed philosophically. The Economic Policy Uncertainty Index measures news mentions of economic policy and forecasters’ disagreement about government spending—it doesn’t measure how this impacted actual business plans. Did they interview any CEOs? Small business owners? Excluding real estate, US gross private domestic investment grew by nearly 45% from its Q3 2009 trough through Q2 2013.i Is there factual evidence businesses cut or delayed investment simply because of “fiscal uncertainty”?

The index itself seems a rather odd input, too. For one, it tries to quantify something—uncertainty—by definition unquantifiable. In doing so, the created index claims 2011’s debt ceiling debate somehow caused more economic policy uncertainty than existed in 2008, when the government swerved from buying “toxic” assets to investing in preferred stock to bail out the financial sector, outright took over Fannie and Freddie, quasi-nationalized parts of AIG and generally behaved in a wildly unpredictable fashion. 2008 also had a recession. Contrast that to 2011, when the economy grew during and after the debt ceiling debate. To us, 2008 seems a touch more uncertain than a debt ceiling debate that went more or less the way many debt ceiling debates have.

It also seems tough to argue, as the report does, fiscal policy has become more uncertain since 2011. If anything, things are clearer since then—with or without ongoing politicking over the debt ceiling and budget. Spending plans don’t get much more certain than the sequester—well-known a year and a half before it took effect. And the fiscal cliff resolution seemingly ends the nearly annual debate over extending the “Bush tax cuts.” Maybe you disagree with how these matters turned out, but they are known—not uncertain.

All of these flaws underpin the report’s claim of economic doom if Congress doesn’t address the debt ceiling. For this, they use another hypothetical—an arbitrary “global financial shock” applied to a “baseline” assumption of economic growth (based on CBO forecasts). Yet the report’s math isn’t shown, instead relying on the broad assertion the fallout will rank somewhere in-between the 2011 debt ceiling and the 2008 Lehman Brothers failure in terms of volatility. There’s a lot of room in between a correction and the biggest bear market in decades, though. This leaves one wondering what the exact assumptions are and how they were applied to business results?

Even if you were to assume breaching the debt ceiling is big and bad, this report’s guesstimate doesn’t pass muster. There are just too many layers of assumptions for solid conclusions to be reached. Evidence suggests not raising the ceiling for a while isn’t a disaster. We aren’t recommending Congress give it a go, but we strongly doubt the Treasury’s prioritizing payments for a while really much resembles “global financial shock.”

i Source: Federal Reserve Bank of St. Louis, Real Gross Private Domestic Investment minus Real Private Fixed Investment in Residential Real Estate, Q3 2009 – Q2 2013.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary 3 Things You Need to Know This Week | Q2 Earnings, ECB Meeting, Trump Accounts

2026-07-20

2026-07-20 -

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—July 13 - July 172026-07-20

-

Market Analysis Pumping Up the Yen?2026-07-17

-

Expert Commentary This Week in Review | US-Iran Conflict, US Inflation, New UK Prime Minister

2026-07-17

2026-07-17

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today