Personal Wealth Management / Market Analysis

Unconventional Drilling Techniques’ Impact on Energy Markets

The combination of two technologies and an old resource has created a US natural gas production boom.

Horizontal drilling, hydraulic fracturing, and shale gas have received a ton of press lately. But what impacts do these unconventional techniques have on energy markets?

Historical Perspective

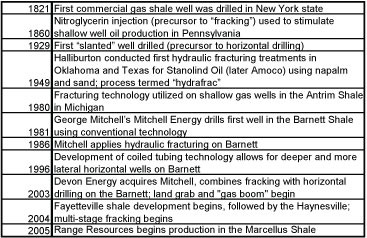

Neither hydraulic fracturing (fracking) nor horizontal drilling are new technologies—the first horizontal well was drilled in 1929 and Halliburton developed fracking in 1949.Shale gas extraction is even older—the first commercial well was drilled in 1821. However, when horizontal drilling and fracking were combined to drill in Texas’ Barnett Shale region in 2003, a natural gas boom was born. In the last decade, shale gas production has increased 14-fold.

Exhibit 1: Historical Milestones in Unconventional Gas Drilling

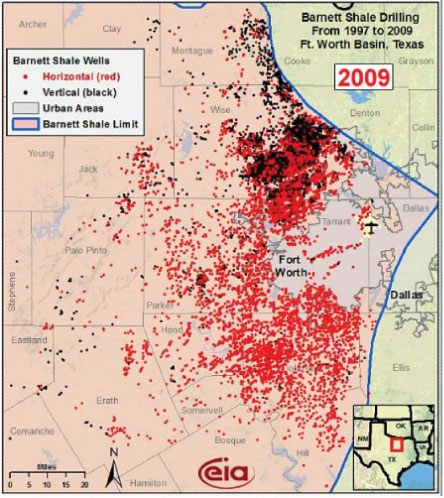

Exhibit 2: Horizontal and Vertical Wells on the Barnett Shale: 1997 Versus 2009

In the maps below, black dots represent vertical wells.Red dots represent horizontal wells.

Source: US Energy Information Administration

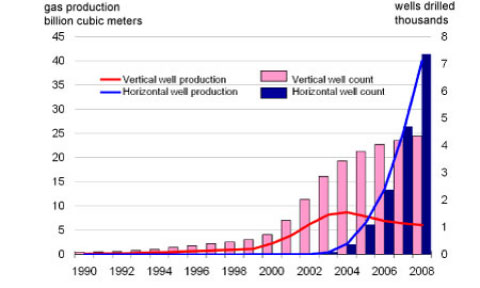

As Exhibit 2 shows, horizontal drilling has exploded on the Barnett Shale in just the last 12 years. Exhibit 3 depicts this too—showing the number of Barnett Shale wells drilled and the corresponding natural gas production.

Exhibit 3: Barnett Shale Wells Drilled and Corresponding Gas Production

Source: US Energy Information Administration

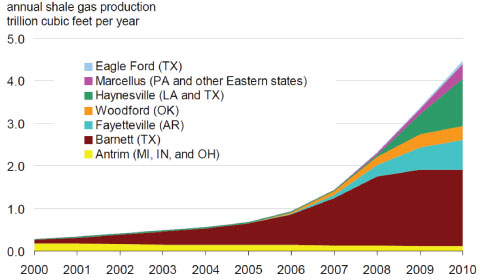

While Exhibits 2 and 3 depict solely Texas’ Barnett Shale, this is far from the only shale gas producing region in the United States. The Barnett Shale is merely the furthest along in development. Exhibit 4 shows shale gas production by regional resource.

Exhibit 4: Shale Gas Production by Regional Resouce

Source: US Energy Information Administration

Shale gas has already had a substantial impact on US gas markets in terms of reserves, resources, production, and prices. Following, we explore shale gas’s impact on each.

Proved Reserves of Natural Gas

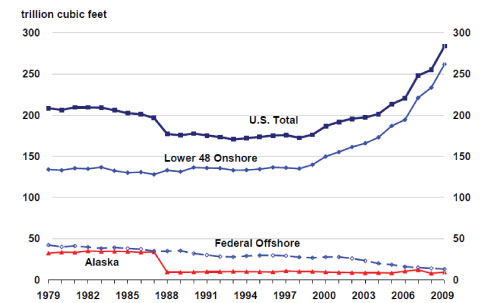

Proved reserves are gas resources that are either in production or have been conclusively proven to be technologically, economically, and legally producible under current operating conditions. From 2001 to 2009, the US Department of Energy calculates US natural gas proved reserves grew from 191 trillion cubic feet (tcf), or about 9.2 years of production, to 284 tcf (12.6 years of production)—the highest level since 1973. The increase was nearly entirely due to shale gas reserves.

Exhibit 5: US Natural Gas Proved Reserves

Source: US Energy Information Administration

Technically Recoverable Resources

Technically recoverable resources are the total amount of the resource, discovered and undiscovered, thought to be recoverable with available technology—regardless of economics. From 2000 to 2011, total recoverable resources increased from 1518 tcf to 2552 tcf. That’s an increase from about 73 years of production to 113 years. Here again, almost all the increase is attributable to shale gas. In 2010 alone, technically recoverable shale gas resources increased from 347 tcf to 827 tcf.

Some use this measure and claim the US has over 100 years of gas supply. This assumes continued technological advances will make most of these resources commercially viable—not an unreasonable belief. Even if one chooses to be skeptical about ongoing innovation, it is safe to say new technology has made gas far more abundant in the US than it was just a decade ago.

Thus, whether one prefers to measure gas supply using proved reserves or technically recoverable reserves, the influence of shale gas is clear—natural gas supply has risen massively due to shale gas.

Production

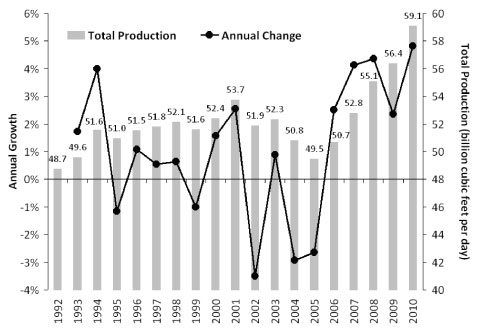

US gas production has increased roughly 20% since 2005—again, almost entirely attributable to shale gas. And it is likely shale will continue to drive US natural gas supply growth. The Energy Information Administration (EIA) projects shale gas will increase its share of domestic gas supply from 14% to 45% over the next quarter century—with a significant effect on the source of our energy supply. Whereas the EIA previously forecast rapidly rising imports, they now project only a slight increase over the next 25 years—a direct result of increasing US domestic natural gas production.

Exhibit 6: US Gas Production

Source: US Energy Information Administration, Fisher Investments Research

The Economics of Shale Gas

Technological advances in drilling for shale gas—and shale oil—have significantly reduced production costs. In fact, there’s an interesting phenomenon: In some regions (about 20% of required incremental gas supply), oil produced in the drilling process offsets the entire cost of gas production—so it effectively has zero production cost.

Most shale gas production carries a cost of about $4/mmbtu and the current marginal cost of supply is roughly $5.50/mmbtu. But even these costs have gotten far cheaper. Over the last year, the marginal cost of production has fallen from $6/mmbtu to the present, the amount of zero production cost gas has doubled, and the amount that can be produced at less than $4.50/mmbtu has increased nearly 40%. Simply, the cost side of shale gas’ economics is rapidly improving.

Market Impact

The increase of low-cost shale gas contributed to a collapse in US natural gas prices—which fell 75% during the global recession and have hardly recovered since. While UK prices saw a similar fall during the recession, they’ve rebounded 120% from their low. The oversupplied US natural gas market has not.

Exhibit 8: Henry Hub (US) Vs. NBP (UK) Natural Gas Prices

Source: Thomson Reuters, Fisher Investments Research

Looking forward, demand is the primary constraint restraining increased natural gas usage. The US Department of Energy currently expects natural gas’ share of US primary energy demand will remain stable for the next 25 years. They do forecast gas will marginally increase its share of electric power generation. However, their current expectations seem more in line with shale gas replacing imported liquid natural gas (LNG) and higher cost natural gas sources as opposed to displacing other forms of energy. This could change—long-range forecasts such as these rely on assumptions resting on assumptions, and the government’s energy policy decisions also play a role in future consumption as well.

The combination of fracking, horizontal drilling, and shale gas has resulted in a powerful energy market force depressing US natural gas prices. This force seems poised to continue moving forward, though to what extent natural gas replaces other energy sources remains an open question.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Corporate Information How You Benefit from Fisher Investments' Transparent Fee Structure

2026-08-04

2026-08-04 -

Corporate Information How Fisher Investments' High-Touch Service Helps You2026-08-04

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets — July 27 - July 312026-08-03

-

Expert Commentary 3 Things You Need to Know This Week | US Jobs, Trade Balance, Earnings Reports

2026-08-03

2026-08-03

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today