Personal Wealth Management / Market Analysis

US-China Tariff Update

What to make of the latest tariff threats between the US and China.

In the latest chapter of the US and China’s ongoing trade conflict, the US threatened to ratchet up the tariff rate on $200 billion in Chinese imports last Wednesday. China responded two days later with new tariff proposals of its own—and Washington promised to “stand tough.” Though media portray this as another step to a damaging trade war, the latest escalations still lack the size to derail the US, Chinese or global economies at large, in my view.

The US government’s latest tariff salvo isn’t exactly brand new. Rather, the US is upping the ante from its originally threatened 10% tariff rate on $200 billion in Chinese imports—aimed at a number of consumer goods ranging from fish to baseball gloves—to 25%. In response, China is aiming new tariffs at $60 billion in US imports. Overall, the rates on China’s list vary between 5% and 25%. The lower rates are focused on more advanced, less replaceable goods such as small planes and computers, while higher rates zero in on more replaceable, commoditized products. China had already threatened tariffs on basically all US imports, so this is largely a change in rates from 10% to 25%—similar to the US threat. China stated its implementation date will depend on US actions.

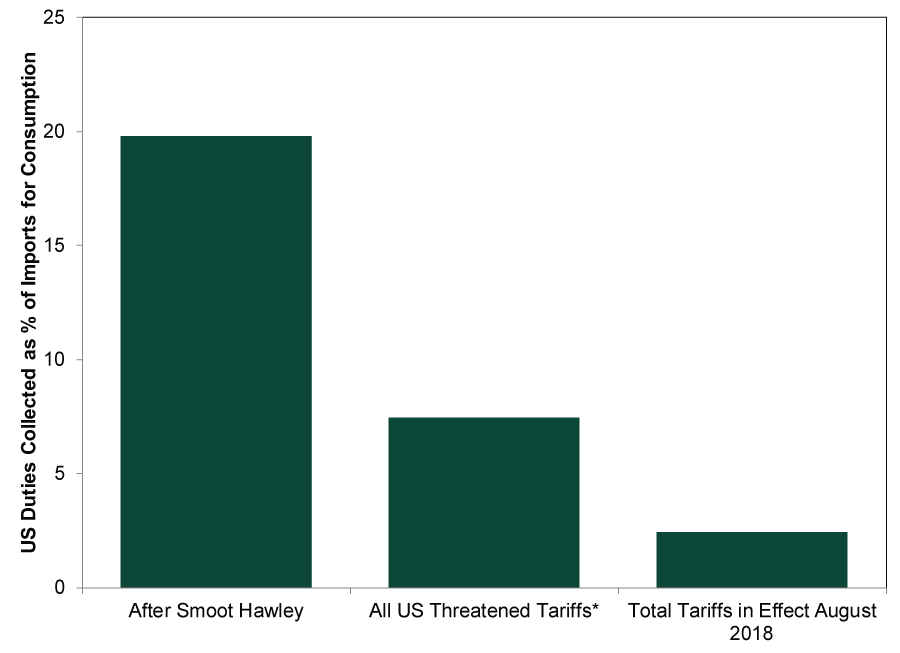

For reference, Exhibit 1 shows US tariff rates during the 1930s trade war compared to those recently implemented and threatened. While media continue fretting the world’s two largest economies hitting each other with tariffs that will devolve into a trade conflict akin to the 1930s global trade war, we are still nowhere close to that. The Smoot-Hawley tariffs resulted in a much higher effective tariff rate (19.8%) compared to the total threatened tariffs today (7.5%).

Exhibit 1: Historical and Projected US Duties as a Percentage of Imports for Consumption

Source: US International Trade Commission and US Census, as of 8/3/2018. *Assumes additional 20% tariff on all auto imports, 25% tariff on $200 billion in Chinese goods and additional 10% on additional $250 billion in Chinese goods.

This doesn’t mean today’s tariff tiff can’t escalate into something worse. However, while possible, it is still a low-probability outcome, and the global economy is likely less vulnerable to a trade shock than in 1929 when the yield curve was deeply inverted and sentiment was euphoric. Solid market drivers—like a growing global economy, still-steep global yield curve and prevalent dour skepticism that keeps sentiment in check— still underpin the bull market, and the current and threatened spate of tariffs alone aren’t enough to cancel out these positives.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Corporate Information How You Benefit from Fisher Investments' Transparent Fee Structure

2026-08-04

2026-08-04 -

Corporate Information How Fisher Investments' High-Touch Service Helps You2026-08-04

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets — July 27 - July 312026-08-03

-

Expert Commentary 3 Things You Need to Know This Week | US Jobs, Trade Balance, Earnings Reports

2026-08-03

2026-08-03

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today