Personal Wealth Management / Economics

US GDP—Better Beneath the Surface

US Q1 2013 GDP was better than many may presume if focusing on headline growth.

US Q1 2013 real GDP grew at a 2.5% seasonally adjusted annual rate (SAAR) in Friday’s preliminary report—below expectations of 3.2% growth. This miss is the focal point of most coverage, but it’s far from representative of the overall report. The details underneath reveal a healthy US private sector continued to grow nicely in the quarter.

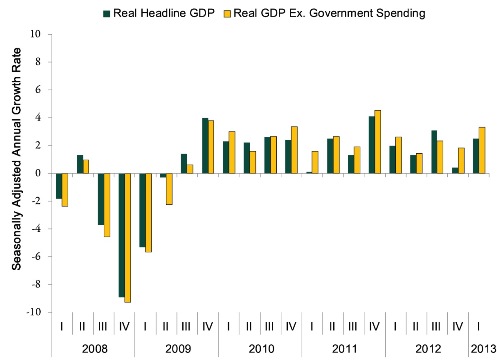

There’s nothing necessarily wrong with a 2.5% growth rate, of course. It’s a noteworthy acceleration from Q4 2012’s 0.4% growth and is tied for the fifth strongest rate since economic growth resumed in 2009. But a primary cause of the understated headline figure is government consumption, which fell again in Q1—the 11th quarterly detraction during the current expansion’s now 15 quarters. This time, reduced government spending subtracted 0.8 percentage point from headline GDP. Exhibit 1 shows headline real GDP growth and real GDP growth excluding government consumption. Excluding government spending, US GDP grew at a healthy 3.3% SAAR clip in the quarter.

Exhibit 1: Headline Real US GDP Growth and Real US GDP Growth Ex. Government

Source: US Bureau of Economic Analysis, as of 04/26/2013.

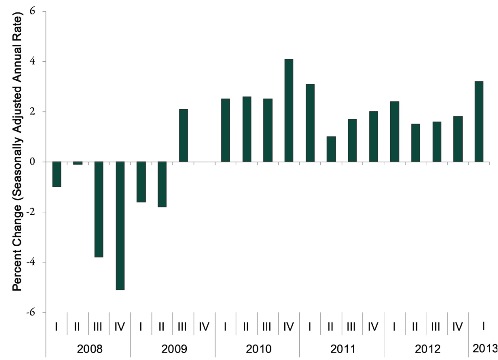

And despite some fears consumer spending would face headwinds due to the payroll tax cut’s expiration, personal consumption expenditures rose 3.2% in the quarter, the fastest pace since Q1 2011. (Exhibit 2)

Exhibit 2: Personal Consumption Expenditures

Source: US Bureau of Economic Analysis, as of 04/26/2013.

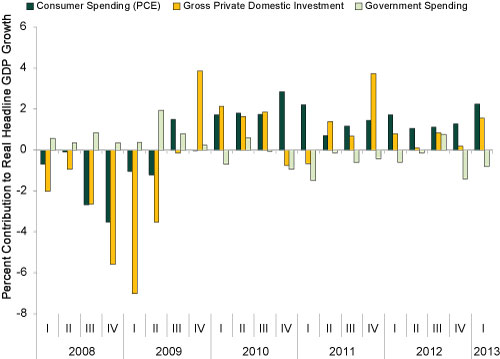

Of the major domestic categories, only government spending detracted from growth. (Exhibit 3)

Exhibit 3: Contributions from Major Domestic GDP Categories

Source: US Bureau of Economic Analysis, as of 04/26/2013.

In fact, drilling down, few domestic subcategories detracted. They are: Federal spending (both defense and nondefense); state and local spending; and a paltry 0.3 percentage point dip in investment in non-residential structures.

Net exports were a detraction, but for a reason that doesn’t suggest weakness. Exports rose 2.9% but were outpaced by faster 5.4% growth in imports. However, rising imports suggest healthy US demand—that GDP accounts for them as a negative is merely a calculation quirk. What one truly wants to see is rising total trade—exports plus imports. And that’s what happened in Q1 (though preliminary GDP reports contain very incomplete trade data).

To truly assess the state of the US economy (or any economy, for that matter) one has to look at far more than simply headline growth.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Economics Quick Hit: Durably Broad-Based Growth2026-07-29

-

Market Analysis On the Chop in the Oil Market2026-07-29

-

Politics Takaichi Raises Japan’s Wall of Worry2026-07-27

-

In The News Why Kevin Warsh should think twice about hiking interest rates — even as anxiety over the Iran war grows2026-07-27

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today