Personal Wealth Management / Economics

US Q1 2015 GDP: A Widely Expected One-Off Slowdown

Q1's GDP report reveals what everyone already knew: Winter weather was nasty, oil drillers cut back, and dockworkers struck.

The US economy grew just 0.2% (seasonally adjusted annual rate) in Q1-below economists' forecasts, but otherwise, not a surprise, and not a sign of a fundamentally deteriorating US economy. Q1's meager growth isn't a tale of a hurting US. It's a tale of falling oil prices, terrible weather and a dockworkers' labor dispute.

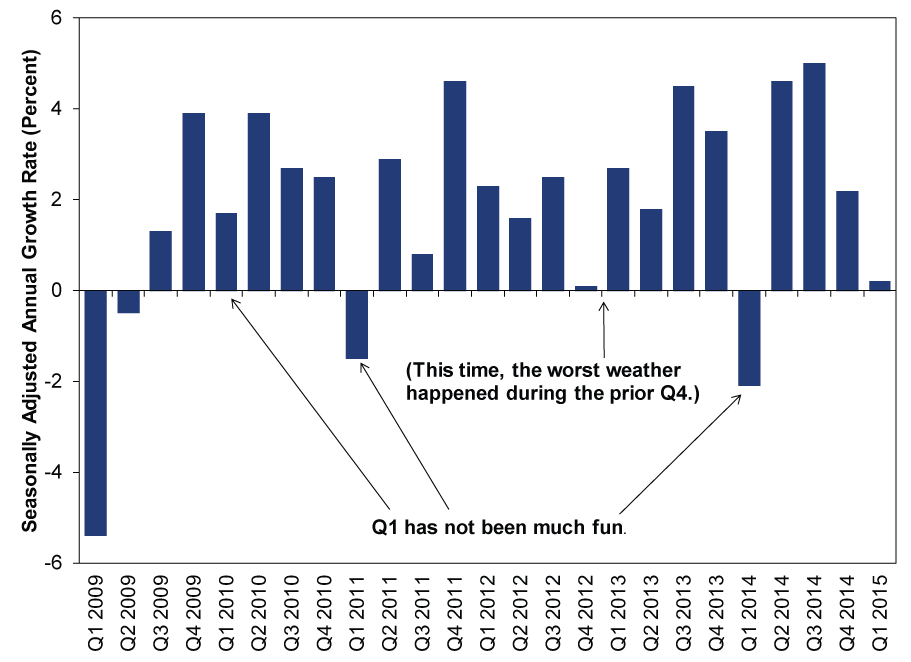

Statisticians' seasonal adjustments, in theory, are supposed to remove weather's skew, but the Bureau of Economic Analysis (BEA) has had some issues here. Q1 has been notably weaker than the rest of the year for decades, and increasingly so since this millennium began. The difference between Q1 and the rest is particularly stark during this expansion. (Exhibit 1) New York Times economist Justin Wolfers pinged the BEA about this: "Their reaction seemed to suggest that they too were surprised by these findings, and they are digging into them. In a statement, Brent Moulton, the associate director for national economic accounts, said they were 'currently examining residual seasonality in several series, which may lead to improvements in seasonal adjustments during the regular annual revision to G.D.P. scheduled for July.'"

Exhibit 1: Quarterly GDP Growth Since 2009

Source: BEA, as of 4/29/2015

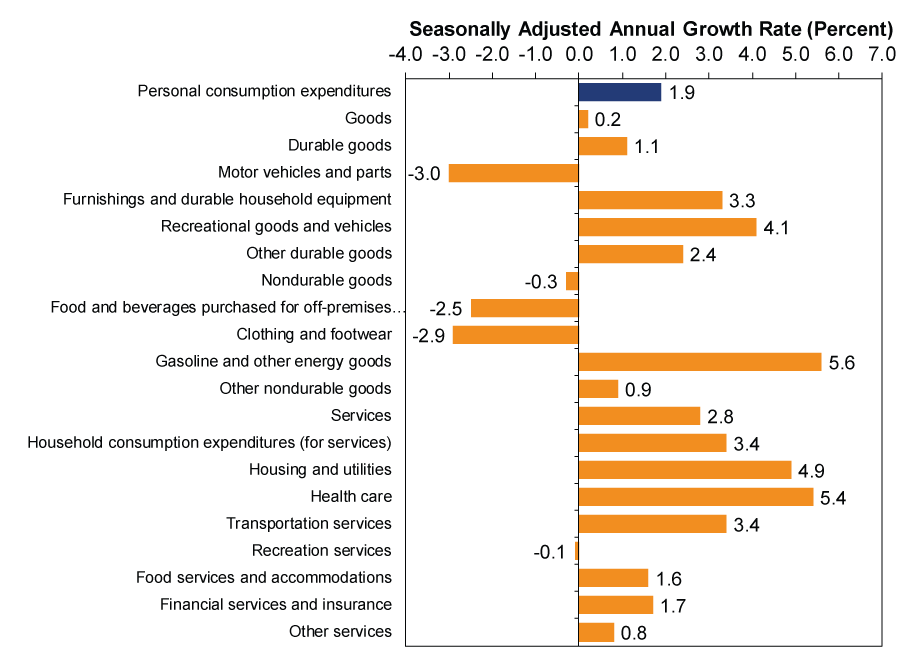

The weather's impact is readily apparent when you look at the breakdown of consumer spending. (Exhibit 2) Overall, household spending rose 1.9%. But spending on goods was anemic, and folks spent less on cars and clothing-all consistent with people avoiding the arctic freeze that slammed the Northeast. Spending on services, meanwhile, rose 2.8%, including a 4.9% jump in spending on housing and utilities-also consistent with folks hunkering down amid that arctic freeze.

Exhibit 2: Consumer Spending, Expanded Detail

Source: BEA, as of 4/29/2015

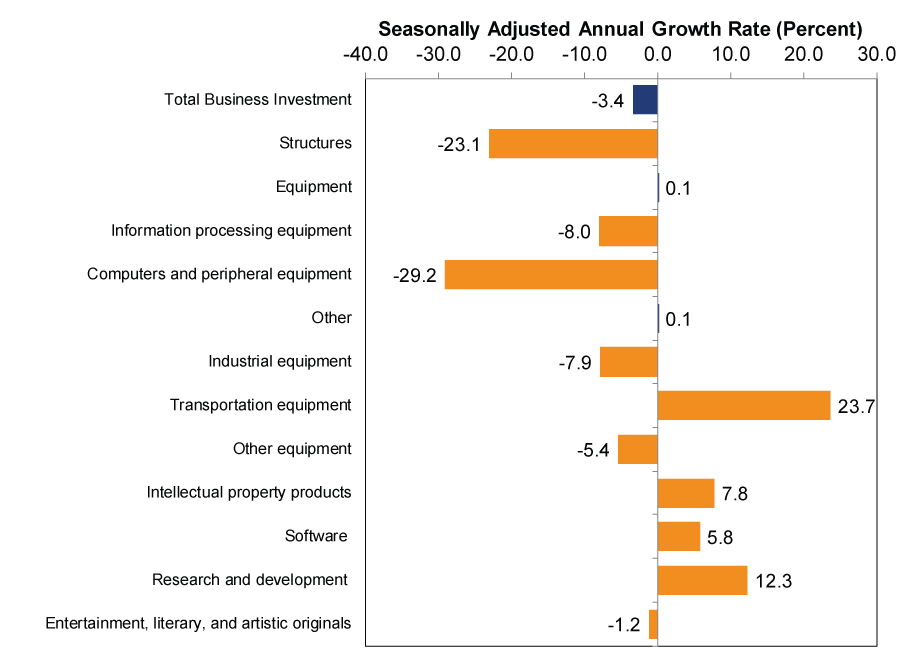

Oil's troubles are evident in business investment, which fell -3.4%. The biggest detractor was a -23.1% drop in investment in structures, which the Commerce Department says is tied largely to a $25 billion plunge in oilfield investment. This is quite unsurprising considering how far oil prices have tumbled since last June-low prices discourage firms from investing in finding and developing new wells. Up-front costs are high, and it isn't worth it unless there is a good chance revenues can recoup those costs at a decent clip. Plus, oil rig count plunged in Q1-it was no secret firms were cutting back. Yet oil's problems are oil's problems, not evidence of trouble throughout corporate America. Investment in intellectual property products, less skewed by the Energy industry, rose 7.8%-led by a 12.3% surge in research and development spending.

Exhibit 3: Business Investment, Expanded Detail

Source: BEA, as of 4/29/2015

Trade was the single biggest detractor. Net trade shaved -1.25 percentage points off total growth, primarily because exports tanked. Ordinarily this would warrant a raised eyebrow, but there is a big mitigating factor here: the West Coast Ports labor dispute. Ports idled up and down the Pacific in January and February, stranding cargo ships at sea and causing containers to stack up in ship yards for weeks on end. Longshoremen resumed normal working schedules in March, but the backlog of ships took weeks to unload, reload, and send back overseas with goods stamped "Made in the USA." Many perishable goods simply never made it. This is why that -7.2% drop in exports is no surprise and not a sign of actual fundamental weakness, here or abroad. Heck, it's a testament to strong domestic demand that imports rose 1.8% despite the shuttered ports.

Overall, this muted GDP growth looks highly unlikely to repeat. It could also very well be revised higher, depending on how those seasonal adjustments go, or lower. Those trade numbers could end up wildly different, as the March trade numbers used in the preliminary report amount to a wild guess.

Either way, we wouldn't dwell on this report. Stocks are forward-looking and have already moved on. Considering the Leading Economic Index is on a 14-month hot streak, stocks should have plenty more growth to look forward to.

Stock Market Outlook

Like what you read? Interested in market analysis for your portfolio? Why not download our in-depth analysis of current investing conditions and our forecast for the period ahead. Our latest report looks at key stock market drivers including market, political, and economic factors. Click Here for More!

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Politics The Tenth Question Facing Alberta2026-08-06

-

Market Analysis Western Oil and Gas Producers Are Ramping Up2026-08-06

-

Corporate Information How You Benefit from Fisher Investments' Transparent Fee Structure

2026-08-04

2026-08-04 -

Corporate Information How Fisher Investments' High-Touch Service Helps You2026-08-04

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today