Personal Wealth Management / Economics

US Q1 GDP Great, but Watch Expectations

As expectations for fast growth proliferate, investors should focus on whether reality is likely to follow through.

GDP is within spitting distance of its pre-pandemic level after the Bureau of Economic Analysis reported initial Q1 growth estimates yesterday. With economic activity now a hair’s breadth from its high, what should investors expect going forward? In our view, a likely return to more normal growth rates.

With GDP’s 6.4% annualized Q1 surge, it is now just -0.9% below its Q4 2019 peak.[i] Since Q2 2020’s lockdown-driven depths, when GDP stood -10.1% below that peak after two successive declines, consumer spending has unsurprisingly led growth as America reopens. This remained true in Q1, with overall personal consumption expenditures (PCE) up 10.7% annualized, leading all major categories.[ii]

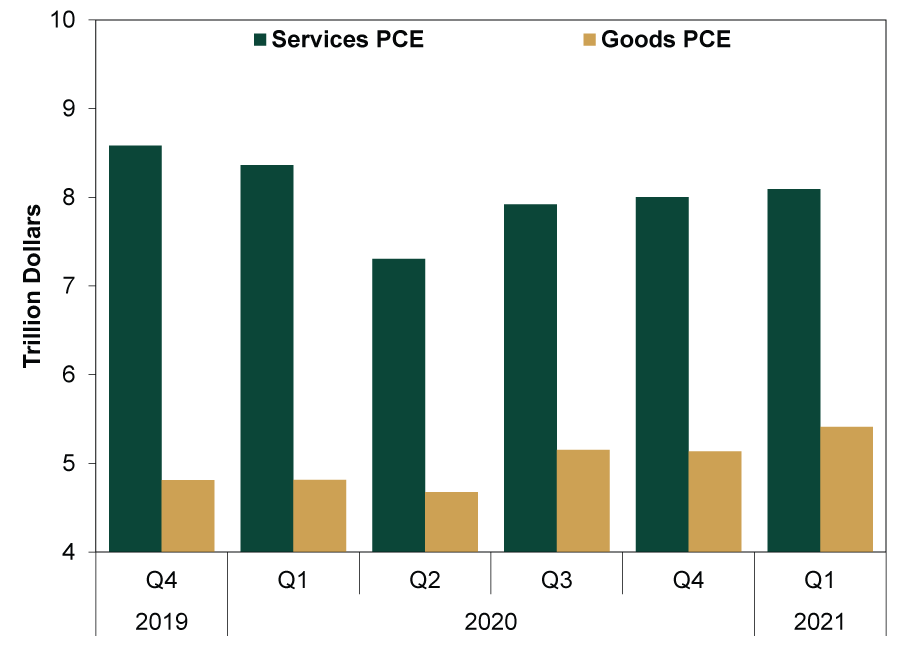

But growth in PCE—the lion’s share of GDP—hasn’t been uniform. Services PCE growth, notably, continues to lag. It grew only 4.6% annualized in Q1 versus goods PCE’s 23.6%.[iii] This is because demand for services is generally more “inelastic” than demand for goods, which is econo-jargon for less sensitive to economic trends. While some services—say travel and entertainment—are discretionary, most aren’t. Think: many healthcare expenditures, insurance payments, monthly utilities and rent. As Exhibit 1 shows, whereas goods PCE is now 12.5% above its pre-pandemic high, services PCE remains -5.7% below.

Exhibit 1: Services PCE Still Below Pre-Pandemic Level

Source: Federal Reserve Bank of St. Louis, as of 4/29/2021. Services and goods PCE, Q4 2019 – Q1 2021.

As the economy fully reopens, many expect services will surge as gangbusters goods spending eventually wanes. But we suspect services’ relatively slow growth is probably a better preview of what is to come than the goods boom. We may see a small pop when more entertainment comes back online, but that probably proves short-lived if last summer’s brief bounce is any indication.

That means all those who are extrapolating galloping growth from goods’ advance are probably in for some disappointment. Just like there is only so much exercise equipment you can buy in lieu of a gym membership, there are (probably) limited amounts of vacations you can schedule over the next year.[iv] Then, back to your normal day-to-day grind, paying the bills—business as usual. After pent-up demand is spent, consumption patterns should revert toward normal. This isn’t a bad thing. But it is important for investors to keep measured expectations. We think regular, pre-pandemic growth rates will resume before too long—perhaps before many, particularly those championing the “Roaring Twenties” theme, seem to think.

With this economic backdrop in mind, it will be critical for investors to monitor whether broad expectations diverge from the likely growth slowdown. It seems many expect a big, sustained boost from the Biden administration’s economic agenda. This stems from the recently passed $1.9 trillion American Rescue Plan to proposals like the $2.3 trillion American Jobs Plan and just-announced $1.8 trillion American Families Plan. A common sentiment we encountered among pundits reacting to the GDP report: ‘’In early 2021, the economy was served a strong cocktail of improving health conditions and rapid vaccinations along with a fizzy dose of fiscal stimulus and a steady flow of monetary policy support. Looking ahead, we foresee the economy’s spring bloom turning into a summer boom.”[v]

Others think America’s amassed stimulus checks over the last year will add fuel to the fire: “Economic growth accelerated in early 2021 as federal stimulus checks and fast-growing COVID-19 vaccinations left consumers flush with cash and ready to spend it just as more states lifted business constraints. The developments pushed up a recovery that wasn’t supposed to gather force until midyear.”[vi] Supposedly, with trillions in excess savings waiting in the wings, a second-stage services boom is about to ignite, which will launch the economy to the moon.[vii] A reality check could be in store.

If economic growth does end up disappointing, that isn’t necessarily bearish, in our view, but it likely would favor growth stocks over value. With their own growth drivers (hence the name), growth stocks don’t need the wider economy heating up to propel earnings. As expectations ramp up, we think focusing on stocks that aren’t dependent on the economy meeting them—those with diverse revenue streams, product pipelines others can’t match, proven management and fortress balance sheets—better serves investors.

[i] Source: Federal Reserve Bank of St. Louis, as of 4/29/2021. Real GDP, Q4 2019 – Q1 2021.

[ii] Source: BEA, as of 4/29/2021. PCE, Q1 2021.

[iii] Ibid. Services and goods PCE, Q1 2021.

[iv] At least when you can find open bookings.

[v] “Fiscal Stimulus Fires up U.S. Economy; Labor Market Recovering,” Lucia Mutikani, Reuters, 4/29/2021.

[vi] “The Economy Grew 6.4% in Q1 as Stimulus Checks, COVID-19 Shots, Looser Business Constraints Spurred More Spending,” Paul Davidson, USA Today, 4/29/2021.

[vii] Or Mars.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis The New Tariffs in Town Are Still Old News2026-07-24

-

Expert Commentary This Week in Review | Market Volatility, Tariffs, SpaceX

2026-07-24

2026-07-24 -

Economics A Summertime Check-in on US Consumers2026-07-23

-

Expert Commentary Why Ken Fisher Is Optimistic About European Stocks

2026-07-23

2026-07-23

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today