Personal Wealth Management / Market Volatility

Volatility by Any Other Name

As the Dow Jones Industrial Average enters bear market territory—and the S&P 500 flirts with it—it is worth remembering the name given to a pullback doesn’t determine returns from here.

Stocks’ seesaw week continues. After bouncing 4.9% on Tuesday, the S&P 500 sank -4.9% on Wednesday, hitting a new low.[i] The peak-to-trough decline breached -20% briefly late in the day before a last-minute climb pared it to -19.0%.[ii] Meanwhile, the Dow Jones Industrial Average—a broken index—now sits -20.3% below its peak, spurring “Bear Market!” headlines across the Internet.[iii] As we will discuss momentarily, magnitude alone doesn’t determine whether a downturn is a bear market. More importantly, whatever moniker this decline ultimately earns, what matters more is what stocks do from here. Look at the entire dataset of S&P 500 history, and you will see sharp declines from a high usually don’t mark the start of something long, grinding and ugly. Most often, they mean a rebound lurks nearby.

Conventional wisdom says a stock market correction is a drop between -10% and -20%, while a bear market is a drop of -20% or worse. In our view, it is a little more complex than that. Corrections are usually fast and sharp. They start and end without warning and usually feature a freakout over a scary, seemingly plausible story. Sentiment is the driving force. Bear markets, on the other hand, usually start slowly as investors shrug off danger signs, with the gentle declines luring in optimistic buyers. They usually have identifiable fundamental causes that the world overlooks until it is too late. Those causes fall in two general categories: the “wall,” in which euphoric investors have climbed the proverbial wall of worry, creating lofty expectations that reality can’t possibly match; or the “wallop,” in which a stealthy negative capable of knocking a few trillion dollars off global GDP goes unnoticed. Regardless of which recipe forms a bear, though, they tend to develop gradually—not fast, like corrections.

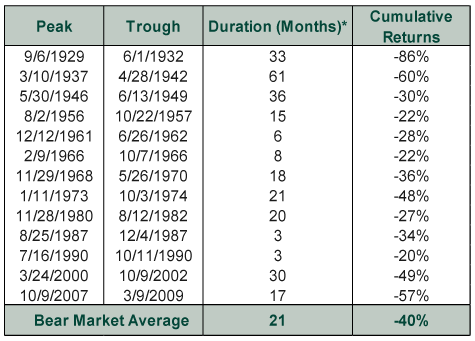

As for magnitude, bear markets don’t just breach -20%. Usually, they take extended trips below it. The one seeming exception to this trend, 1990’s shallow and short S&P 500 bear, was part of a longer, deeper global bear. Then, the MSCI World Index fell -25.9% in price terms between January 4 and September 28 and had a classic rolling top.[iv]

Exhibit 1: S&P 500 Bear Markets

Source: FactSet, as of 4/4/2016. S&P 500 price returns for the periods shown. *One month equals 30.5 days.

The S&P 500 has taken just three weeks to reach -19.0%—a correction-like plunge. Sentiment took mere days to flip from mild optimism to deep pessimism. When the coronavirus first spread outside China, stocks took the news in stride, and press coverage featured stocks’ long history of getting over pandemics. In late February, when the extent of Italy’s vulnerability became clear, that changed, and the wheels came off. Now panic rules the day. Prominent economists claim we are already in a recession. Pundits warn a financial crisis is brewing in high-yield corporate debt now that junk bond yields have spiked above 7%, potentially creating problems for cash-strapped firms trying to refinance debt. Italy’s lockdown has resurrected fear of bank implosions and sovereign default. Central banks are cutting rates, and governments are scrambling to pass fiscal stimulus packages. German Chancellor Angela Merkel said all Germans should prepare to catch the coronavirus, and UK Prime Minister Boris Johnson is potentially at risk after his Health Minister tested positive—not market drivers, but they add to the sense of dread. As for markets, go to any mainstream financial news website, and you will see a who’s who of pundits warning of more pain to come.

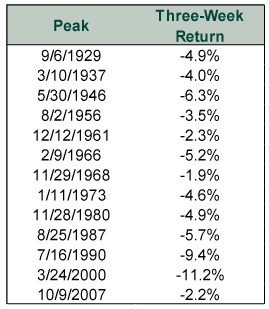

In our experience, sentiment doesn’t flip this quickly during bear markets. As Exhibit 2 shows, no bear market in history started as badly as the past three weeks. (Even 2000, which had a few big swings early, rebounded to near flat before grinding lower as the dot-com bubble deflated.) The early optimism is what makes bear markets so long and destructive. It keeps stocks from fully pricing whatever negative is lurking under the surface, buoying them with false hopes. If bull markets climb a wall of worry, bear markets spend their opening weeks and months sliding gently down a slope of hope. It isn’t until the final throes, when the extent of the trouble becomes apparent to all, that the drop gets fast and violent. These drops shake out the remaining bulls. Panic permeates all corners of the financial universe. It looks … well, it looks a lot like things do today.

Exhibit 2: Bear Markets Start Slowly

Source: FactSet, as of 3/11/2020. S&P 500 price returns over the three weeks from the date shown.

Whatever you want to call this decline, market movement and sentiment look like they typically do towards the end of a bad stretch, not the beginning, in our view. Believe it or not, this is only stocks’ 79th-worst three-week stretch in history. Of the 78 that were uglier, 62 were late in bear markets. The 2007 – 2009 bear market ended with a similar plunge. That doesn’t mean the bottom is in. Stocks could slide further or seesaw a while longer. Turning points are impossible to predict. More important, in our view, is what typically happens on the other side of a panic: a sharp rebound that forms the right half of a “V” on a chart. This, too, can happen at any time, for seemingly no reason and without warning. Even after it begins, you should anticipate a never-ending parade of pundits telling you it won’t last.

If you are investing for long-term growth and you have been patient thus far, we don’t think this is the time to cave. Capturing the rebound is likely key to getting where you want to go. We still think that rebound is likely to arrive sooner rather than later. In Wuhan, China—where the virus broke out—life is getting back to normal after about two months of quarantines. That augurs well for people in Europe, Japan, Korea and America returning to school, work and mass gatherings much quicker than folks seem to be anticipating today. Meanwhile, central banks, governments and commercial banks are working together to help otherwise solvent households and companies overcome short-term, virus-related cash crunches. Even if the more pessimistic economists are right and this does turn out to be a recession, stocks usually bottom before economic data show improvement. If you wait for official confirmation of an economic recovery, you likely risk missing significant returns.

[i] Source: FactSet, as of 3/11/2020. S&P 500 price return on 3/10/2020 and 3/11/2020.

[ii] Ibid. S&P 500 price return, 2/19/2020 – 3/11/2020.

[iii] Ibid. Dow Jones Industrial Average price return, 2/12/2020 – 3/11/2020.

[iv] Ibid. MSCI World Index price return, 1/4/1990 – 9/28/1990

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis The New Tariffs in Town Are Still Old News2026-07-24

-

Expert Commentary This Week in Review | Market Volatility, Tariffs, SpaceX

2026-07-24

2026-07-24 -

Economics A Summertime Check-in on US Consumers2026-07-23

-

Expert Commentary Why Ken Fisher Is Optimistic About European Stocks

2026-07-23

2026-07-23

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today