Personal Wealth Management / Market Analysis

Weak Auto Sales Are Normal Late in Bull Markets

Falling auto sales shouldn’t threaten the bull market.

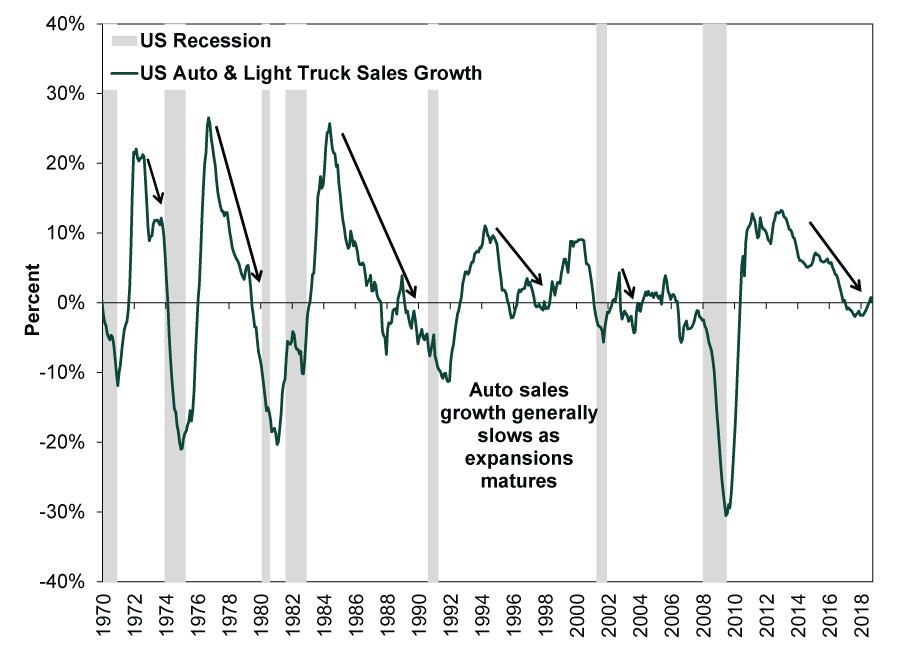

Falling auto sales caused a stir this month, seemingly contributing to investors’ collective freak-out on October 10 and 11. People often presume falling auto sales are a sign of a faltering economy. Cars are a big discretionary purchase, one often made using credit—so, the theory goes, they illustrate demand and consumer confidence, hinting at where growth may go. But this instinct is wrong. Exhibit 1 shows auto sales growth is strongest in the early stages of an expansion—as the economy bounces out of recession. Then, once the initial rebound is over, auto sales frequently decelerate as the economic cycle matures. Typically, sales turn negative during the expansion’s second half and can continue falling a long while before a recession begins. Therefore, falling auto sales aren’t a broad market-timing tool, in our view. We see them more as an ordinary feature of later-stage bull markets like the present.

Figure 1: Auto Sales Growth Tends to Surge Early Cycle and Decelerate Late Cycle

Source: US Bureau of Economic Analysis and FactSet, as of 10/15/2018. 12-month moving average in US auto and light truck sales, January 1970 – September 2018.

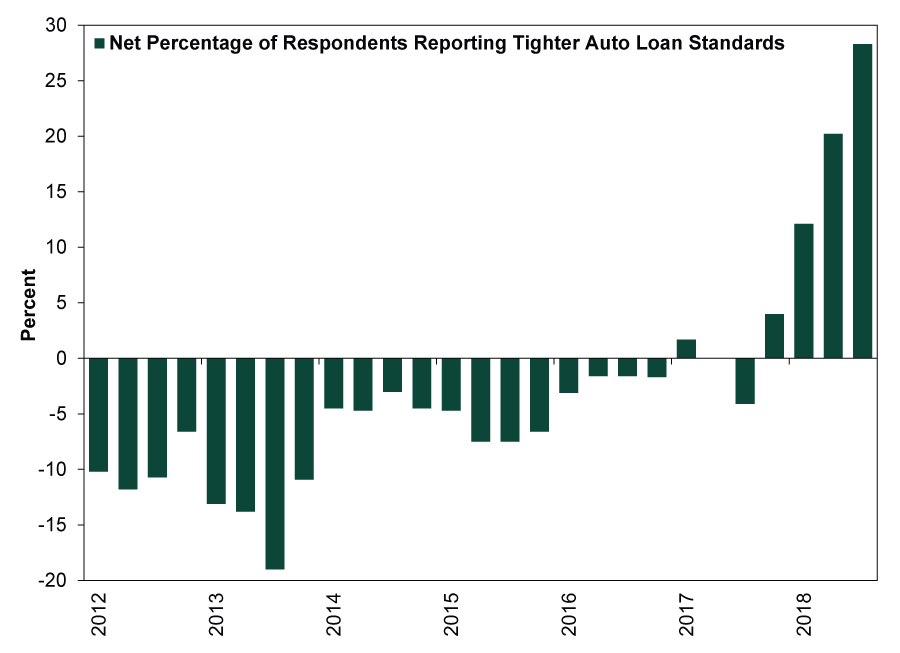

Part of the reason for late-cycle auto sales deceleration is tighter credit conditions. The current expansion is no exception. Exhibit 2 shows the net percentage of US banks reporting tighter lending standards for auto loans. Over the past year, banks have become more cautious. This is not a cause for alarm—according to the Federal Reserve, auto loans comprise only 3.3% of total US bank credit. Rather, it is just an example of how demand growth can decelerate late cycle in segments of the market that are credit-dependent.

Exhibit 2: US Senior Loan Officer Survey Shows Lenders Have Been Tightening Auto Loan Standards

Source: Federal Reserve, as of 10/15/2018. Net percentage of respondents reporting tighter auto loan standards, Q1 2012 – Q3 2018.

Falling total sales aren’t the only headwind facing auto industry stocks these days. Another late-cycle challenge for automakers is heavy competition. Early in expansions, input price growth is generally weak and the economy has plenty of excess capacity. But as capacity tightens in maturing expansions, input price gains can accelerate. In some industries, producers can be very successful late cycle if they are able to pass those costs along to customers. In other industries, producers lack pricing power, so they must absorb rising input costs, hurting profit margins. Pricing power is a complex phenomenon, but competition is one factor affecting it. Exhibit 3 compares automakers’ and smartphone manufacturers’ US market share. In the smartphone market, 4 companies take 90% of market share, while the same share goes to 10 companies in the automotive market. So when input prices accelerate late cycle, automakers have limited ability to pass those costs to customers. Any competitors with spare capacity can undercut prices to gain market share.

Exhibit 3: Automakers Face Much Heavier Competition Than Smartphone Manufacturers

Sources: The Wall Street Journal and Counterpoint Research, as of 10/15/2018.

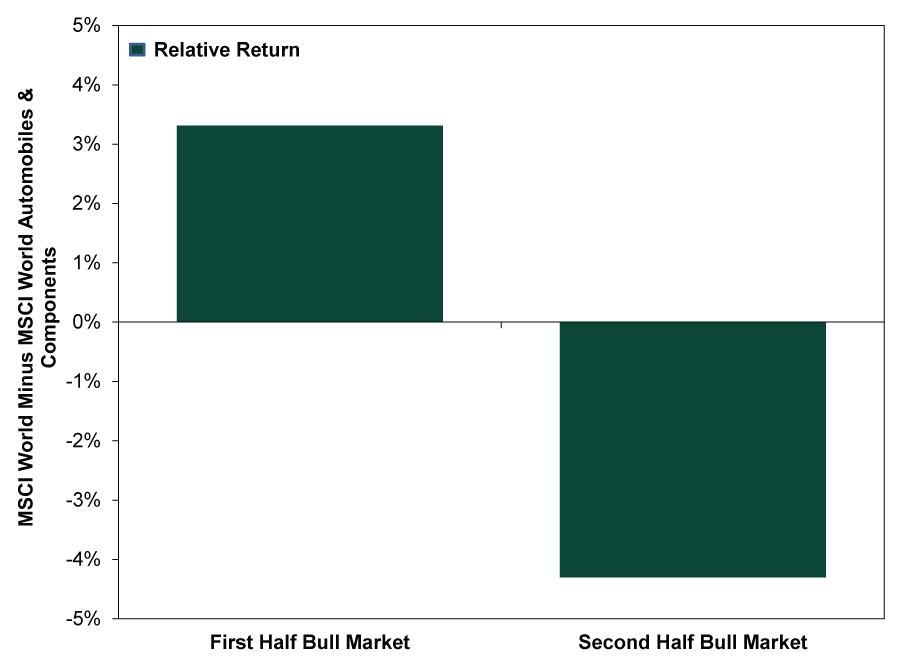

Historically, automotive stocks perform best early in bull markets. Exhibit 4 shows the average annualized relative returns for automakers versus the MSCI World by bull market halves. Since we believe we are in the later stages of a bull market when automakers historically lag the market, we believe this is a time to have less automaker exposure due to the headwinds of tighter credit conditions and heavy competition.

Exhibit 4: Automotive Stocks Historically Outperform Early in Bulls; Underperform Late in Bulls

Source: FactSet, as of 10/15/2018. Based on MSCI World Index and MSCI World Automobiles & Components Index price returns in all full bull markets from 1970 – 2008.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Politics Blunting Burnham?2026-07-21

-

Market Analysis Why the SOX “Bear Market” Isn’t Foreboding2026-07-21

-

Expert Commentary 3 Things You Need to Know This Week | Q2 Earnings, ECB Meeting, Trump Accounts

2026-07-20

2026-07-20 -

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—July 13 - July 172026-07-20

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today