Personal Wealth Management / Market Analysis

What Canada’s Oil Glut Can Teach Investors

Companies in the same sector may face different risks depending on where they do business.

Oil prices rose swiftly in mid-2018 before selling off alongside stocks in Q4, as fears of weaker economic growth stoked worries over faltering oil demand. Like stocks, though, oil has rebounded in 2019, likely leading many to wonder about the outlook for crude. To us, the global oil market appears fundamentally stable: After spending years working through a large supply overhang, supply and demand look pretty balanced. But this overall balance masks diverging fortunes for select producers. Take Canada, for example, where Energy firms are grappling with a supply glut they seemingly can’t shake. In our view, Canadian oil firms’ woes illustrate the importance of heeding factors that may affect sectors differently around the world.

Canada’s oil surplus stems primarily from a lack of refineries and pipelines. Although Western Canada[i] produces about 95% of Canada’s crude (most of that in Alberta), it accounts for just about a third of the country’s refining capacity.[ii] So much of its oil must go elsewhere for processing—ideally via pipeline, as shipping by rail or tanker truck is more expensive and slower. But Western Canadian crude output was already stretching the region’s pipeline capacity in 2017—and it kept rising in 2018.[iii] As of last September, crude supply exceeded available pipeline capacity by 202,000 barrels per day, filling up local storage facilities.[iv] New capacity isn’t arriving anytime soon, as two potential new pipelines (Keystone XL and Trans Mountain) are bottled up in court. A replacement to an existing pipeline (Enbridge 3) is on pace for completion at the end of 2019—which should help some, but is likely not material enough to make a big difference. Meanwhile, pipeline disruptions related to extreme weather and scheduled maintenance to US refineries exacerbated the supply buildup.

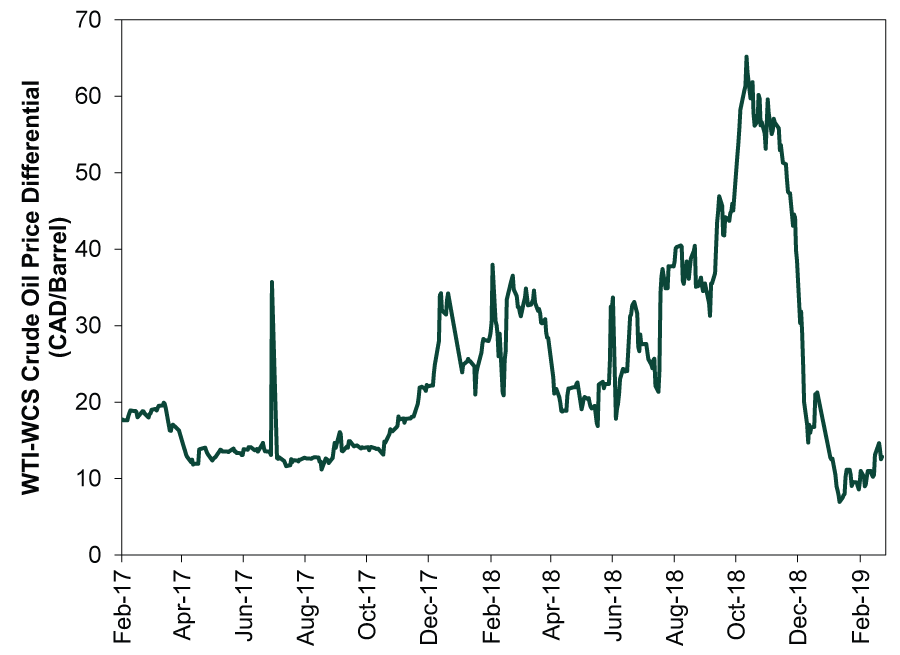

The predictable result: Canadian oil prices plunged. The spread between Western Canadian Select (WCS) and West Texas Intermediate (WTI—the US crude benchmark) rose above $50 in October, up from a 2015 – 2017 average of ~$13.[v] Since oil prices are a major driver of Energy firms’ profits, Canadian producers sought ways to boost prices. One approach: good old-fashioned lobbying. Several firms—some of which had already reduced their own production—asked the Albertan government to mandate industry-wide cuts. While the Canadian oil industry is largely privately owned, the provincial government can mandate ceilings. It doesn’t do so often. But in this case, Alberta Premier Rachel Notley—with the support of Canada’s federal government—did. On December 2, the Albertan government announced a temporary output cut of 8.7% until more storage opens up—likely around mid-year, with smaller cuts remaining until Enbridge 3 opens.

On the surface, the move appeared successful. Canadian oil prices surged, slashing their spread versus US prices.

Exhibit 1: US-Canada Oil Price Spread

Source: FactSet, as of 2/25/2019. WTI-WCS Oil Price Differential, 2/1/2017 – 2/22/2019. Price difference shown in Canadian dollars.

There was a problem, though: Thanks to the lower spread, it became too expensive to ship crude by rail to refineries in the US. Rail shipments sunk—by one measure, dropping -56% in February’s first week compared to a month earlier.[vi] If this outlet for excess supply remains economically infeasible, the glut may worsen.

Following protests by some producers, Albertan authorities permitted some firms to produce above their quota and said the cap would rise next month. The government also leased 4,400 rail cars, allowing it to buy, take orders for and ship crude itself. However, the program won’t start until July and won’t be ramped up until 2020. Nor is it clear to us that inserting the government as a middleman will help the market function more efficiently.

Government intervention also stirs doubt about future policy, making it hard for producers to plan ahead. In this case, Alberta didn’t intervene until producers requested it. But in the future, officials may not wait for industry input to act—potentially giving oil firms (and markets) less warning of approaching changes. Upcoming provincial elections—due by May—are another potential source of uncertainty. While the leader of the opposition United Conservative Party has voiced support for the cuts, a changing of the guard could spur another energy policy overhaul. Plus, if Notley’s New Democratic Party remains in power, its tactics still might change once election pressure passes. In our view, the uncertainty likely discourages investment in the sector, potentially weighing on future production and profits.

We see a few takeaways for investors here. First, we think there are probably better opportunities elsewhere in Energy currently—especially large global producers with better transportation and refinery options and lower production costs. Second, oil patch problems may prove a headwind for Energy-centric Canadian stocks. Energy represents 21% of the MSCI Canada Index—and Financials (39%) have significant Energy exposure via financing.[vii] This may help explain why Canadian stocks trailed world markets by a wide margin last year—as the glut built—including during Q4’s global correction. Now, typically, equity categories that fall the most in a correction subsequently bounce back the highest. Canadian stocks have benefited from this tendency so far in 2019. However, we think this is a sentiment feature—unlikely to last. Looking forward, we expect Canadian oil’s fundamental issues to weigh on the country’s stocks.

In our view, this underscores the importance of weighing country-specific factors when considering sectors. A sector’s outlook may be positive overall but negative in certain countries or for certain types of firms. Similarly, decisions about which countries to invest in—including your own—should take into account select sectors’ potentially outsized influence on returns. Every sector and country has unique fundamental and political risks. More knowledge about how they diverge, overlap and interact can help you be a better investor.

[i] Home to four provinces: Alberta, British Columbia, Manitoba and Saskatchewan.

[ii] Source: Canadian Association of Petroleum Producers, as of 2/25/2019.

[iii] Ibid.

[iv] “Western Canadian Crude Oil Supply, Markets, and Pipeline Capacity,” National Energy Board of Canada, December 2018.

[v] Ibid. Canadian oil trades typically at a discount against US and global oil benchmarks because it is harder to process and is located further from major refinery centers, adding to transport costs.

[vi] “Alberta’s oil cuts backfire as crude-by-rail shipments collapse,” Robert Tuttle, Bloomberg, 2/11/2019.

[vii] Source: FactSet, as of 2/22/2019.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Politics Blunting Burnham?2026-07-21

-

Market Analysis Why the SOX “Bear Market” Isn’t Foreboding2026-07-21

-

Expert Commentary 3 Things You Need to Know This Week | Q2 Earnings, ECB Meeting, Trump Accounts

2026-07-20

2026-07-20 -

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—July 13 - July 172026-07-20

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today