Personal Wealth Management / Financial Planning

What Dividends Don’t Deliver

Should investors focus solely on high-dividend stocks?

Editor's Note: MarketMinder does NOT recommend individual securities; companies referenced herein are merely cited as examples of a broader theme we wish to highlight.

All right dear MarketMinder reader, true or false: Stocks with high dividend yields are safer than regular common stocks. If you answered true, read on. If you answered false, you are correct, but still, read on so you can confirm why you were right. We frequently hear and read about investors who seek dividend stocks solely because of their yield. They seem "safer" because you seemingly get the best of both worlds: the stock's growth plus a payment back to you. However, this is a derivation of the capital preservation and growth myth, which unfortunately doesn't exist.[i] Neither, in the investment world, does true "safety." There is nothing magical about stocks with high dividends-believing they are a "safer" option can be a damaging mistake.

The myth behind high-dividend stocks' "safety" is alluring. A dividend can feel like a buffer against daily market volatility, for even if stocks are flat or drop a bit, you still receive the dividend. If the stock goes up, it may feel like a bonus. Moreover, dividends are seemingly logical candidates to provide cash flow. So why not load up on them?

Contrary to popular belief, dividends aren't foolproof. First, a dividend isn't "free money." Rather, the cash comes from the stock itself. Pretend you bought Dividend Stock XYZ at $100 per share on January 1. It pays a dividend of $5 every quarter. Meanwhile, the stock price is entirely unchanged by any factor other than the dividend for the entire year.[ii] At year end, Dividend Stock XYZ's price would be $80 because each dividend was subtracted from the share price. There is a reason the date by which you must have owned a stock to receive a dividend is called the "ex. dividend date"-it is the date the dividend is deducted from the price. This is why it is an error to liken dividends to interest. Interest is a return ON your principal. Dividends are a return OF your principal. Interest compounds. Dividends do not, unless you reinvest them.

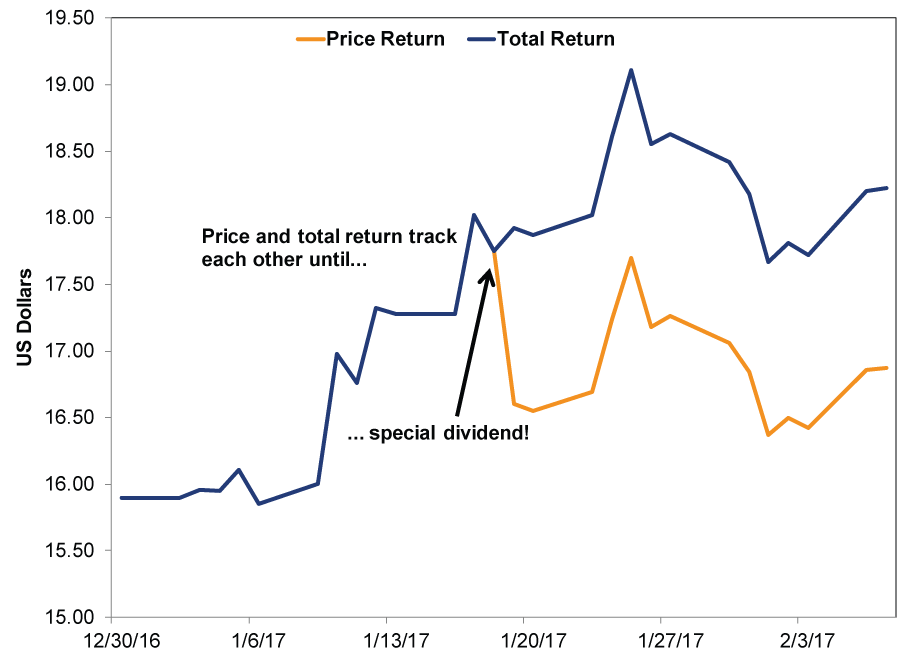

Day-to-day market volatility tends to mask typical dividend deductions, so consider these two real-life examples when firms paid out whopping, special one-time dividends. In 2012, Wynn Resorts paid out a special $7.50 dividend. Yet it didn't materially impact performance aside from that initial dividend math. Exhibit 1 shows the price and total returns (price plus dividend) of the stock around that event.

Exhibit 1: Wynn Resorts' 2012 Special Dividend

Source: FactSet, as of 1/25/2017. Wynn Resorts, price vs. total return, from 9/28/2012 - 12/31/2012.

These aren't rare events either. Just a couple weeks ago, Melco Crown Entertainment[iii] also paid out a special dividend, to similar effect. (Exhibit 2)

Exhibit 2: Melco Crown Entertainment's 2017 Special Dividend

Source: FactSet, as of 2/7/2017. Melco Crown Entertainment, price vs. total return, from 12/31/2016 - 2/6/2017.

For investors, remember that a dividend is a form of yield, compensation for taking on the risk of potential loss. Dividends also aren't guaranteed-the issuing firm can cut it at any time. The aforementioned Wynn Resorts reduced its dividend 67% in 2015 due to some struggles in its overseas business. Relying on dividends for cash flow can put investors in a tough spot should they get cut.

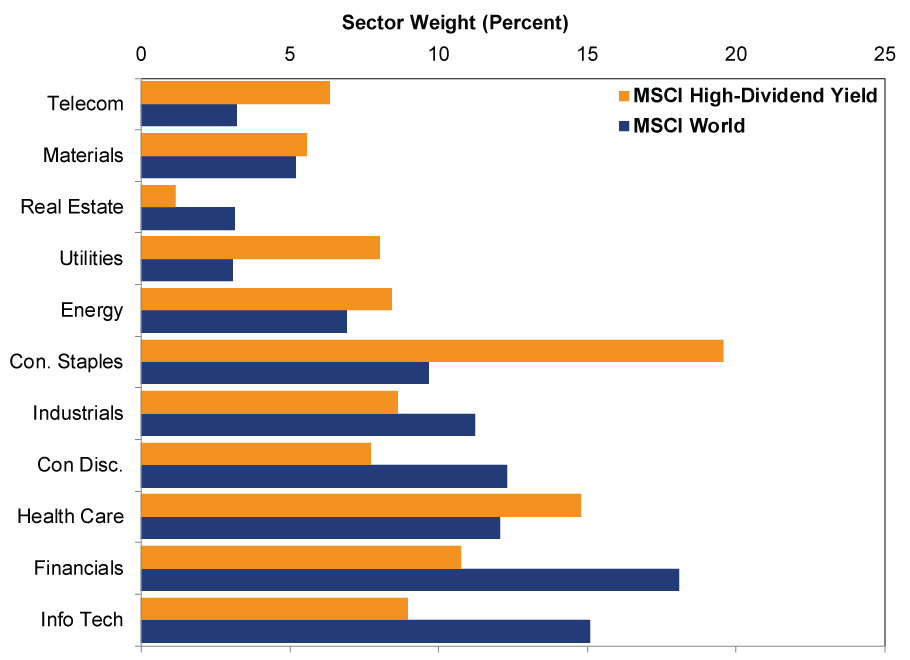

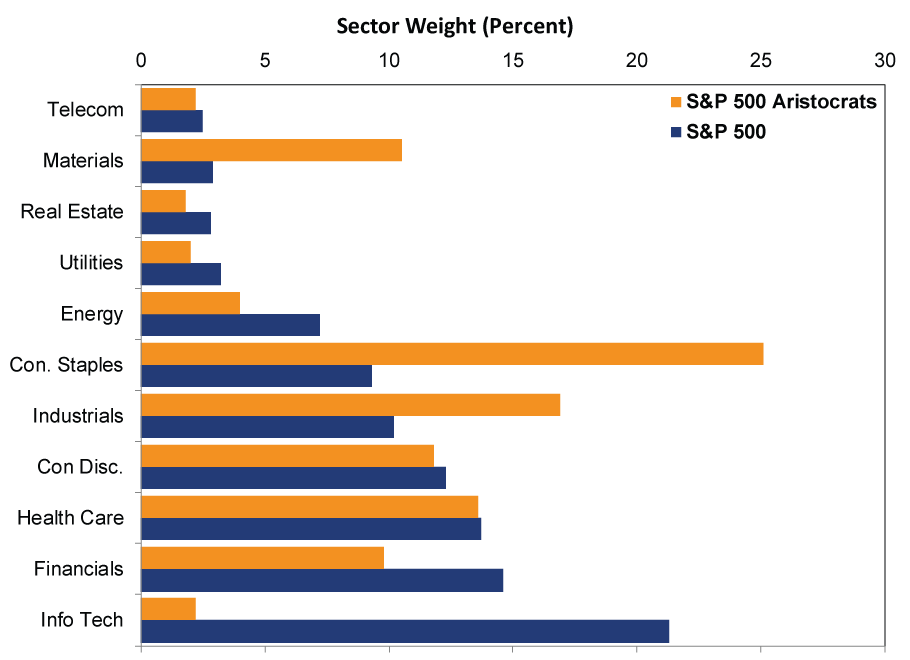

Moreover, concentrating in high-dividend stocks can reduce diversification, dividend-paying stocks are presently more common in sectors like Consumer Staples and Utilities. (They were really common in Financials, too, pre-2008, which set high-dividend investors up for a lot of hurt.) However, they are less common in other areas, and the sector composition of high-dividend indexes differs markedly from broader markets. (Exhibit 3 - 4)

Exhibit 3: Sector Weightings for MSCI World vs. MSCI World High-Dividend Yield

Source: FactSet, as of 2/7/2017.

Exhibit 4: Sector Weightings for S&P 500 vs. S&P 500 Aristocrats

Source: S&P Dow Jones Indices, as of 1/31/2017.

Consumer Staples comprises about 20% of the MSCI World High-Dividend Yield and 25% of the S&P 500 Aristocrats-nearly double the MSCI World's weighting and triple the S&P 500's. Likewise, Information Technology amounts to about 15% in the MSCI World and 21% in the S&P 500. Yet it's just 9% for MSCI's counterpart and a puny 2% in the Aristocrats index.

Rather than assign special powers to dividends, remember stocks are stocks-one class or style isn't inherently "better" than another. Many investors may prefer dividend stocks because the yield serves their cash flow needs. However, dividends aren't the only place to fulfill that. As our founder, Ken Fisher, has written before, you can get portfolio income from other sources. For instance, you could sell stocks and enjoy "homegrown dividends." While it may be taboo to tap your principal, answer this question: Why else do you have it? Plus, if you're strategic about it, you could sell as part of regular portfolio maintenance, pruning back outsized positions or selling stocks that no longer make sense to own. And homegrown dividends could be more tax-efficient[iv] too! Always think in terms of total return. Yield-in the form of a dividend or interest-is a component of that, but it isn't the only part.

Most importantly, don't forget the risks inherent in any and every security. Every investment comes with the possibility of loss, whether it's a common stock, a high-dividend stock, fixed income or anything else. For investors seeking long-term growth, we think stocks are vital. Just don't get caught up in any particular style as innately superior to others-all styles have their time in the sun, as well as the rain.

[i] It's akin to the Yeti, the Tikbalang and calorie-free cake.

[ii] For illustrative purposes, folks.

[iii] It's another casino, based in Macau. Special dividends aren't just the terrain of casinos, though. Microsoft paid one in the mid-2000s.

[iv] Disclosure: We aren't tax advisers, and this isn't tax advice. For any tax-related issues, defer to your tax adviser to determine the most appropriate action for you.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis The New Tariffs in Town Are Still Old News2026-07-24

-

Expert Commentary This Week in Review | Market Volatility, Tariffs, SpaceX

2026-07-24

2026-07-24 -

Economics A Summertime Check-in on US Consumers2026-07-23

-

Expert Commentary Why Ken Fisher Is Optimistic About European Stocks

2026-07-23

2026-07-23

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today