Personal Wealth Management / Market Analysis

What Everyone Is Missing About Inflation This Week

Please see Milton Friedman with any questions.

If sharp pullbacks weren’t so scary, it would be almost funny how investors managed to freak out collectively solely because they all bought into a flawed economic theory that a Nobel Prizewinner debunked 50 years ago. While it probably doesn’t seem like it right now, of all the crazy stories to hit sentiment in recent years, from Chinese stock market circuit breakers (2016) to teeny tiny Greece, the Great Inflation Scare of 2018 is in the running for craziest. Allow me to explain.

Tying price movement over a day or two to any one thing is almost always a foolish endeavor. But nearly everyone was scared of inflation on Friday and Monday. It started with the release of the January jobs report on Friday morning, which showed wages rising 2.9% y/y in the month—one of the fastest in eons. Considering how sluggish wage growth has preoccupied people over the last several years, you would think this would be good news. But apparently it wasn’t, because people believe wage growth drives inflation. If wages could soar before the tax cuts kicked in and really goosed investment and wages, people claimed, then it is only a matter of time before the economy overheats, wages and inflation go through the roof, and the Fed is forced to jack up short rates and end the party.

The problem with this logic is something we’ve explained here many times before: Wages don’t drive inflation. To paraphrase the late, great Milton Friedman, inflation is always and everywhere a monetary phenomenon—too much money chasing too few goods. Your three variables there are the money, the chasing and the goods. Money doesn’t refer to our paychecks. Rather, it refers to the total amount of money sloshing around the system—including anything that reasonably functions as money, like commercial paper, loans and Treasury notes. Unless economic output soars, a higher quantity of money changing hands more quickly will drive prices higher. It is simple supply and demand.

Wages are an after-effect of this. Friedman explained this quite nicely in a 1968 speech, in which he took on the popular theory of his day: a model called the Phillips Curve, which purported to link unemployment and inflation.[i] Its namesake, William Phillips, theorized that low unemployment forced employers to hike wages and then raise prices to offset the added cost and preserve profit margins. Zip, bam, boom, inflation! But there was a simple flaw in his logic, which Friedman pointed out: When employers compete for workers, they factor inflation into the wages they offer. When inflation is low, they don’t need to add much of a premium, so you get slow nominal wage growth. When inflation is high, they have to ratchet up their pay, and nominal wage growth rises. But real (inflation-adjusted) wage growth isn’t nearly so volatile.

Why is this important? When you consider that employers compete with real wages, saying wages drive inflation is tantamount to saying inflation drives inflation. What sense does that make? Does past anything drive future anything?

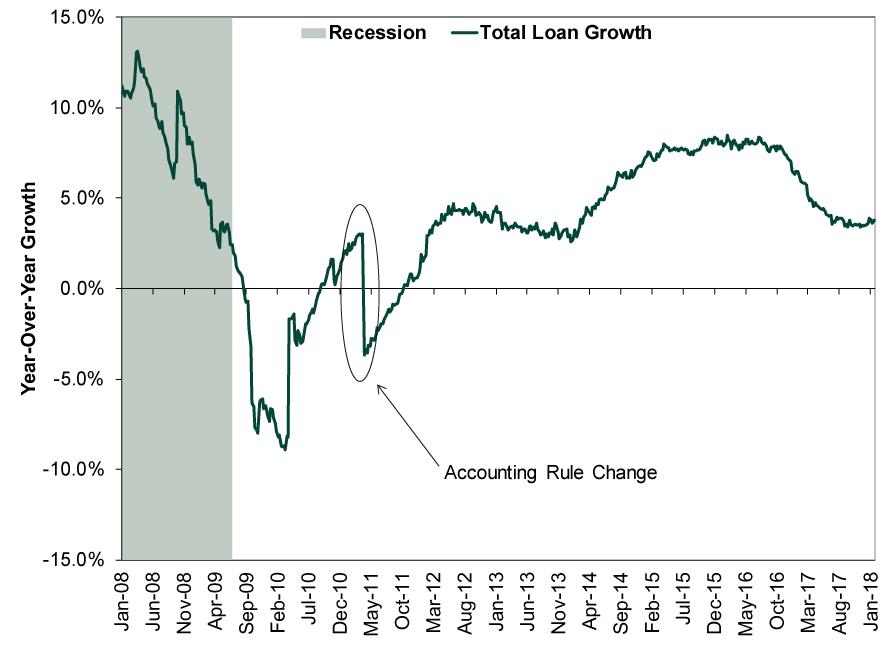

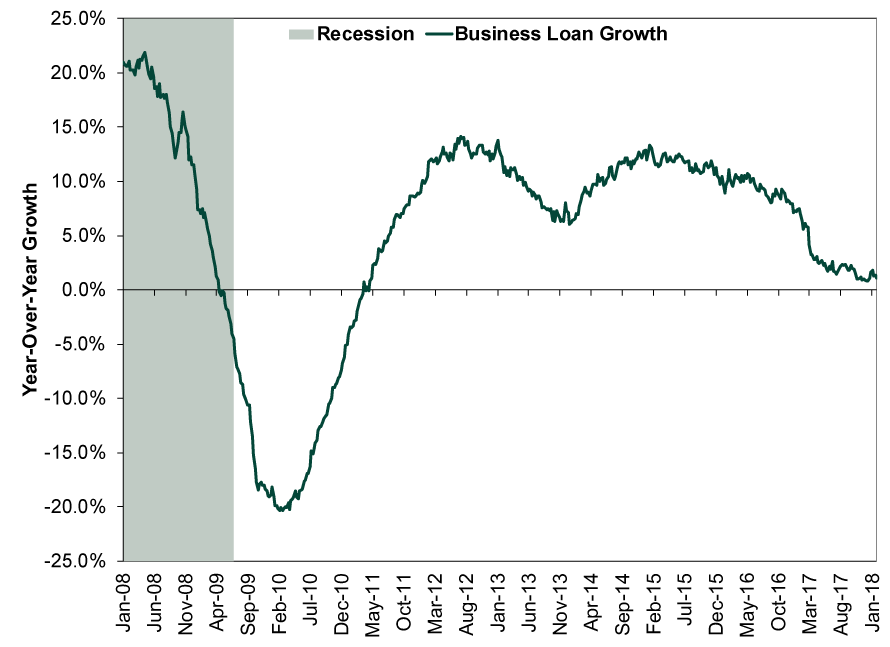

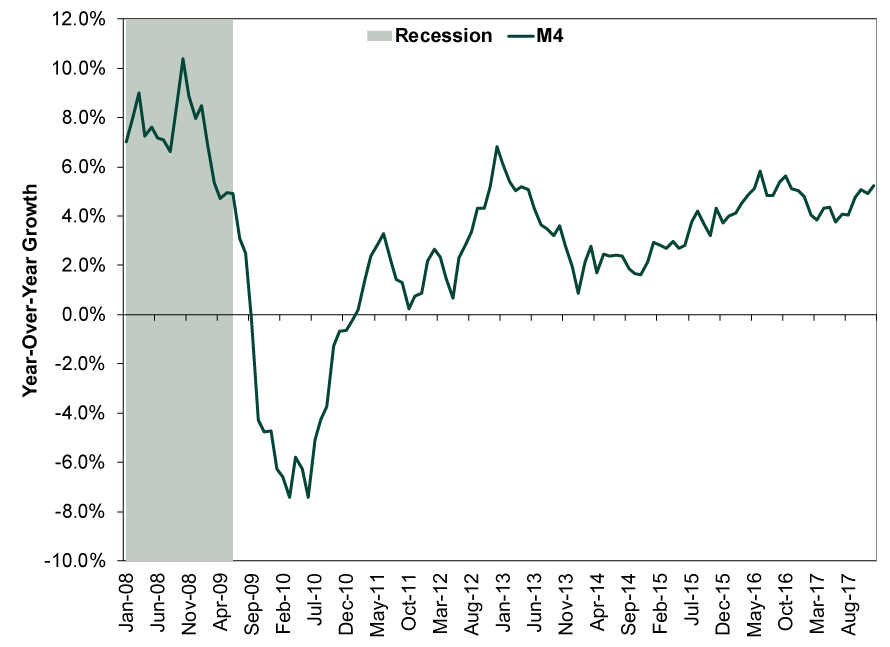

If this selloff resumes after Tuesday’s bounce, remembering your Friedman can help you stay cool. Setting aside that inflation and Fed rate hikes aren’t inherently bad for markets, you can look at some actual inflation precursors and get a sense of whether rapidly rising inflation is likely. Three good ones: total loan growth, business loan growth and broad money supply growth. Here are pictures of each. Loan growth has crawled lately. Broad money supply has picked up some but remains below levels seen earlier in this expansion—levels that preceded quite low inflation.

Exhibit 1: Total Loan Growth

Source: St. Louis Fed, as of 2/6/2018. Year-over-year percent change in total loans and leases in bank credit, weekly, 1/2/2008 – 1/24/2018.

Exhibit 2: Business Loan Growth

Source: St. Louis Fed, as of 2/6/2018. Year-over-year percent change in commercial and industrial loans, weekly, 1/2/2008 – 1/24/2018.

Exhibit 3: M4 Money Supply Growth

Source: Center for Financial Stability, as of 2/6/2018. Year-over-year percent change in M4 money supply, monthly, January 2008 – December 2017.

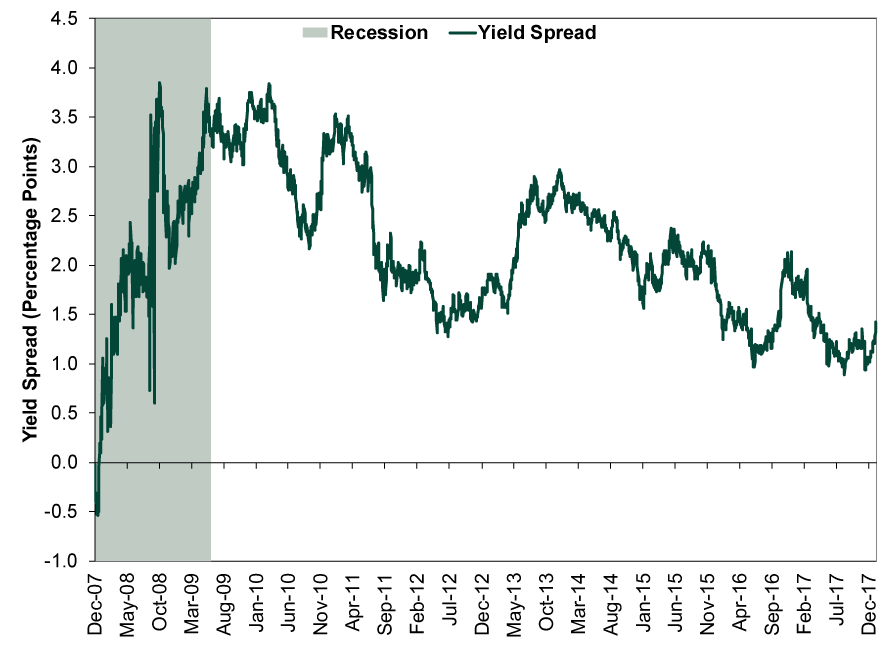

You can also look at the yield curve spread, which is a primary driver of bank lending. Banks borrow at short rates and lend at long rates, making the spread between the two their potential profit—in bankerspeak, this is called the net interest margin. The US Treasury yield spread is a good proxy for this. When it widens, margins are higher, making lending more attractive for banks, often leading to higher lending down the road. Flatter yield spreads, by contrast, tend to discourage lending. As Exhibit 4 shows, while the US yield spread has widened a smidge in the past few weeks, it remains near its lowest levels of this expansion.

Exhibit 4: Yield Curve Spread

Source: FactSet, as of 2/6/2018. 10-year US Treasury yield minus effective fed-funds rate, daily, 12/31/2007 – 2/6/2018.

There is another ironic thing about the last several days: For years, headlines have whined about US inflation undershooting the Fed’s two-percent target. Then they get a whiff of something they (mistakenly) think will finally solve the lowflation puzzle, and they decide they didn’t want it after all. Trying to have it both ways is a classic sign of unwarranted negativity. So tune out the noise, allow yourself to smile a bit, and stay cool. Pullbacks are painful in the heat of the moment, but they usually end quickly.[i] The 1970s’ stagflation later took on the Phillips Curve, too. But for some reason, many economists didn’t get the memo.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis Business Friendly Bureaucracy or No, Britain is Growing2026-07-16

-

Economics Don’t Doubt the Old World2026-07-16

-

Market Analysis On the June Inflation Cooldown2026-07-14

-

Expert Commentary 3 Things You Need to Know This Week | US Inflation, China GDP, US Retail Sales

2026-07-13

2026-07-13

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today