Personal Wealth Management / Economics

What May’s Flash PMIs Say About the Global Economy

The worst contraction seems to be over, at least for now.

Slightly less awful than April. That is our primary takeaway from last week’s release of May’s IHS Markit preliminary—or “flash”—purchasing managers’ indexes (PMIs) for many major world economies. PMIs tally the breadth of economic activity, and while more companies are now reporting an uptick, the results still show most businesses are contracting. This, despite gradual reopening, likely contributes to what seems to be an increasingly common view: that any economic recovery will be slow and drawn out. How fast that economic revival moves from here probably depends on further reopening progress. But for stocks, we think what matters most is how the economic trajectory squares with expectations.

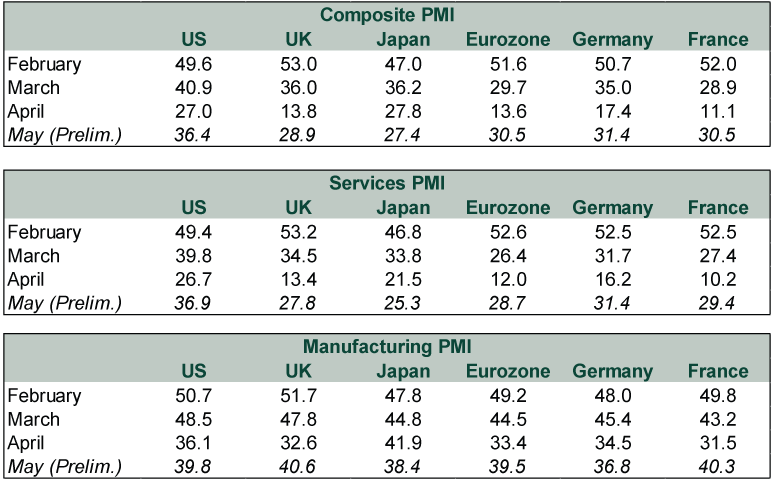

May’s flash PMIs broadly rose versus April’s extremely low levels. But all remained well under 50, indicating contraction—just not as widespread as last month’s. (Exhibit 1) Services activity—the lion’s share of developed world GDP—saw the biggest jump off of April’s depressed levels, leading the increase in composite PMIs. Yet services’ readings remained worse than manufacturing’s across the board.

Exhibit 1: Major Economy PMIs

Source: IHS Markit and FactSet, as of 5/21/2020.

Despite the bigger-than-expected bounce, these PMIs show the global economy remains in dire straits. Business contraction is still more widespread than at any time on record pre-pandemic. Forward-looking new orders also remain weak, suggesting June isn’t likely to fare much better. As IHS Markit reported for the US: “Although the overall contraction in new business eased in May, it was still the second-steepest in the series history. Firms continued to report significant decreases in client demand as customers further postponed the placement of orders.”[i] This sentiment was rife in Europe as well.

On a sector basis, services’ global rebound appeared driven by loosening lockdowns, which suggests reopening is helping unleash some pent-up demand. As for manufacturing, its continued higher readings may give the impression factories are better positioned for the crisis. Perhaps that is true, especially with factories across the developed world appearing on track to open before other businesses. But it could also be a mirage. Last month’s final read showed a record rise in firms reporting supplier delivery times lengthening. While an increase in this subcomponent is normally a sign of surging demand, in this case, as IHS Markit notes, “suppliers have simply not been making and shipping goods.”[ii] It is possible that trend continued in May, although flash PMIs lack necessary detail to really size up what is driving the uptick.

A country-by-country look makes it somewhat easier to see the lockdowns’ impact. Japan was arguably the last major developed country to impose lockdowns. So it is no surprise to us that its composite PMI didn’t budge much as manufacturing faltered. No significant lockdown lifting, no uptick. Similarly, the UK was the last Western European nation to enter lockdown. UK PMI industry details show healthcare and technology services reported growth, while many travel, tourism and leisure firms noted that business had slumped to zero. Meanwhile, Germany’s PMI appears to be leading the eurozone’s higher with the country further along in the reopening process. In America, contraction seems relatively less extensive, likely resulting from the easing lockdowns in some areas as well as e-commerce’s wider use.

More telling from a market perspective, in our view, is the reaction to the data. Few seem to be taking much comfort in May’s higher numbers. While acknowledging slight relief from easing restrictions, most coverage emphasized economic conditions’ ongoing deterioration, vulnerability to a COVID second wave and the absence of a vaccine, echoing companies’ caution. Economists remain pessimistic, saying PMIs are further evidence Q2 will likely post the worst quarterly economic contraction on record, with any recovery likely sluggish. As one bank economist put it, “People hoping for a V-shaped recovery should go back to the alphabet and pick another letter.”[iii]

Sentiment, in short, remains near rock bottom. Tentative reopening and somewhat less bad PMIs aren’t leading to a surge in optimism. For investors, souring sentiment suggests reality going forward is unlikely to disappoint markets.

[i] “May Sees Further Steep Fall in Output Amid COVID-19 Crisis,” Staff, IHS Markit, 5/21/2020. https://www.markiteconomics.com/Public/Home/PressRelease/3ea9e157cc5d447c9ecbb1ad5037cbf6

[ii] “Understanding US Manufacturing PMIs, and How Supplier Shortages Are Giving an Artificial Boost to the PMI Amid the Coronavirus Outbreak,” Chris Williamson, IHS Markit, 5/4/2020. https://ihsmarkit.com/research-analysis/understanding-us-manufacturing-pmis-and-supplier-shortages-May20.html

[iii] “Downturn in Economic Activity Starts to Ease Across the Eurozone,” Valentina Romei, Financial Times, 5/21/2020. https://www.ft.com/content/8ffb5d91-074b-4fd2-8b74-bfbbb60750e7

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis Why the SOX “Bear Market” Isn’t Foreboding2026-07-21

-

Politics Blunting Burnham?2026-07-21

-

Expert Commentary 3 Things You Need to Know This Week | Q2 Earnings, ECB Meeting, Trump Accounts

2026-07-20

2026-07-20 -

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—July 13 - July 172026-07-20

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today