Personal Wealth Management / Market Analysis

When Roaring Kitty and r/WallStreetBets Went to Washington

The highlights and lowlights of the House Financial Services Committee’s investigation into all the happenings around “meme” stocks.

If you drew a Venn Diagram involving short sellers, retail traders, social media posts, newfangled brokerages, boring stock clearing technicalities, a possibly beleaguered mall retailer and a Congressional committee, we think you would find only one point of intersection: last week’s House Financial Services Committee (HFS) hearing entitled, “Game Stopped: Who Wins and Loses When Short Sellers, Social Media, and Retail Investors Collide.” It was an investigation, HFS Chair Maxine Waters said, into whether regulations were needed following the late-January surge-and-crash in a number of “meme” stocks. We watched this endlessly entertaining five-plus-hour hearing so you didn’t have to. What follows is our summary of the highlights and lowlights. You can decide which is which.

Before we go further, please consider our disclosure: This piece will meander through the happenings in a Congressional committee hearing. Along the way, it will discuss a few individual securities. Please remember that MarketMinder doesn’t make individual security recommendations. The piece will also, by nature, touch on politics. Our commentary in this regard is intentionally non-partisan and aims solely to explore how these issues intersect with markets.[i]

Cast of Characters

Like any good theater production, this spectacle included a colorful cast, all appearing via video conferencing technology. Here are our principal players:

Keith Gill, aka Roaring Kitty, aka Deep [Expletive] Value—an individual investor who bought GameStop years ago because he thought it was deeply, umm, undervalued. He would occasionally share his research on Reddit and in YouTube videos and is widely seen as the guy who started the GameStop craze. He made sure lawmakers knew he is not in fact a cat, but his signature red headband was draped over an inspirational poster of a kitten clinging to a branch with the caption, “Hang in There.”

Vlad Tenev—founder of Robinhood, the app-based brokerage where many Redditors traded GameStop. He was there ostensibly to explain why Robinhood halted purchasing of GameStop on one of its most volatile days. Logically, he blamed a collateral call from the clearing agent, the Depository Trust Clearing Corporation (DTCC). That was too boring for congresspeople looking to grandstand, so many instead argued he was really out to do a reverse Robin Hood—steal from the poor individual investors and give to the rich hedge fund managers, like …

Ken Griffin—founder and CEO of Citadel, a hedge fund, and its associated securities firm. Citadel, despite one congressperson’s confused assertion, does not own DTCC. Rather, it is one of the investing world’s largest market makers and pays brokerage houses—including Robinhood—to execute their trades. This practice, called Payment for Order Flow (PFOF), underpinned several lawmakers’ conspiracy theories.

Gabe Plotkin—founder and Chief Investment Officer of Melvin Capital, a hedge fund whose big short position in GameStop got squeezed when Redditors bid the stock to the moon. His biggest moment came early, when he had Zoom on mute while taking his oath to tell the truth. How awkward.

Jennifer Schulp—Director of Financial Regulation Studies at the Cato Institute, there to answer questions about regulations’ influence on the GameStop saga and whether more were necessary.

Steve Huffman—CEO and co-founder of Reddit. Even after the hearing, it was unclear why he was there. But he was ready for primetime, with professional lighting, perfect posture and excellent speaking cadence—no shaky mobile devices or bad camera angles for him. Oddly, he was the only participant to stand the whole time. If he had paced the stage and gesticulated more wildly, we would have thought he was delivering a TED Talk.

Speaker #1—random unnamed person who violated Congressman Ed Perlmutter’s point-of-order reminding everyone listening to stay muted and asked Griffin: “Why are you here and what are you doing?” Only on Zoom, folks.

Five unseen people in the room with Griffin—presumably, lawyers with cue cards of sorts.

Of course, there were also the 54 esteemed members of the HFS. Those who chose to speak were allotted five minutes apiece to pepper the witnesses with questions. As they did so, it quickly became clear that to most, Tenev was the villain. Maybe also Griffin. Huffman saw a few that touched on the notion of fake news versus free speech. Very few directed any questions at Schulp. When Roaring Kitty was addressed, it was mostly to congratulate him in turning $53,000 invested in GameStop into $48 million.[ii]

Oh and in case you were wondering, yes, most of the “questions” were tangent-filled speeches, and there was a disagreement among congresspeople over whether the whole hearing was political theater.

The $35 Billion Question

Some congresspeople seemed pretty confused about how a broker-dealer operates. Several, seizing upon a passage in Tenev’s written statement, asked him to present the “$35 billion in realized and unrealized gains” he said Robinhood clients had achieved as a rate of return. They claimed this was the only fair way to view the figure, facilitating comparison to the S&P 500 or thereabouts. Otherwise, the number is trivia—meaningless.

While we agree the figure in isolation is meaningless, any presentation of it as a rate of return would be equally so. Robinhood isn’t a money manager. It is only a broker—effectively, an electronic platform allowing clients to access securities. The clients’ actions effectuate a return. Hence, there is no characterization in terms of gain and loss that would either convict or acquit Robinhood as a platform. Furthermore, there is no way to know if the comparison is actually apples to apples. Robinhood clients assuredly hold securities that aren’t stocks, so comparison to an all-equity index is faulty from the get-go.

An aside: We actually know this is true because Tenev testified that “only” 13% of Robinhood clients have traded options. Options aren’t included in the S&P 500 and constitute a different risk and return profile from stocks (risk and return that will vary dramatically depending on how they are used). Now, Tenev said this as if it minimized the amount of options trading his firm’s clients are engaged in. But in our experience, 13% of a brokerage’s clients trading options is high. Super high. We would have thought more questions would target this at the hearing. Alas, few did.

Calculating Returns Is Hard

Even if asking Tenev for Robinhood customers’ aggregate returns weren’t a nonsensical request, the notion that it is as easy as comparing dollars allegedly gained to Robinhood’s aggregate assets under custody—and then comparing that percentage figure to the S&P 500’s return—is just not how you do this.

You see, Robinhood has been active as a broker-dealer since March 2015. But its 13 million-plus users started investing at different times. Many have likely made withdrawals. Some former users have probably moved their entire accounts elsewhere.

Therefore, in order to calculate returns properly, you would have to account for each user’s deposits, additions and withdrawals—a process called time-weighted returns. For instance, pretend Sally Student starts her Robinhood account at the end of her sophomore year in college with a $5,000 deposit. That grows 10% in a year, bringing her portfolio value to $5,500. Encouraged, she adds $500. One year and another 10% return later, she has $6,600. That is great news, because she is also graduating and needs a new apartment—and her unrealized gain will cover the security deposit after taxes. Huzzah! So she sells some stock and withdraws $1,600, leaving her account value at $5,000.

If you use the congressperson’s formula, then her return would be 0% in two years. That is obviously incorrect. In reality, it would be 21%, because you would multiply the 10% returned before the cash addition by the 10% returned after the cash addition. If she then earned 15% on her $5,000 in year three of investing, her cumulative return would be 39.2%. (But by the congressperson’s math, it would be just 15%.)

Complicated? Yah, that is the point. Calculating performance for even one person requires careful tracking and math. Extrapolating that across all of Robinhood’s current and former clients is … a lot. Doable, and it wouldn’t shock us if Robinhood had some sort of algorithm tracking that internally. But that is what it would take, not some quick mental math on a webcam.

Let the Market, Not Brokerages, Judge Rationality

The fact Robinhood is a brokerage also invalidates another representative’s line of questioning that queried whether it should police trades placed by customers to “ensure that investors are making trades based on legitimate, material, financial information and not social media, the design of trading platforms or any other superfluous reason.” Tenev seemed a bit taken aback by the question, and we can see why: For one, it is impossible. But also, again, Robinhood is a broker-dealer. They are not a Registered Investment Adviser and do not have discretion over client accounts.

Individual investors will trade for a host of reasons. Some, like Roaring Kitty, seem quite rational indeed. Others are probably less so. But who is to judge? In our many years analyzing mainstream financial press, social media, newsletters, books, television commentary and the like, we have seen lots of preposterous theories about why you should buy or sell this-or-that. We have seen it from professional analysts. We have seen some good coverage from all these outlets too. If investors seek help in discerning which information is useful and which isn’t, they have options:

- Read MarketMinder religiously[iii]

- Hire a Registered Investment Adviser[iv]

- Get extremely educated and fact-check the information they encounter.

The idea of a broker-dealer even attempting to build a system that analyzes why you bought or sold something is not only silly (and would be rather heavy-handed if it were doable), it totally mischaracterizes their role. You could actually see the fallacy of this right in the very same hearing. Roaring Kitty’s original thesis to buy GameStop, per his testimony, was that the $5 stock was undervalued. He saw it as a company that should have been valued at $20 – $25 per share, based on his fundamental analysis. Hedge fund manager Plotkin thought the stock was fundamentally overvalued. Who was right? Plotkin seemed to be for about six years, considering he first sold the stock short in 2014. Roaring Kitty obviously scored big this year. Both contend they are still correct now!

This all highlights a key point: A variety of opinion is essential to market efficiency. If everyone believed the same things were sensible and the same things off base, markets would price only those factors in, leaving ginormous blind spots. You need to have an array of people that disagree, perhaps vehemently, to allow stocks to see and weigh a wide range of views.

Speaking of Markets’ Efficiency

As for Huffman, congresspeople targeted him with questions on whether the Redditors’ stock discussions constituted market manipulation. He made a number of great points in defense of individual investors’ analytical chops and rightly pointed out there is no functional difference between an individual talking about their investment thesis online and a professional doing it on CNBC—except that in some cases the professional may have more conflicts of interest, depending on their role and business model. But then he made a comment that was excellent in spirit but might lead investors astray if they take it too literally:

“On Reddit, I think the investment advice is actually probably among the best because it has to be accepted by many thousands of people before getting that foot of visibility.”

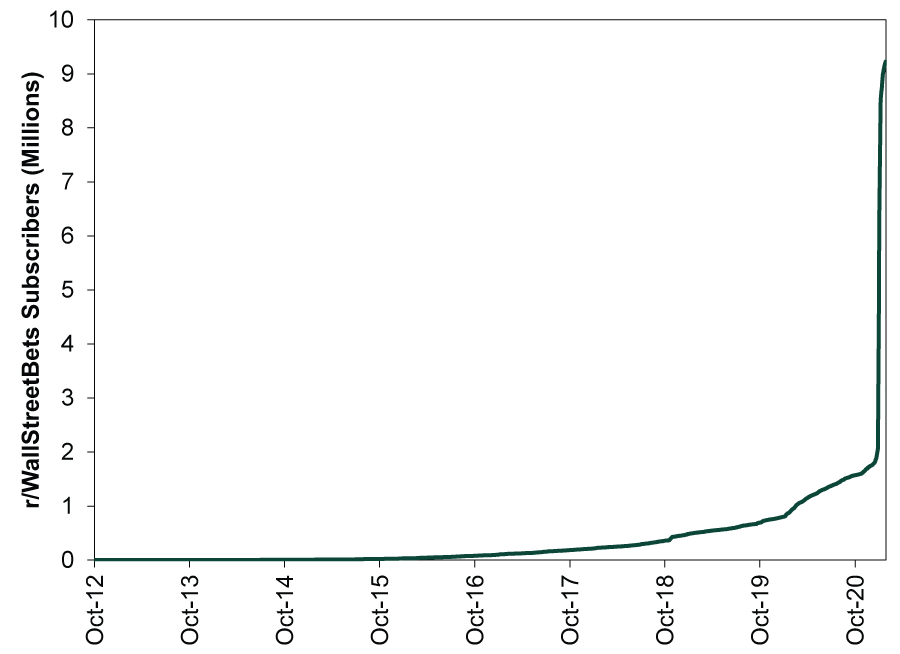

Yes, that might indeed help the higher-quality analysis rise to the top of the forum and become the most visible. But the problem is that with so many eyeballs on said advice, by the time it gets enough upvotes to rise to the top, it is probably already priced in—particularly with the WallStreetBets subreddit now having over 9 million users. Everyone who upvotes an investment thesis considers that advice and makes the decision to buy, sell or do nothing. All of those opinions influence the price. So by the time you read it, many, many someones have already traded on it. Any edge it offered originally is gone. Even if it was great advice!

Markets incorporate all widely known information efficiently. Maybe that didn’t include posts on WallStreetBets years ago, when its user count was tiny. But as Exhibit 1 shows, there are far too many eyeballs there now. As Plotkin alluded when questioned, hedge fund analysts and algorithms are incorporating its content. So yes, depending on your humor, r/WallStreetBets is entertaining. It is fun watching funny and smart people talk about their trades. The memes are glorious. But posts there are probably not worth acting on these days unless you are interpreting the information differently than the Reddit crowd is. Not that GameStop and other meme stocks are perpetually doomed, as today’s spike attests (although we would guess that was tied to some actual news about the company’s turnaround strategy). But notwithstanding day-to-day wiggles, our general point holds: As our firm’s founder and Executive Chairman, Ken Fisher, put it in his classic book, The Only Three Questions That Count, the best edge in investing comes from knowing something others don’t or interpreting widely known information differently (and correctly) than the crowd.

Exhibit 1: R/WallStreetBets Subscriber Count

Source: SubredditStats.com, as of 2/24/2021.

What About Payment for Order Flow?

As for the hearing’s big philosophical question: Is Payment for Order Flow evil? Several congresspeople seemed convinced the answer is Yes, arguing the legal practice amounts to bribery, creates conflicts of interest and benefits the market maker disproportionately—presuming they will yield to the temptation to front-run client trades. Griffin and Tenev tackled these claims multiple times, reminding lawmakers that PFOF is chiefly responsible for brokerages’ ability to offer zero commissions. (Amusingly, one HFS member responded to this with the earthshattering revelation that there is no such thing as a free lunch).

Trading has always had two sets of costs: explicit, which refers to commissions; and implicit, which refers to bid/ask spreads, liquidity and other items that could lead to an inferior purchase or sale price for the customer. PFOF has, arguably, helped mitigate these implicit costs to a great degree as well. Griffin discussed this extensively when citing the advantages of executing trades at so-called dark pools via Citadel Securities or other market makers versus the public exchanges.

Griffin’s case is that exchanges are legally required to keep “tick” sizes at a minimum of one penny—meaning, stocks get priced to the penny, rather than a fraction thereof. That keeps bid/ask spreads (meaning, the going purchase bid and the going price for sale) further apart. In a dark pool, pricing can go several more decimal places, and bid/ask spreads are narrower, which can ultimately get the client better pricing. That isn’t ostensibly a case for PFOF, though, as much as it is one for executing trades via wholesalers. PFOF encourages that, which is how this comes into the equation. But it is what Griffin and the five off-camera folks argued.

Furthermore, stock exchanges are for-profit organizations, and a big chunk of their revenue comes from transaction fees. Those can make it more costly for retail brokers to execute client trades there. Directing client orders through wholesalers, who can transact on their own internal system versus paying costly exchange fees, is a big reason commissions have nosedived in the last 20 years, in some cases going to zero. Banning the practice would probably undo a lot of these gains.

To us, PFOF is an overall net benefit to investors. It is hard to empirically prove, though, as clear counterfactuals are generally lacking. A recent study by Bloomberg found that, “Retail brokers’ controversial practice of selling client orders to market makers (payment for order flow) benefits equity investors by enhancing execution quality, with our analysis showing that Citadel Securities and its peers returned $3.7 billion in 2020 to investors in the form of price improvement.” … “That’s nearly 3x what they paid for that equity flow.”[v] But regardless, there is also no doubting the complexity of the issue, which is likely how it fuels this kind of debate. If the providers and/or regulators find a way to add transparency or clarity to the inner workings of PFOF and how it affects overall execution cost and quality, that would be a good thing. But treading lightly here is important. (HT: Fisher Investments’ Trading Desk for contributing their views to this.)

Did Something Very Wrong Happen Here?

That is the question this hearing purportedly aimed to answer. But after five hours’ viewing, we aren’t sure we got any closer to an answer. Depending on one’s point of view, certainly, PFOF could be viewed as wrong. Roaring Kitty and the Redditors[vi] could be cast in a negative light as market manipulators, irrational traders or other. Obviously, hedge fund managers and the founder of a new brokerage that targets new retail investors could be. Many paint social media execs in a negative light daily. Preventing Redditors from buying based on boring capital requirements has already fueled conspiracy theories. Congress, of course, could be looked at as usually wrong.

But, contrary to the conclusion of one representative who was sure something “very wrong had happened here,” the evidence for that is still lacking. Yes, some folks who piled in late suffered when GameStop (et al) tumbled. Yes, some hedge fund clients may have taken it on the chin when Melvin Capital closed its short position at a loss. But those facts alone don’t mean something untoward happened.

In our view, the bigger risk from all this isn’t that these weird things take place on rare occasion. After all, and as we wrote previously, we never thought this saga was material for long-term investors. It was a curiosity that drew eyeballs—lots of them—because it didn’t neatly fit pre-existing narratives around markets. Hearings like this one more or less prove that. No, in our view, the more realistic risk is that legislators see what happened as problematic and act rashly. Thankfully, there is no sign of that today—and no way to infer what could happen from this broad ramble of a hearing. But there may be more yet to come on this. If so, we will be watching.

[i] We definitely don’t make individual politician recommendations, either.

[ii] The plaudits will look very odd if the suit courts rule against him in litigation alleging securities fraud.

[iii] Even we are not above a shameless plug, we guess.

[iv] See note iii.

[v] Robinhood-Gamestop Hearing Will Scrutinize How Brokerages Get Paid for Trades,” Bob Pisani, CNBC, 2/18/2021.

[vi] We want a hat tip if you choose this for a band name.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary Why Ken Fisher Is Optimistic About European Stocks

2026-07-23

2026-07-23 -

Economics A Summertime Check-in on US Consumers2026-07-23

-

Politics Blunting Burnham?2026-07-21

-

Market Analysis Why the SOX “Bear Market” Isn’t Foreboding2026-07-21

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today